モメンタム指標クロス反転トレンド追跡戦略

概要

本戦略は、MACD、RSI、ADXなどの複数のモメンタム系テクニカル指標を総合的に活用し、価格の反転シグナルを識別します。逆張り戦略を採用し、強いトレンドが反転した際に逆張りでエントリーします。また、損切りと利確を設定することで、利益を確定しリスクを管理します。

戦略の原理

本戦略では、まずMACD指標の短期移動平均線と長期移動平均線のゴールデンクロス・デッドクロスを比較して価格トレンドを判断します。次にRSI指標を組み合わせてダマシのブレイクをフィルタリングし、本当の価格反転が発生した後にのみ取引シグナルを生成します。最後にADX指標を利用して、価格がトレンド状態に入ったかどうかを再度検証します。これらの複数条件がすべて同時に満たされた場合にのみ、買いまたは売りのシグナルが発生します。

具体的には、MACDの短期線が長期線を上抜け、RSIが50を超えて上昇し、ADXが20を超えた場合が買いシグナルです。MACDの短期線が長期線を下抜け、RSIが50を下回って下落し、ADXが20を超えた場合が売りシグナルです。

優位性分析

本戦略の最大の優位性は、複数の指標を組み合わせることで、レンジ相場や誤ったシグナルを効果的にフィルタリングし、トレンドの反転ポイントを確実に捉え、高い勝率を得られることです。また、損切りと利確を設定することで利益を確定しリスクを管理し、予期せぬ事象の影響を効果的に抑えることができます。

リスク分析

本戦略の最大のリスクは、トレンド反転の判断を誤ることです。例えば、価格が深い押し目をつけた場合に誤った判断をする可能性があります。また、反転後の新しいトレンドの持続性が不十分で、十分な利益を得られないリスクもあります。

解決策としては、パラメータをさらに最適化し、損切りの幅を調整するか、追加の補助指標を組み合わせてシグナルをフィルタリングすることが考えられます。

最適化の方向性

本戦略は以下の方向性でさらに最適化できます。

- MACD、RSIのパラメータ組み合わせを最適化し、価格反転の判断精度を向上させる。

- KD、BOLLなどの追加指標を増やし、指標による包囲効果を形成する。

- 損切りの幅を動的に調整し、異なる市場状況に応じて調整する。

- 反転後の実際の値動きに基づいて、利確位置をリアルタイムで修正する。

まとめ

本戦略は、複数のモメンタム指標を総合的に活用し、潜在的な価格反転の機会を識別します。パラメータ最適化、より多くの補助指標の組み合わせ、損切り・利確戦略の動的調整により、戦略の安定性と信頼性をさらに高め、市場が提供するさまざまな取引機会を確実に捉えることができます。

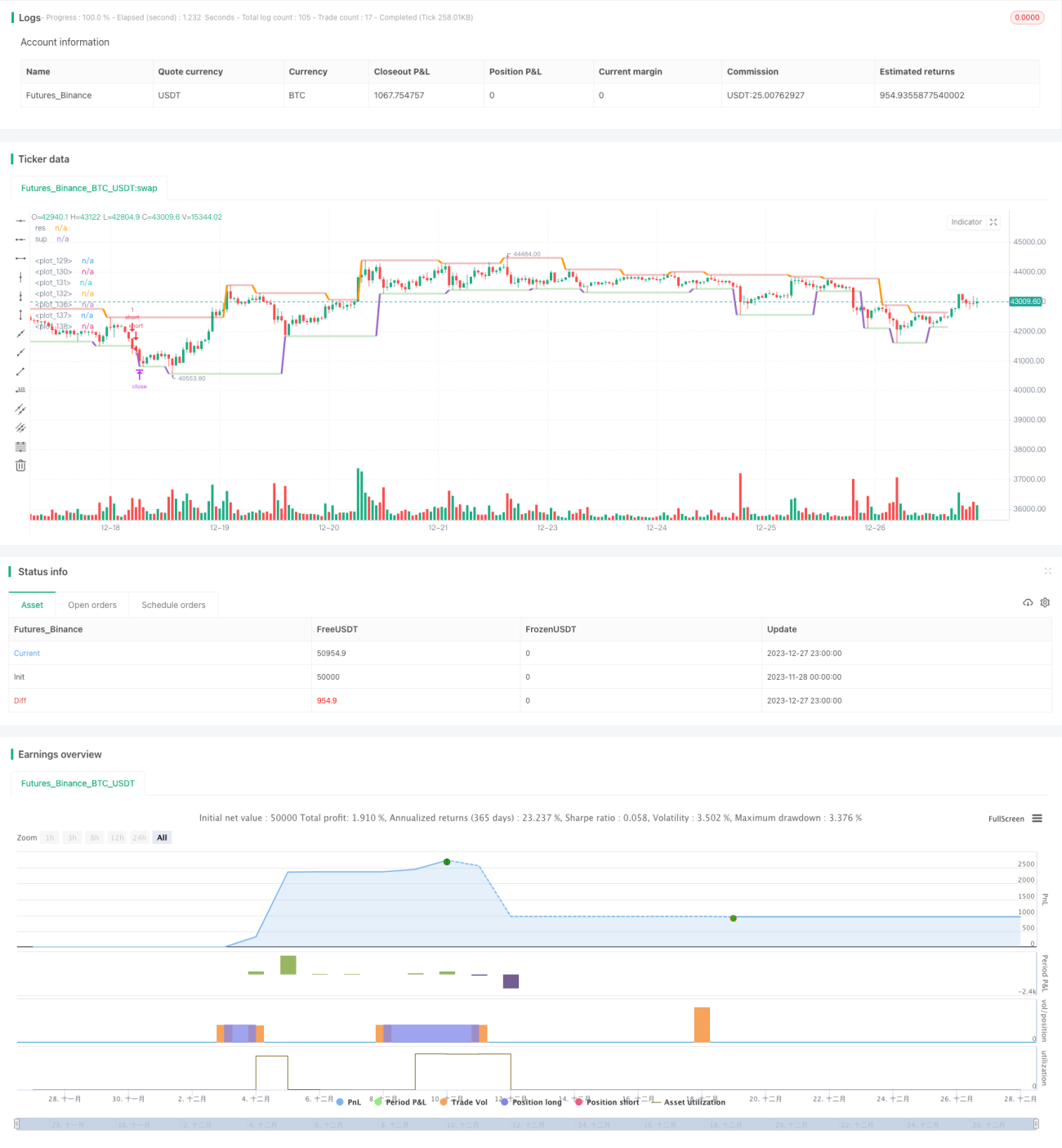

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © AHMEDABDELAZIZZIZO

//@version=5- 1