ボリンジャーバンドATRトレーリングストップ戦略

概要

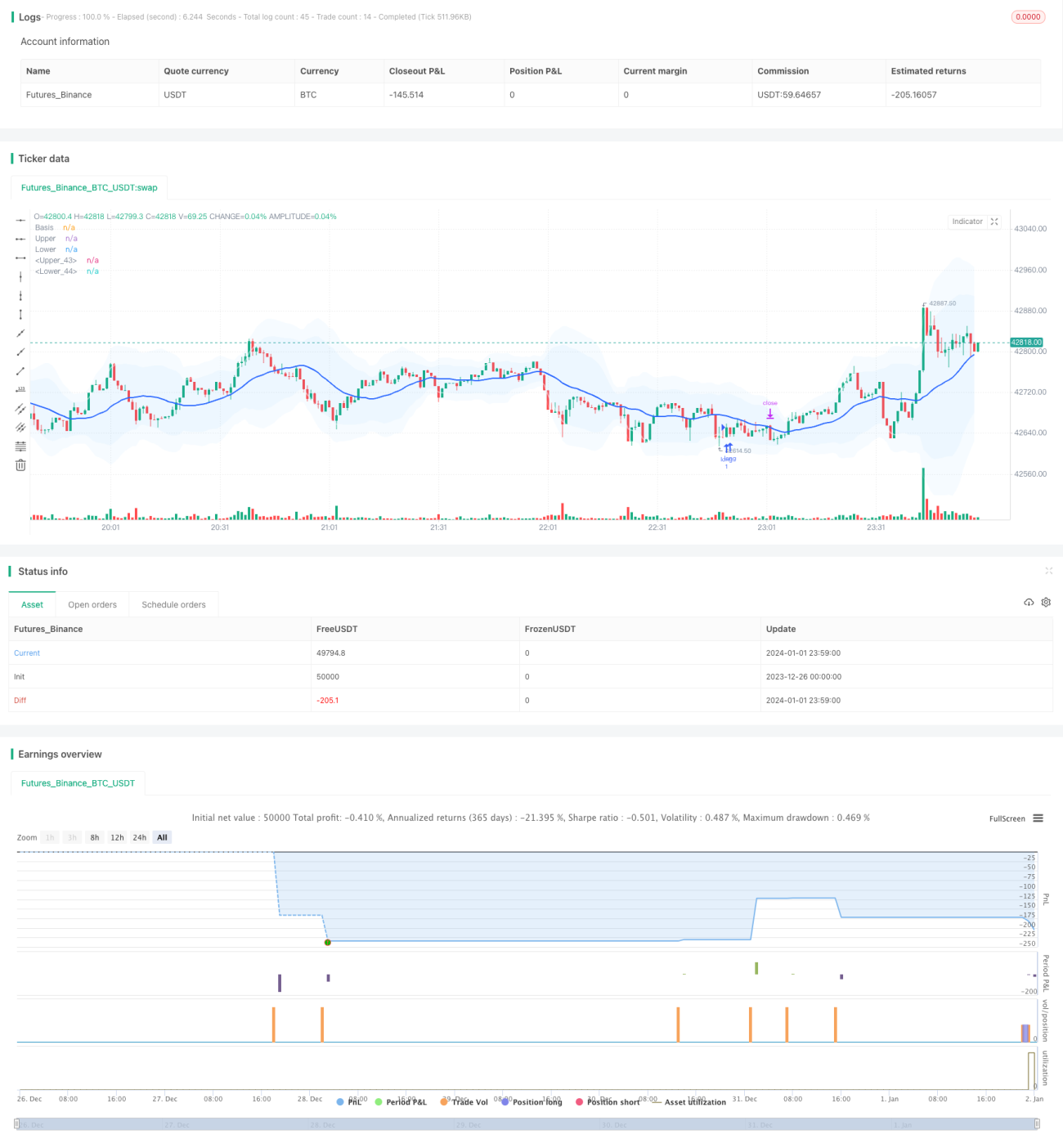

この戦略は、ボリンジャーバンド指標と平均真実範囲(ATR)指標を組み合わせ、トレーリングストップ機能を備えたブレイクアウト取引戦略を形成します。価格が指定された標準偏差のボリンジャーバンドの上限または下限を突き抜けた際に取引シグナルを発します。同時に、ATR指標を使用してストップロスと利食いの水準を計算し、損益比率をコントロールします。さらに、この戦略は時間フィルターやパラメーター最適化などの機能も備えています。

戦略の原理

第一に、中央線、上限線、下限線を計算します。中央線は価格の単純移動平均線(SMA)であり、上限線と下限線は価格の標準偏差の整数倍です。価格が下限線から上方にブレイクした場合にロング、上限線から下方にブレイクした場合にショートを行います。

第二に、ATR指標を計算します。ATR指標は価格の平均的な変動幅を示します。ATRの値に基づいてロングポジションのストップロス水準とショートポジションのストップロス水準を設定します。また、ATRの値に基づいて利食いの水準を設定し、損益比率をコントロールします。

第三に、時間フィルターを使用し、指定された時間帯のみ取引を行うことで、重要なニュースイベントによる急激な変動を回避します。

第四に、トレーリングストップの仕組みです。最新のATRの値に基づいてストップロス水準をリアルタイムで調整し、より多くの利益を確定させます。

優位性の分析

- ボリンジャーバンド指標は価格の中心を反映するため、単一の移動平均線よりも効果的です。

- ATRによるストップロスにより、1トレードあたりの損益比率をコントロールでき、リスクを効果的に管理できます。

- トレーリングストップは市場の変動に応じて自動調整され、より多くの利益を確定できます。

- 戦略のパラメーターが豊富で、カスタマイズされた組み合わせが可能です。

リスク分析

- 相場がレンジで調整する場合、小さな損失が複数回発生しやすくなります。

- ボリンジャーバンドのブレイクアウトによる逆張りは失敗する可能性があります。

- 夜間や重要なニュースの時間帯は取引リスクが高いため、回避する必要があります。

対策:

- リスク管理の原則を厳守し、1トレードあたりの損失を抑制します。

- パラメーターを最適化し、勝率を向上させます。

- 時間フィルターを使用して高リスク時間帯を回避します。

最適化の方向性

- 異なるパラメーターの組み合わせをテストし、設定を最適化します。

- OBVなどの出来高指標を追加してタイミングを図ります。

- 機械学習モジュールを追加して最適化を図ります。

まとめ

本戦略は、ボリンジャーバンド指標を用いてトレンドの中心とブレイク方向を判断し、ATR指標を用いて利食い・ストップロスを計算して損益比率を確保し、さらにトレーリングストップで利益を確定します。戦略の強みは、カスタマイズ性が高く、リスクをコントロールしやすく、短期的なデイトレード(Intraday Trading)に適している点です。パラメーターの最適化や機械学習により、さらに勝率と収益性を高めることが可能です。

- 1