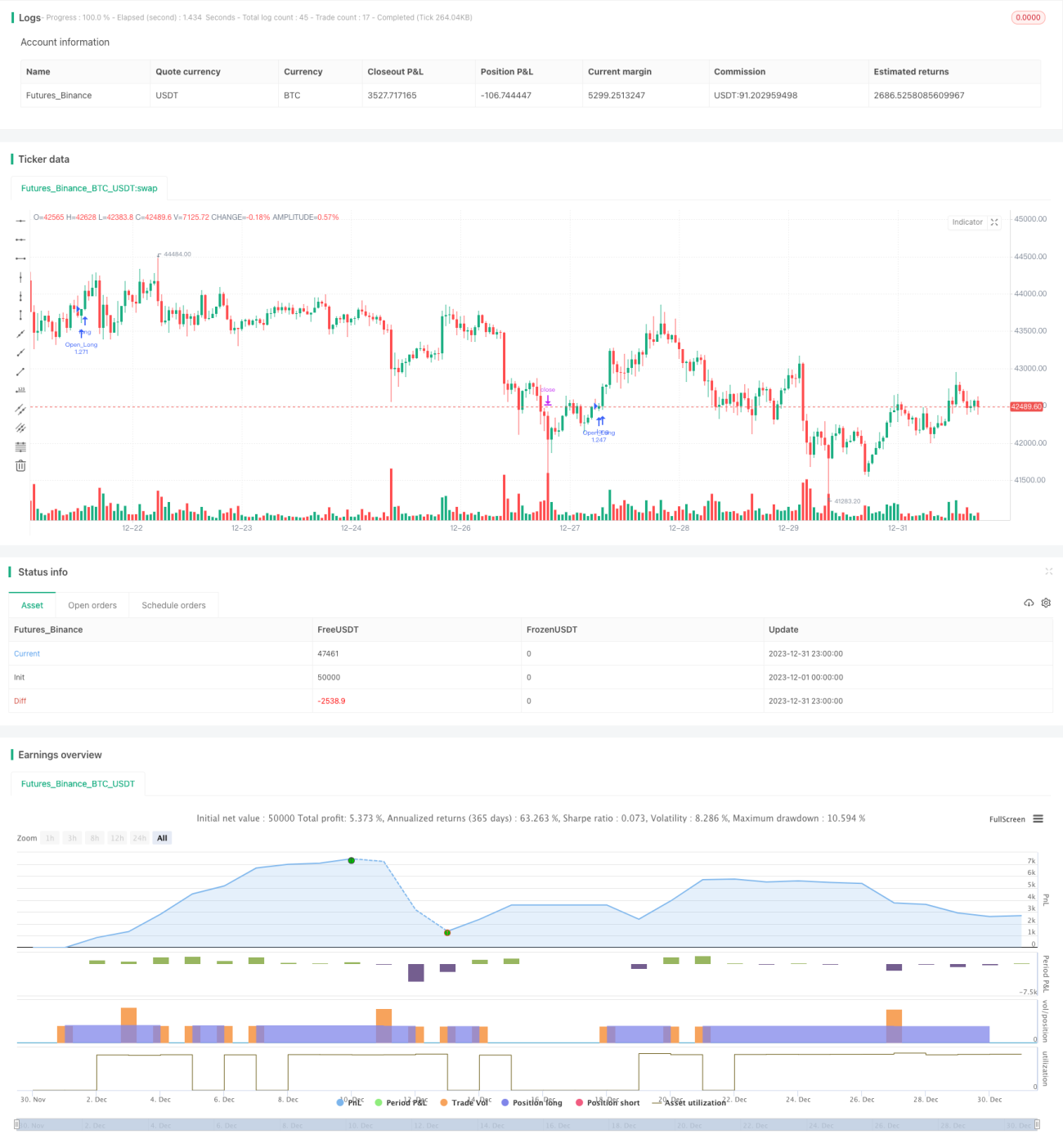

ローソク足に基づくロングブレイクアウト戦略

1

Follow

1802

Followers

概要

本戦略は、シンプルなローソク足パターン判定ルールを設定することで、テスラの4時間足におけるロングブレイクアウト取引を実現します。実装が簡単で、ロジックが明確、理解しやすいという利点があります。

戦略の原理

戦略の核となる判断ロジックは、以下の4つのローソク足パターンルールに基づいています。

- 現在のローソク足の最安値が始値より低い

- 現在のローソク足の最安値が前のローソク足の最安値より低い

- 現在のローソク足の終値が始値より高い

- 現在のローソク足の終値が前のローソク足の始値および終値より高い

上記4つのルールがすべて満たされた場合、買い方向のポジションをオープンします。

さらに、本戦略ではストップロスとテイクプロフィットの水準も設定されており、価格が利確または損切りの条件に達した場合、ポジションをクローズします。

優位性分析

本戦略には以下のような利点があります。

- 使用するローソク足の判定ルールは非常にシンプルかつ直接的で、理解しやすく、実践もしやすい。

- 完全に価格実体に基づいて判断しており、複雑なテクニカル指標を使用していないため、バックテストの結果が直接的である。

- 実装コード量が少なく、実行効率が高く、最適化や改良が容易である。

- パラメータ調整により、ストップロス・テイクプロフィット条件を自由に設定し、リスクをコントロールできる。

リスク分析

注意すべき主なリスクは以下の通りです。

- 固定数量でポジションをオープンしており、ポジション管理を考慮していないため、過剰な取引リスクが存在する可能性がある。

- フィルターが設定されていないため、レンジ相場において無効な取引が多発する可能性がある。

- バックテストデータが不足しているため、戦略の効果判断に偏りが生じる可能性がある。

以下の方法でリスクを軽減できます。

- ポジション管理モジュールを追加し、資金規模に応じて取引数量を動的に調整する。

- 取引フィルター条件を追加し、レンジ相場での無秩序なポジションオープンを回避する。

- より多くの過去データを収集し、バックテスト期間を延長して、結果の信頼性を高める。

最適化の方向性

本戦略の最適化可能な方向性は以下の通りです。

- ポジション管理モジュールを追加し、資金使用率に基づいて取引規模を決定する。

- ストップロス・テイクプロフィットのトレーリングメカニズムを設計し、弾力的なエグジットを実現する。

- 取引フィルターモジュールを追加し、無効な取引を回避する。

- 機械学習手法を活用してパラメータを自動最適化する。

- 複数銘柄のアービトラージ取引をサポートする。

まとめ

本戦略は、シンプルなローソク足パターン判定ルールにより買いブレイクアウト取引を実現しています。改善の余地はあるものの、シンプルさと直接性の観点から、初心者が理解し使用するのに非常に適したロング戦略です。継続的な最適化により、戦略の効果をより一層高めることができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1