クアントマスター専用マルチレベル移動平均クロス戦略

概要

本戦略は、多段階の移動平均線のクロス原理を活用し、中長期的なトレンドを捉え、安定した利益を実現します。戦略では、異なるパラメータを持つ高速、中速、低速の3組の移動平均線を使用し、それらのクロス状況に基づいて売買判断を行います。この多段階移動平均線クロス戦略は、従来の2組のみの移動平均線戦略と比較して、より多くの偽シグナルをフィルタリングし、勝率を向上させることができます。

戦略原理

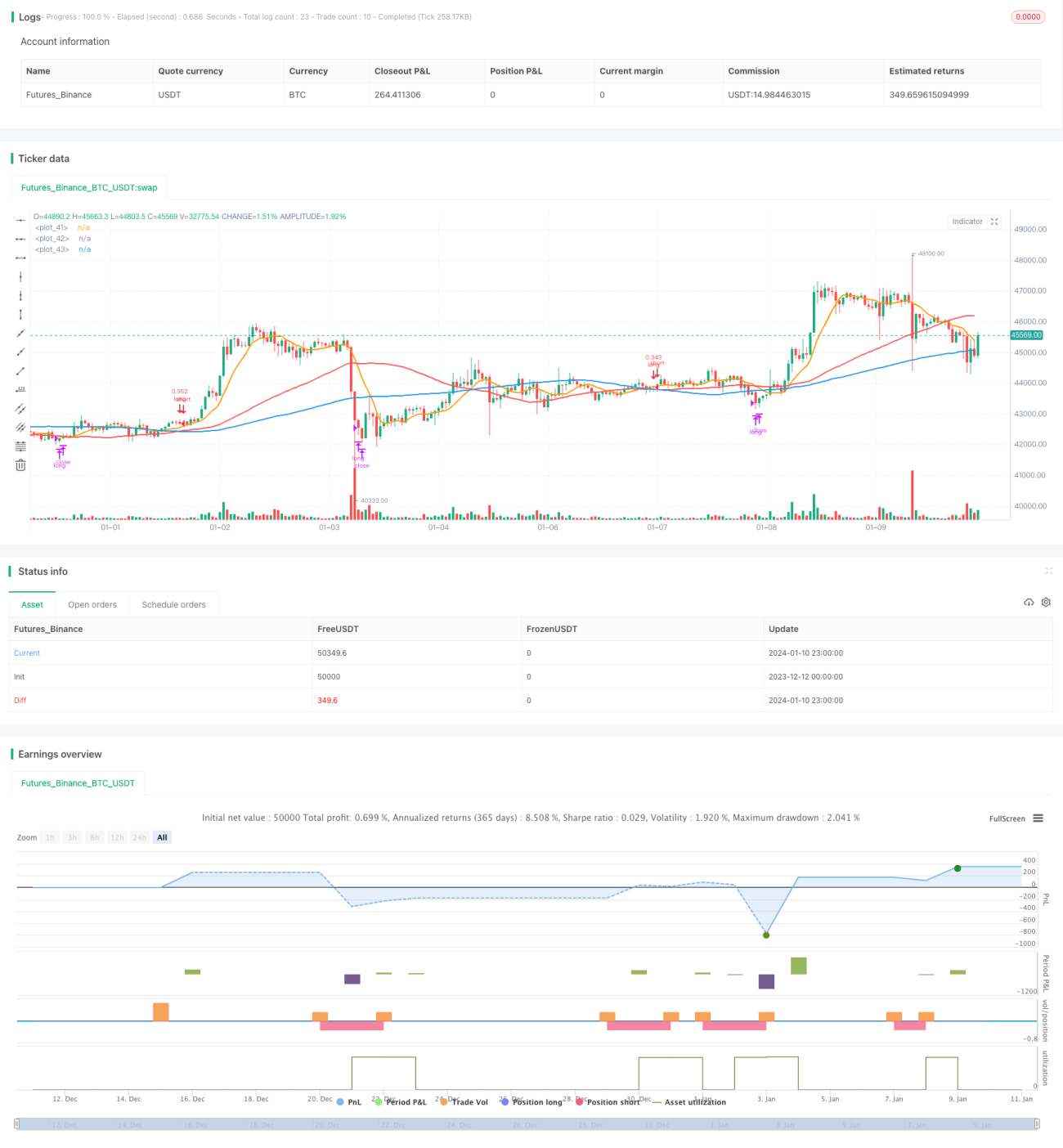

本戦略では、3組の移動平均線を使用します。高速移動平均線(MAshort)、中速移動平均線(MAmid)、低速移動平均線(MAlong)です。MAshortのパラメータは9で、最も反応が速く、短期シグナルを捉えるために使用します。MAmidのパラメータは50で、速度は中程度であり、トレンドを確認するために使用します。MAlongのパラメータは100で、最も反応が遅く、長期トレンドの方向性を判断するために使用します。

戦略の具体的な取引ロジックは以下の通りです。中速移動平均線(MAmid)が低速移動平均線(MAlong)を上抜けた場合、株価の上昇モメンタムが形成されていることを示すため、この時点で買いポジションを取ります。高速移動平均線(MAshort)が中速移動平均線(MAmid)を下抜けた場合、短期トレンドに転換が生じたことを示すため、この時点でポジションを決済します。

本戦略の最大の利点は、複数の移動平均線を組み合わせてマッチングすることで、偽シグナルを効果的にフィルタリングし、中長期的な上昇トレンドの中で比較的力強いブレイクアウトのみを選択して買いポジションを構築できる点です。

優位性分析

本戦略には以下の優位性があります。

- 戦略パラメータは最適化されており、中長期的なトレンドに効果的にマッチし、勝率が高い。

- 多段階の移動平均線設計により、ノイズや偽シグナルをフィルタリングできる。

- 様々な株式や暗号通貨に適用可能で、過去のバックテスト結果が良好。

- 取引頻度が高くなく、1回のポジション構築で資金の30%を利用するため、リスクは管理可能。

- 時間周期を設定可能で、実運用における柔軟性が高い。

リスク分析

本戦略には以下のリスクも存在します。

- 長期トレンドが突然転換する確率は低いが、発生した場合のストップロス幅が大きくなる可能性がある。

- 取引頻度が高くないため、資金利用率がある程度低下する問題がある。

- 戦略パラメータは異なる取引銘柄に応じて最適化する必要があり、適用範囲が限定される可能性がある。

上記のリスクに対し、本戦略の適用範囲をさらに拡大するとともに、ストップロス技術を組み合わせて最大ドローダウンをコントロールします。中長期トレンドに転換が生じた場合には、ポジションサイズを縮小することで対応します。

最適化の方向性

本戦略は以下の点からさらに最適化が可能です。

- 移動平均線の期間パラメータを最適化し、より優れたパラメータ組み合わせを探す。

- 出来高の指標を追加して確認を行い、カーブフィッティングの問題を回避する。

- 戦略の最大損失値を設定する。例えば最大ドローダウンを20%とし、強制ストップロスを実施する。

- 機械学習モデルを追加してトレンドを判断し、戦略の自己適応能力を向上させる。

まとめ

本戦略は典型的な中長期定量戦略であり、多段階の移動平均線をマッチングすることで長期的なトレンドを捉え、取引リスクをコントロールしつつ継続的に利益を上げます。単一指標と比較して、本戦略は複数のパラメータを統合することで、強力な中長期トレンドシグナルを効果的に識別できます。さらなる最適化により、本戦略はより多くの銘柄に適用可能となり、定量取引の分野で重要な役割を果たすことが期待されます。

- 1