モメンタム指標と恐怖指数のクロス戦略

1

Follow

1802

Followers

概要

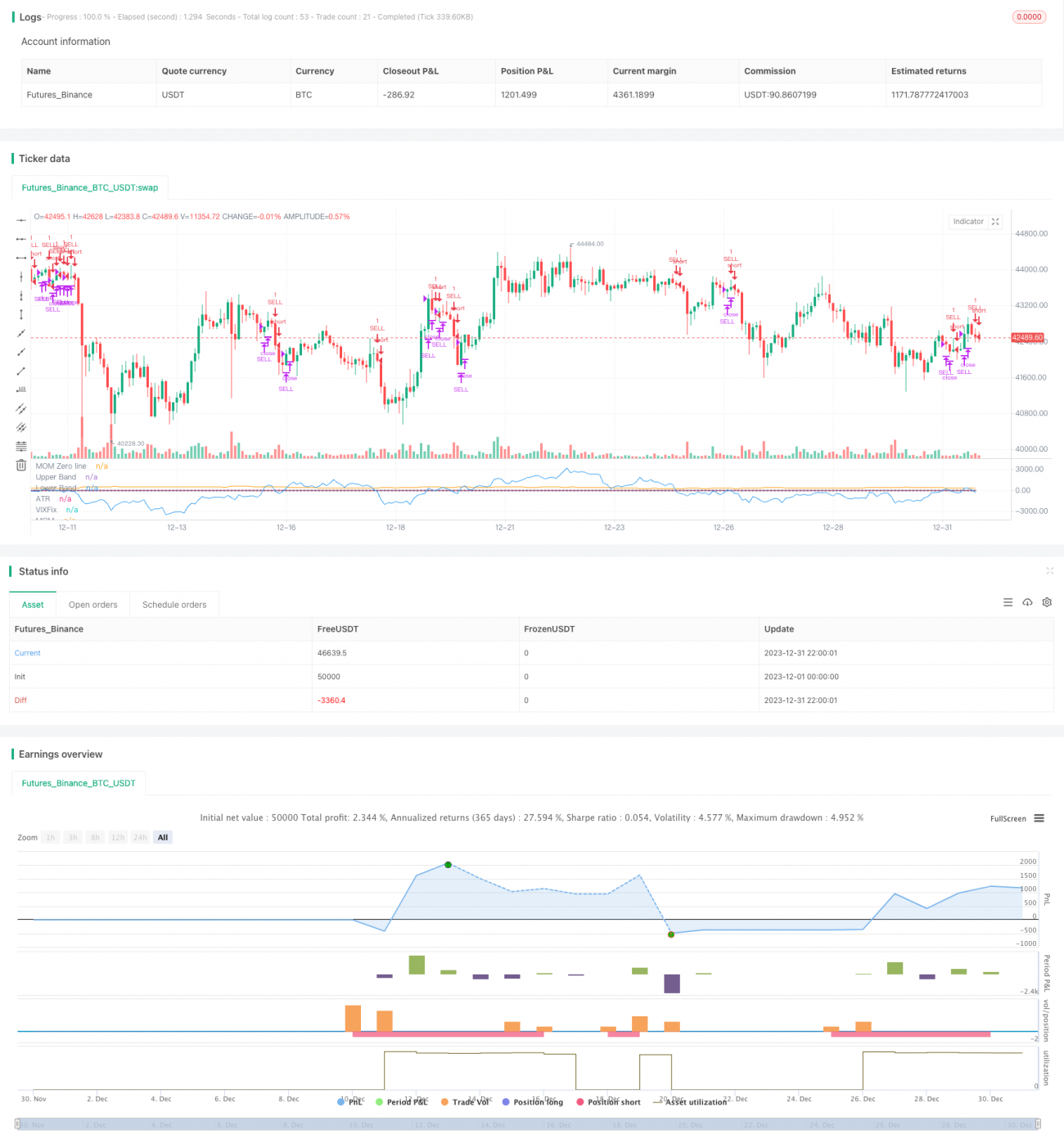

本戦略は、モメンタム指標と恐怖指数のクロスを計算して市場の動向を判断し、特定のクロスが発生した際に売りシグナルを出力することで、大幅な下落相場を捉えることを目的としています。

戦略の原理

- 50期間のモメンタム指標を計算します。これは現在の価格が50期間前と比べてどれだけ変化したかを示します。

- 22期間の恐怖指数補正値を計算します。これは最高値と最安値の比率を用いて市場の恐怖感を示します。

- モメンタム指標が恐怖指数を下回った場合、市場に下落圧力が存在することを示します。

- モメンタム指標がさらに下落し危険域(-5から5の間)に入った場合、強い売りシグナルが発せられます。

優位性分析

- 市場の取引心理指標である恐怖指数を利用することで、市場の構造的変化を効果的に判断できます。

- モメンタム指標は価格変動の速度と勢いを判断でき、市場トレンドの変化を補助的に判断できます。

- 異なる種類の指標を組み合わせることで、突発的な事象を識別する精度を高めることができます。

- パラメータを調整することで、異なる市場環境に柔軟に対応できます。

リスク分析

- 恐怖指数とモメンタム指標のクロスが毎回大幅な下落を保証するわけではありません。最終判断には他の指標を総合する必要があります。

- 売り後にストップロスを設定していないため、損失を効果的に抑制できません。

- 反転や再エントリーの問題が考慮されていません。本戦略は突発的な下落を捉えることのみを目的としています。

改善点

- 売り後にストップロスポイントを設定し、損失を抑制します。

- 出来高やボリンジャーバンドなど他の指標を追加し、シグナルの信頼性を高めます。

- 再エントリーのシグナルを追加し、戦略が長期的なサイクルで完全に運用できるようにします。

- パラメータを最適化し、最適なパラメータの組み合わせを見つけます。

まとめ

本戦略は、モメンタム指標と恐怖指数のクロスを利用して市場の下落警告を発します。突発的な下落を効果的に捉えることができますが、短期的な用途にのみ適しており、退出メカニズムやリスク管理が欠けています。今後はさらなる改良を加え、長期的に持続可能な戦略へと発展させる必要があります。

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © gary_trades

//THIS SCRIPT HAS BEEN BUIL TO BE USED AS A S&P500 SPY CRASH INDICATOR (should not be used as a strategy).Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1