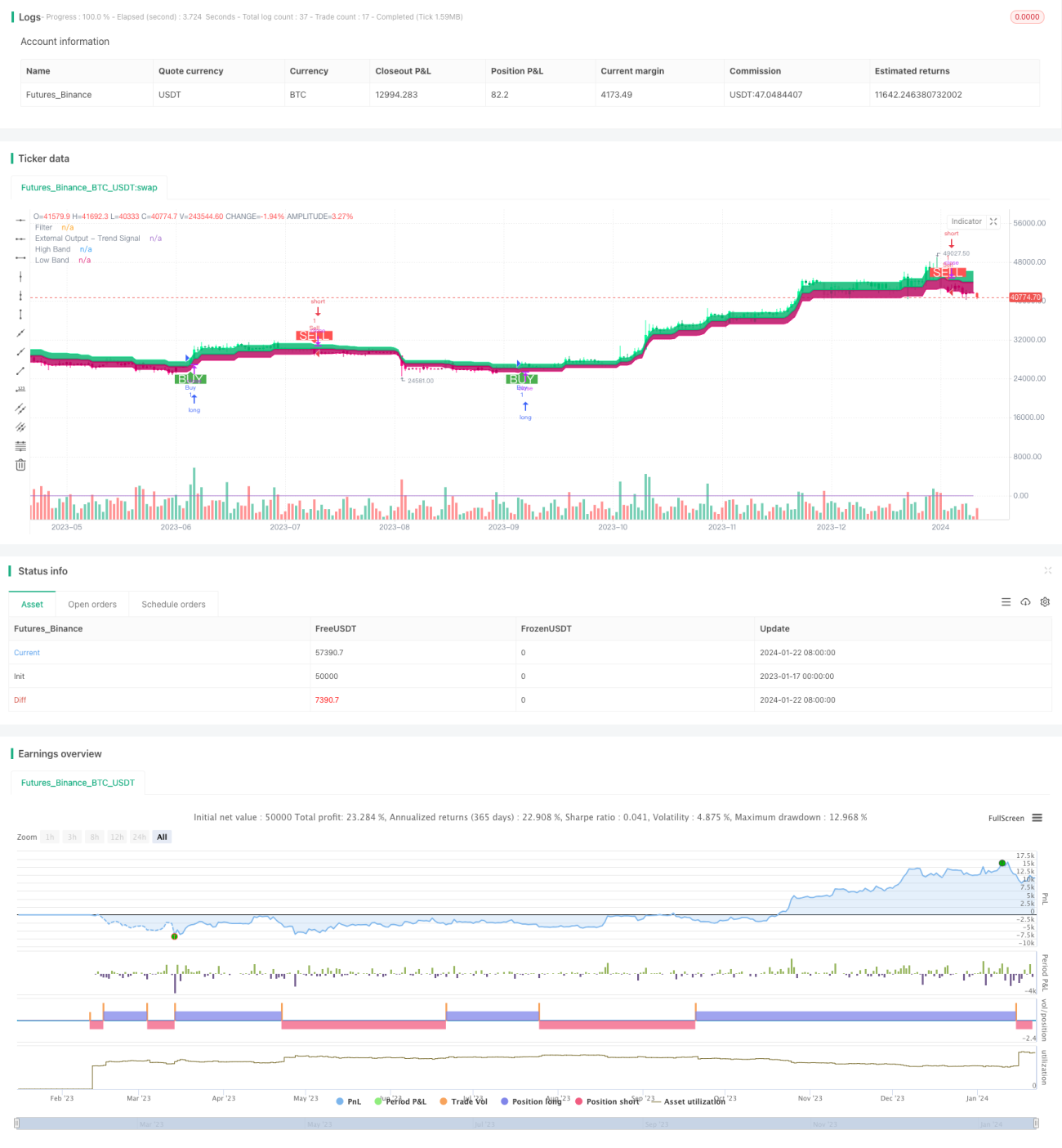

双方向適応範囲フィルターモメンタムトラッキング戦略

1

Follow

1802

Followers

概要

この戦略は、双方向適応型レンジフィルターモメンタム追跡戦略です。適応型レンジフィルターを用いて価格変動を追跡し、出来高指標と組み合わせて価値の方向性を判断し、安値で買い高値で売ることを実現します。

戦略原理

- 適応型レンジフィルターを使用して価格変動を追跡します。フィルターサイズはユーザーが設定したレンジ周期、数量、規模に基づいて適応的に調整されます。

- フィルターはType 1とType 2の2種類があります。Type 1は標準レンジ追跡型、Type 2は階段丸め型です。

- フィルターと終値の大小関係に基づいて価格変動の方向を判断します。価格が上限ラインを上回れば強気、下限ラインを下回れば弱気とします。

- 前日比の終値の上昇/下降関係と組み合わせて、価値の方向を判断します。価値が上昇すればロング、下降すればショートとします。

- 価格が上限ラインを突破し、かつ価値が上昇している場合に買いシグナルを発出し、価格が下限ラインを割り込み、かつ価値が下降している場合に売りシグナルを発出します。

優位性分析

- 適応型レンジフィルターは市場の変動を正確に捉えることができます。

- 2種類のフィルターにより、異なる取引嗜好に対応できます。

- 出来高指標と組み合わせることで、価値の方向性を効果的に識別できます。

- 戦略は柔軟で、市場に応じてパラメータを調整できます。

- 適切な取引条件ロジックをカスタマイズして選択できます。

リスク分析

- パラメータ設定が不適切だと、過剰取引や機会損失につながる可能性があります。

- ブレイクアウトシグナルには一定の遅延が生じます。

- 出来高指標には一定のラグリスクがあります。

- レンジブレイクアウトは容易に逆張りリスクに直面します。

リスク対策:

- 適切なパラメータ組み合わせを選択し、適宜調整します。

- 他の指標と組み合わせてトレンドを識別します。

- 重要な価格帯付近やトレンド反転時には慎重に取引します。

最適化の方向性

- 異なるレンジサイズと平滑化周期のパラメータ組み合わせをテストし、最適な組み合わせを見つけます。

- 異なるフィルタータイプを試し、個人の好みに合ったものを選択します。

- 他の出来高指標や補助的なテクニカル指標を試行します。

- 取引条件ロジックを最適化・調整し、非合理的な取引を減らします。

- 市場のフラクタル理論と組み合わせて、適応的なポジション調整比率を設定します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1