トレンド追跡ストップロス・利益確定戦略

1

Follow

1802

Followers

概要

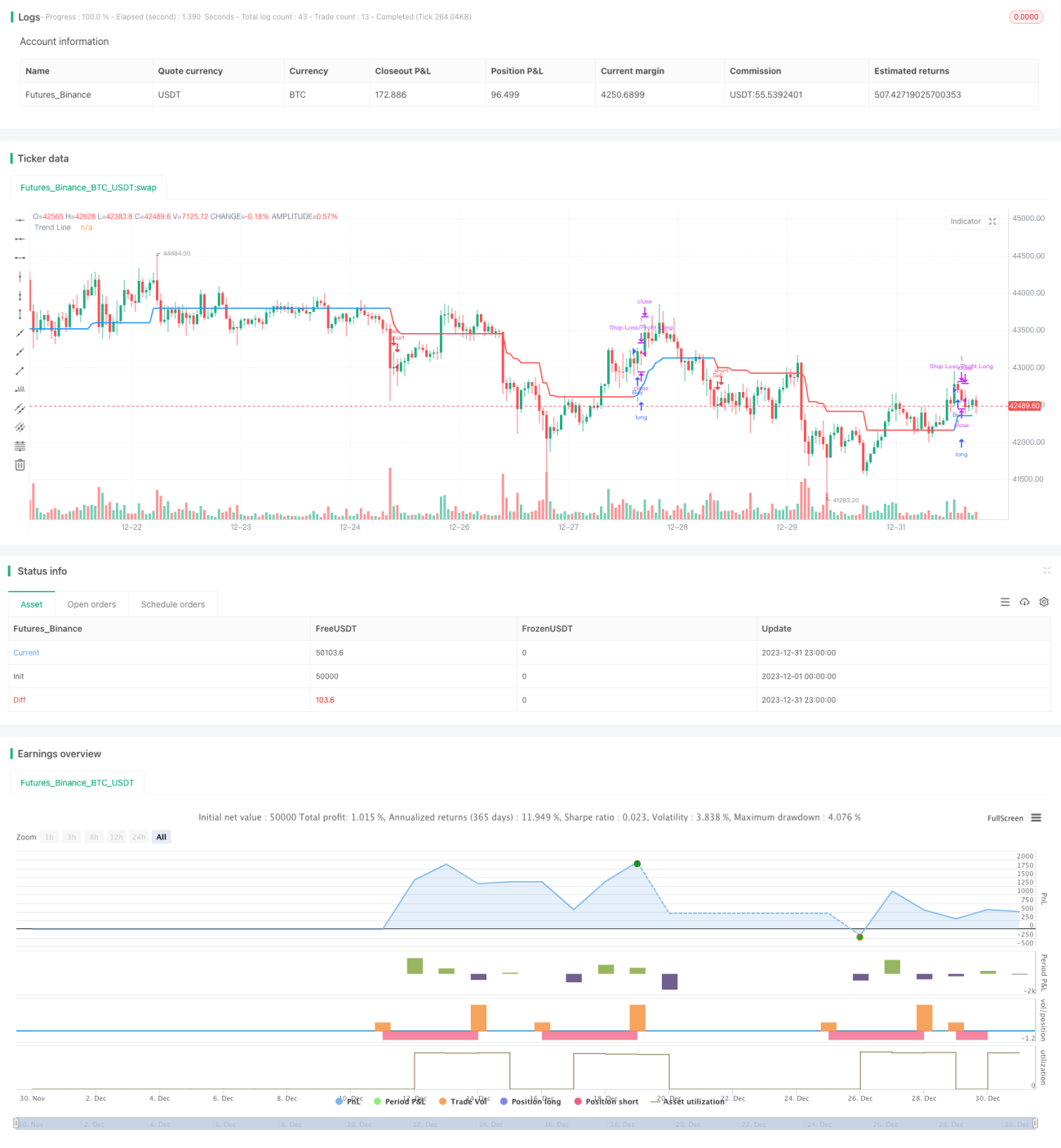

これは、ボリンジャーバンドを用いてトレンドを判断し、ATRインジケーターを利用してストップロスと利確を設定するトレンドフォロー戦略です。まず市場のトレンドを判断し、ENVIRONMENTラインを算出し、ポジションクローズ時にストップロス・利確ポイントを設定します。

戦略の原理

- ボリンジャーバンドの上限線と下限線を計算します。

- 終値が上限線を上回っているか、下限線を下回っているかを判断します。該当する場合はトレンド市場とみなし、それぞれロング市場とショート市場とします。

- トレンド市場の場合、環境線を計算します。環境線は、最安値からATRを引いた値(ロング市場)、または最高値にATRを足した値(ショート市場)に基づきます。

- トレンド市場でない場合、環境線は前のローソク足の環境線と同じ値を維持します。

- ENVIRONMENTラインを比較してトレンド方向を判断します。上昇していればロング、下落していればショートとします。

- ENVIRONMENTラインの方向が転換した時点で、買い/売りシグナルを発生させます。

- ストップロスと利確を設定します。固定ストップロス距離はエントリー価格の100倍、変動利確距離はエントリー価格の1.1倍(ロング)または0.9倍(ショート)とします。

優位性分析

- 市場のトレンドを判断できるため、偽のブレイクアウトによる取引を減らせます。

- ENVIRONMENTラインを設定することで、相場に巻き込まれるのを防ぎます。

- ストップロスと利確が適切に設定されており、利益を確保しつつリスクをコントロールできます。

リスク分析

- パラメータ設定が不適切だと、取引機会を逃す可能性があります。

- ボリンジャーバンドはレンジ相場において誤った判断をする確率が高くなります。

- ストップロスが近すぎると、瞬時にやられてしまう可能性があります。

最適化の方向性

- ボリンジャーバンドのパラメータを最適化し、異なる銘柄に適応できるようにします。

- ENVIRONMENTラインの計算方法を最適化します(他のインジケーターの導入など)。

- ストップロスと利確のパラメータ設定をテストし、最適化します。

まとめ

この戦略は、ボリンジャーバンドでトレンドを判断し、ENVIRONMENTラインを使用してストップロス・利確を設定するものです。主な利点は、トレンドの判断が明確で、ストップロス・利確の設定が合理的であり、リスクを効果的に管理できる点です。主なリスクは、ボリンジャーバンドによるトレンド判断の誤りと、ストップロスが近すぎることです。今後の最適化の方向性としては、パラメータ最適化、ENVIRONMENTラインの計算方法の改善、ストップロス・利確の最適化などが挙げられます。

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © zhuenrong

// © DreadblitzStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1