ブルマーケット追跡システム

概要

強気相場追跡システムは、トレンドフォローに基づく機械的な取引システムです。4時間足チャートのトレンド指標を利用して取引シグナルをフィルタリングし、エントリーは15分足チャートの指標に基づいて判断します。主な指標はRSI、ストキャスティクス、MACDです。このシステムの利点は、マルチタイムフレームの組み合わせにより偽のシグナルを効果的に除去できる一方、より低い時間軸の指標を利用して精度の高いエントリータイミングを得られる点です。ただし、過剰取引や偽のブレイクアウトを引き起こしやすいといったリスクも存在します。

原理

このシステムの核となるロジックは、異なる時間軸の指標を組み合わせてトレンド方向とエントリータイミングを特定することです。具体的には、4時間足チャートのRSI、ストキャスティクス、EMAがすべて条件を満たすことで全体のトレンド方向を判断します。これにより、ほとんどのノイズを効果的に除去できます。同時に、15分足チャートのRSI、ストキャスティクス、MACD、EMAも同じ方向で強気または弱気を示すことで、具体的なエントリータイミングを決定します。これにより、良好な買い・売りポイントを見つけることができます。4時間足と15分足の判断が一致した場合にのみ、このシステムは取引シグナルを発出します。

利点

- マルチタイムフレームの組み合わせにより、偽のシグナルを効果的にフィルタリングし、主要トレンドを識別できる

- 15分足の詳細指標により、精度の高いエントリータイミングを取得可能

- RSI、ストキャスティクス、MACDなどの主要なテクニカル指標を組み合わせて使用するため理解しやすく、最適化も容易

- mStop利益確定、損切り、トレーリングストップなどの厳格なリスク管理手段を採用しており、1回の取引リスクを効果的にコントロールできる

リスク

- 過剰取引リスク。短期的な時間軸に敏感なため、多数の取引シグナルが発生し、過剰取引につながる可能性がある

- 偽のブレイクアウトリスク。短期指標の判断が誤判定を起こし、偽のブレイクアウトシグナルを発生させる可能性がある

- 指標の無効化リスク。テクニカル指標自体に一定の限界があり、極端な相場では機能しなくなる可能性がある

対応策として、以下の観点からシステムを最適化できる:

- 指標パラメータを調整し、異なる市場環境に適応させる

- フィルタリング条件を追加し、取引頻度を減らして過剰取引を防止する

- 利益確定・損切りの戦略を最適化し、市場の変動幅に合わせる

- 異なる指標の組み合わせ案をテストし、最適解を探す

まとめ

強気相場追跡システムは、全体として非常に実用的なトレンドフォロー機械取引システムです。マルチタイムフレームの組み合わせ指標を利用して相場トレンドと重要なエントリータイミングを識別します。適切なパラメータ設定と継続的な最適化テストにより、このシステムはほとんどの相場環境に適応し、安定した収益を達成できます。ただし、潜在的なリスクを認識し、積極的な対策を講じてこれらのリスクを予防・緩和することも重要です。

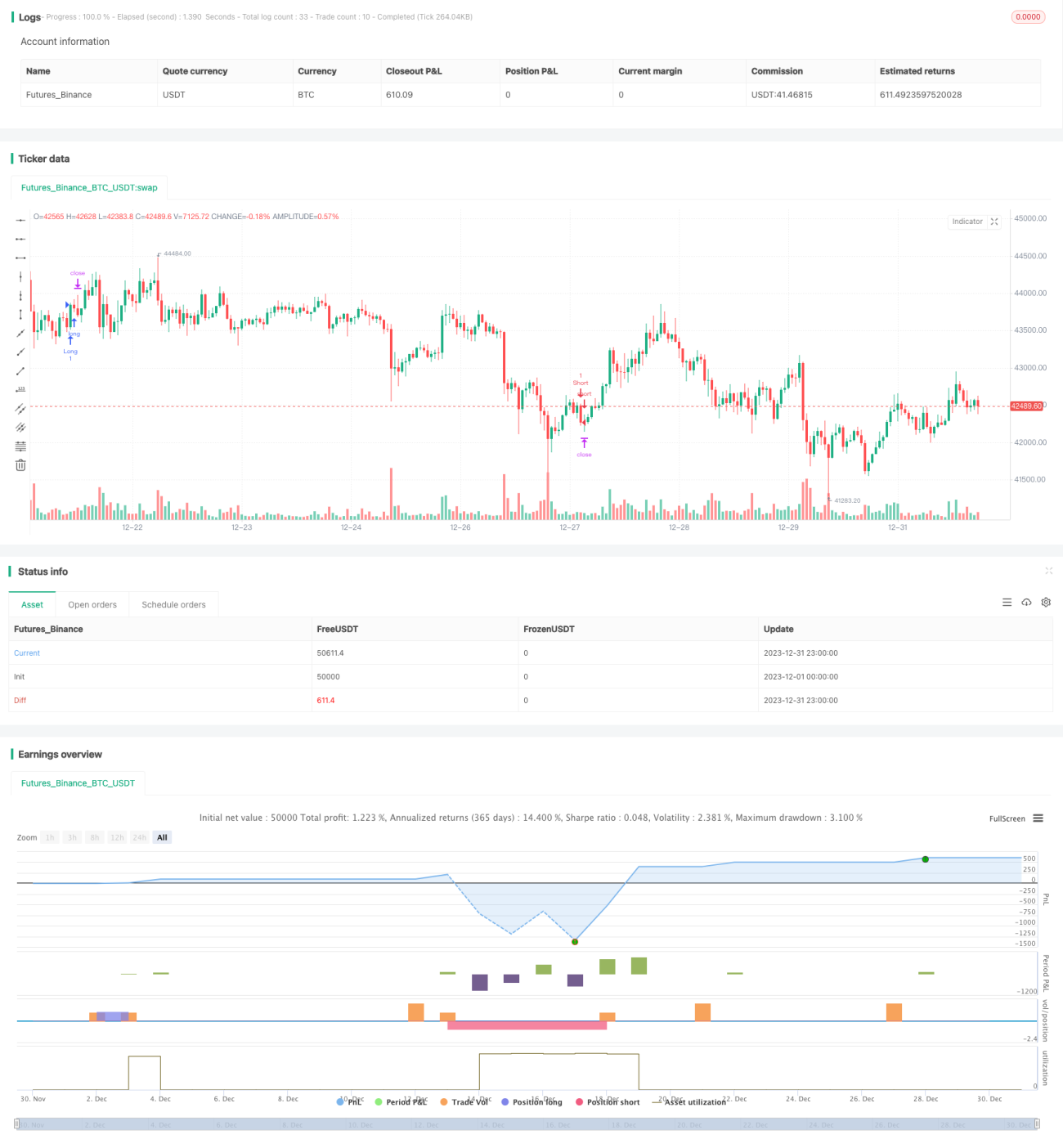

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Cowabunga System from babypips.com", overlay=true)

// 4 Hour Stochastics

length4 = input(162, minval=1, title="4h StochLength"), smoothK4 = input(48, minval=1, title="4h StochK"), smoothD4 = input(48, minval=1, title="4h StochD")- 1