二重移動平均線トレンドフォロー戦略

概要

デュアル移動平均線トレンドフォロー戦略(Dual Moving Average Trend Tracking Strategy)は、短期移動平均線と長期移動平均線の組み合わせでトレンド方向を判断し、さらにローソク足の実体色をエントリーシグナルとして用いる定量取引戦略です。この戦略は、トレンドフォローと逆張り取引の両方の特徴を持ち合わせています。

戦略の原理

本戦略では、期間20の長期移動平均線を用いて全体的なトレンド方向を判断し、価格が上抜けた場合は上昇トレンド、下抜けた場合は下降トレンドと見なします。同時に、期間5の短期移動平均線をエントリーフィルターとして活用し、価格が短期移動平均線をブレイクした場合にのみ取引シグナルを発します。さらに、直近N本のローソク足の実体色をチェックし、実体色が連続して赤(陽線)である場合に上昇トレンドと組み合わせてロングシグナル、連続して緑(陰線)である場合に下降トレンドと組み合わせてショートシグナルを発することで、フェイクアウトを防止します。

本戦略は、全体トレンド、短期移動平均線、ローソク足実体という3つの次元の情報を総合的に判断することで、取引シグナルの信頼性を高めています。3つの方向が一致した場合にのみ取引シグナルを発し、ノイズの一部を効果的にフィルタリングします。

戦略の優位性

-

トレンドフォローと逆張り取引の両方の特性を持ち、異なる市場環境に適応できます。

-

取引シグナル発生前に多次元の判断を行うため、偽シグナルを効果的にフィルタリングし、勝率を向上させます。

-

パラメータ最適化の余地が大きく、移動平均線の期間やローソク足実体色の判定本数などを調整することで最適化が可能です。

-

戦略ロジックが明確かつシンプルで理解しやすく、初心者の学習に適しています。

戦略のリスク

-

大幅なレンジ相場では連敗(osing streak)が発生しやすく、大きなドローダウンを招く可能性があります。移動平均線のパラメータを調整するか、ストップロスを導入することで回避できます。

-

ボックス相場ではワーソー(whipsaw)が発生しやすく損失を生む可能性があります。ローソク足実体色の判定本数を調整するか、逆張り取引をオフにすることで対処できます。

-

パラメータ設定が適切であることを確認するために十分なバックテストが必要で、適切でない場合は戦略のパフォーマンスに大きな影響を与えます。

最適化の方向性

-

異なる種類の移動平均線(指数移動平均線、カウフマン適応移動平均線など)を試す。

-

取引数量管理の追加(固定数量、または口座資産に応じた調整など)。

-

ストップロス機構の追加。価格が再び長期移動平均線を下抜けた場合にストップロスで撤退することも検討。

-

異なる銘柄でテストし、戦略の安定性と適応性を判断する。

まとめ

デュアル移動平均線トレンドフォロー戦略は、トレンド判断と逆張り取引を組み合わせることで、中長期トレンドを効果的に捉えるだけでなく、短期でも追加収益を得ることが可能です。パラメータ最適化とメカニズム強化により、さらに利益の幅を拡大できます。本戦略のロジックはシンプルかつ明確で、初心者の学習研究に非常に適しています。ただし、あらゆる戦略は異なる銘柄とパラメータで十分に検証し、その安定性と収益性を確保する必要があります。

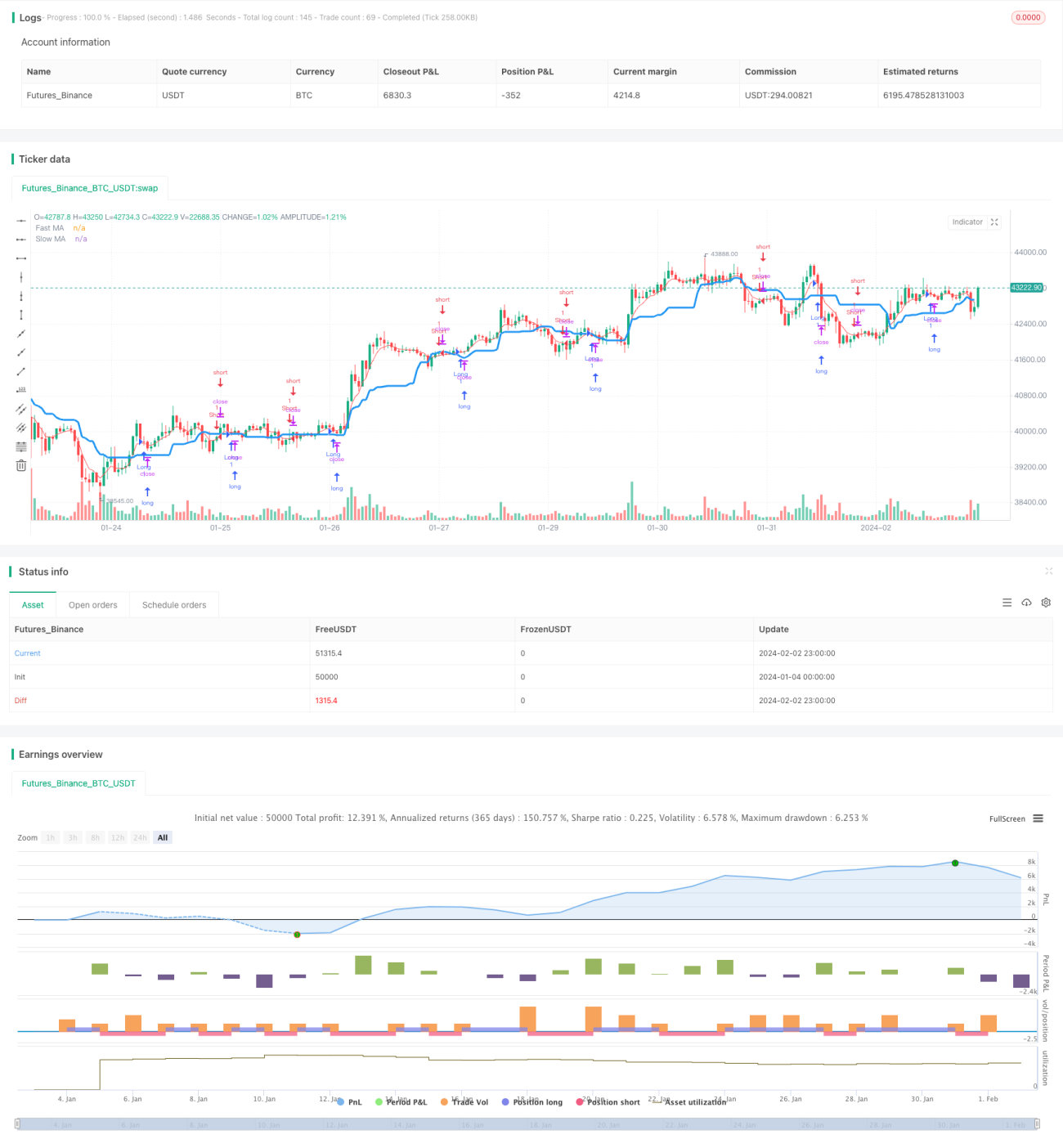

/*backtest

start: 2024-01-04 00:00:00

end: 2024-02-03 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title = "Noro's Trend MAs 1.5", shorttitle = "Trend MAs 1.5", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value=100.0, pyramiding=0)

//Settings- 1