ダイナミック移動平均線クロス・トレンド戦略

1

Follow

1802

Followers

概要

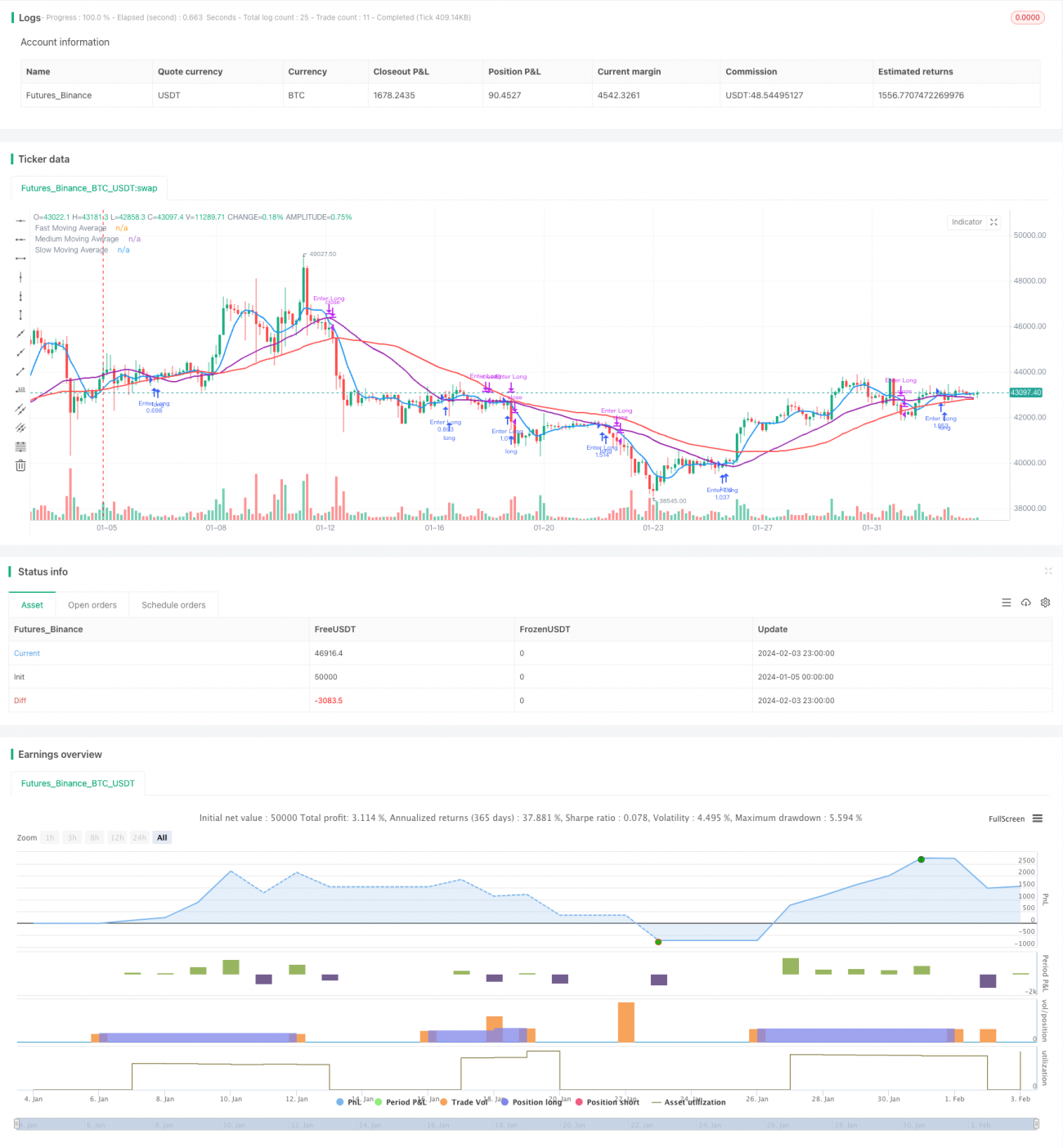

この戦略は、暗号通貨市場に適用可能な単純移動平均線(SMA)クロスオーバー戦略です。高速、中速、低速の3つのSMAを利用して、潜在的なエントリーとエグジットのシグナルを特定します。高速SMAが中速SMAを上抜けした場合に買いシグナル、高速SMAが中速SMAを下抜けした場合に売りシグナルが発生します。

戦略の原理

パラメータ設定

この戦略では、トレーダーが以下の主要パラメータを設定できます。

- 価格データソース:終値またはその他の価格

- 不完全なローソク足を考慮するかどうか

- SMA予測方法:シフト予測または線形回帰予測

- 高速SMA期間:デフォルト7

- 中速SMA期間:デフォルト30

- 低速SMA期間:デフォルト50

- 口座資金

- 1トレードあたりのリスク割合

SMA計算

ユーザーが設定したSMA期間に基づき、高速SMA、中速SMA、低速SMAをそれぞれ計算します。

取引シグナル

高速SMAが中速SMAを上抜けした場合に買いシグナル、高速SMAが中速SMAを下抜けした場合に売りシグナルが発生します。

リスクとポジション管理

口座資金と1トレードあたりのリスク割合を組み合わせて、1トレードあたりの想定元本を計算します。さらにATRを利用してストップロス幅を計算し、最終的に1トレードあたりの具体的なポジションサイズを決定します。

優位性分析

- 複数のSMAを使用してトレンドを識別するため、判断力が向上

- SMA予測方法が選択可能で、適応性が高い

- 取引シグナルがシンプルで明確、実行が容易

- リスク管理とポジション管理を統合し、より科学的

リスク分析

- SMA自体の遅延性により、価格の反転ポイントを見逃す可能性がある

- テクニカル指標のみを考慮し、ファンダメンタルズを組み合わせていない

- 突発的なイベントの影響を考慮していない

SMA期間を適切に短縮したり、他の指標を補助として使用するなどして最適化できます。

最適化の方向性

- 他の指標を組み合わせて誤シグナルをフィルタリング

- ファンダメンタルズ判断を追加

- SMA期間パラメータの最適化

- リスクとポジション計算パラメータの最適化

まとめ

本戦略は、SMAクロスオーバー判断、リスク管理、ポジション最適化の複数の機能を統合した、暗号市場に適したトレンドフォロー戦略です。トレーダーは自身の取引スタイルや市場環境などに応じてパラメータを調整し、最適化を実施できます。

Source

Pine

/*backtest

start: 2024-01-05 00:00:00

end: 2024-02-04 00:00:00

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Onchain Edge Trend SMA Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Configuration ParametersStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1