RSI指標と価格ブレイクアウトを組み合わせた短期戦略

1

Follow

1802

Followers

概要

本戦略はRSIインジケーターと価格ブレイクを組み合わせ、一定のトレンド下で形成されるレンジ内でローテーション機会を探り、短期売買を行うことで高効率な短期利益を追求します。

戦略の原理

- RSIインジケーターの判断:RSIが売られすぎライン30を下回ったときに買いシグナルを発生させ、潜在的な反転の買いポイントとします。RSIが買われすぎライン60を上回ったときに売りシグナルを発生させ、利益を確定します。

- ウィンドウ制限:指定されたバックテスト時間ウィンドウ内でのみ有効とし、戦略の効果を制限して全体的な裁定を防ぎます。

- ブレイク判断:価格動向と組み合わせてブレイクの機会を探り、戦略の実際の効果を高め、不必要な空回りを防ぎます。

そのため、本戦略は複数の次元の判断ロジックを統合し、一定のトレンドとブレイク機会の下で、RSIインジケーターによる売買シグナルを利用して短期利益を得るローテーション操作を行います。市場の短期的な売られすぎからの反発や買われすぎからの下落の機会を効果的に捉えることができます。

優位性分析

- 複数のロジック判断を組み合わせることで、単純なRSI戦略と比較してより厳密であり、双方向の空回りによる不要な損失を効果的に回避できます。

- RSIインジケーターを使用して局所的な極値領域を判断し、反転の機会を探して利益を得ます。

- バックテスト時間ウィンドウを設定することで、特定の市場相場に対して検証と最適化を行い、戦略の実際の有用性を高めます。

- 短期利益を追求し、トレンドの転換を予測する必要がないため、把握しやすくリスクを低減します。

リスクと解決方法

- 全体のトレンド方向を直接判断できないため、人手による大局分析が必要です。

- RSIインジケーターは価格変動に遅れて反応するため、最適な売買ポイントを逃す可能性があります。

- 戦略が適用される大きな相場環境を十分に理解する必要があります。

- より多くのテクニカルインジケーターを導入して大トレンドを判断し、戦略パラメーターを最適化することで、戦略の柔軟性を高めることができます。

最適化の方向性

- 大トレンドの判断を追加し、長期間含み損となるポジションを回避します。

- RSIパラメーターを調整し、買われすぎ/売られすぎラインを最適化して効果を高めます。

- ストップロスロジックを追加します。

- バックテストウィンドウ範囲を最適化し、戦略を実際の相場により適合させます。

まとめ

本戦略はRSIインジケーターを使用して買われすぎ/売られすぎの短期的な反転機会を判断し、価格ブレイクと組み合わせて短期利益を得るローテーション操作を行います。特徴は短期効率の追求、操作のシンプルさ、限定されたリスクであり、特定の相場状況下で短期トレーダーに非常に適しています。全体の大トレンドを判断し、パラメーターなどを最適化することで、より良い結果を得る必要があります。

Source

Pine

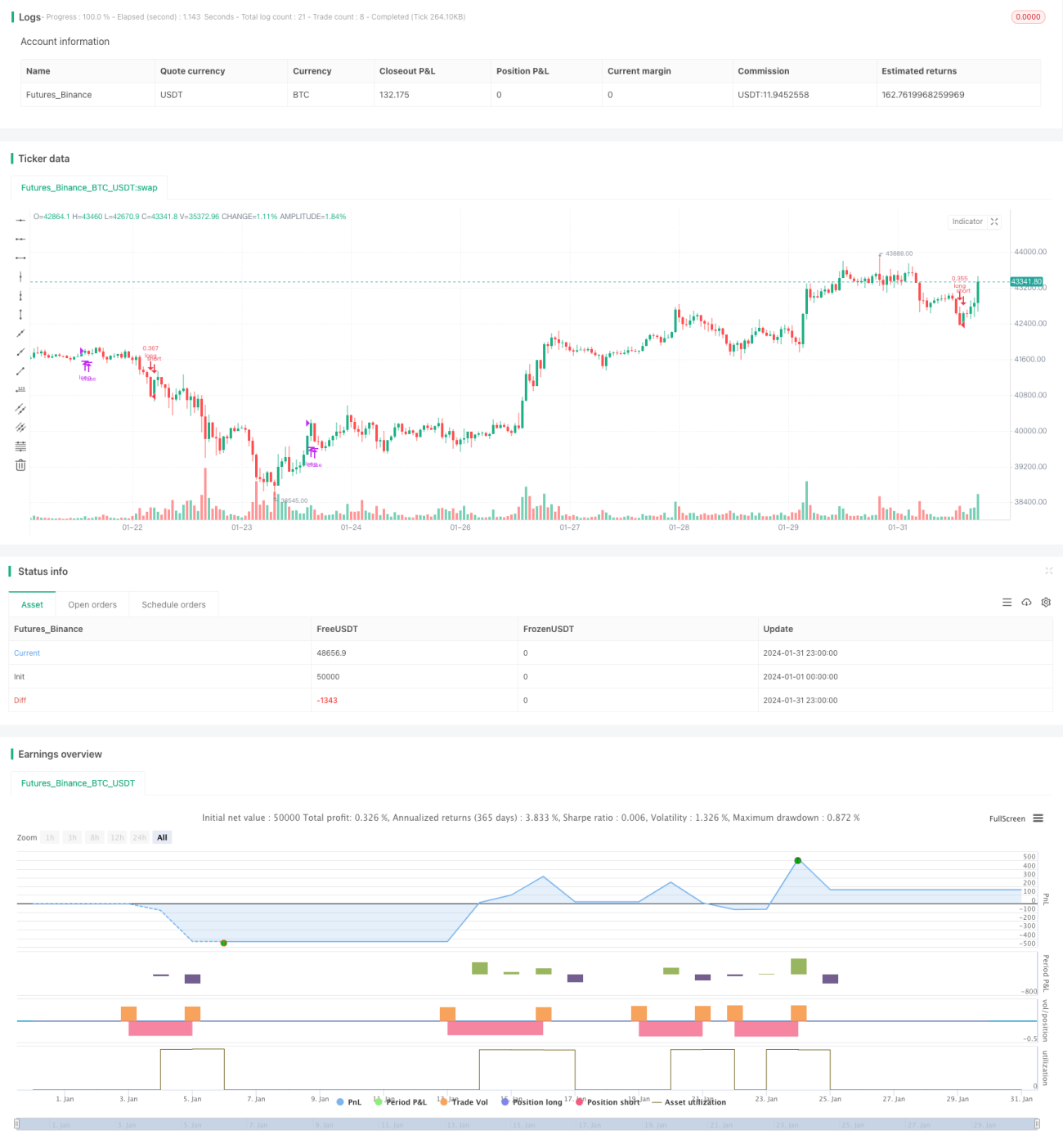

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © relevantLeader16058

//@version=4Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1