高出来高ブレイクアウトの複利ポジション戦略

1

Follow

1802

Followers

概要

本戦略の核となる考え方は、高取引量下でブレイクアウトを追跡し、リスク予算パーセンテージと250倍のシミュレーションレバレッジを設定することで複利ポジションを実現することです。高い売り圧力後の潜在的な反転機会を捉えることを目的としています。

戦略の原理

以下の条件がすべて満たされた場合、ロングエントリーします。

- 取引量がユーザー定義のしきい値(volThreshold)を超えている

- 現在のローソク足の最安値が前のローソク足の最安値より低い(lowLowerThanPrevBar)

- 現在のローソク足の終値がマイナスであり、かつ前のローソク足の終値より高い(negativeCloseWithHighVolume)

- 未決済のロングポジションが存在しない(strategy.position_size == 0)

ポジションサイズの計算方法は以下の通りです。

- 口座 equity に対するリスク割合(riskPercentage)に基づいてリスク金額を計算

- リスク金額にシミュレーションレバレッジ倍率(leverage、デフォルト250倍)を乗じて契約数を算出

エグジットルール:

ロングポジションの損益率 posProfitPct がストップロスライン(-0.14%)または利確ライン(4.55%)に達した時に決済します。

優位性分析

本戦略の優位性は以下の点にあります。

- 高取引量に伴うトレンド反転の機会を捉えられる

- 複利ポジション管理により、利益の伸びが速い

- ストップロスと利確の設定が合理的で、リスク管理に有効

リスク分析

本戦略には以下のようなリスクも存在します。

- 250倍のレバレッジにより損失が拡大する可能性

- スリッページ、手数料、証拠金などの実際の取引要素を考慮していない

- パラメータの最適化や実運用での検証を繰り返す必要がある

以下の方法でリスクを低減できます。

- レバレッジ倍率を適切に引き下げる

- ストップロスの幅を拡大する

- 実際の取引コストを考慮する

最適化の方向性

本戦略は以下の観点から最適化が可能です。

- レバレッジの動的調整

- ストップロス・利確条件の最適化

- トレンドフィルターの追加

- 銘柄の具体的特性に合わせたパラメータ調整

まとめ

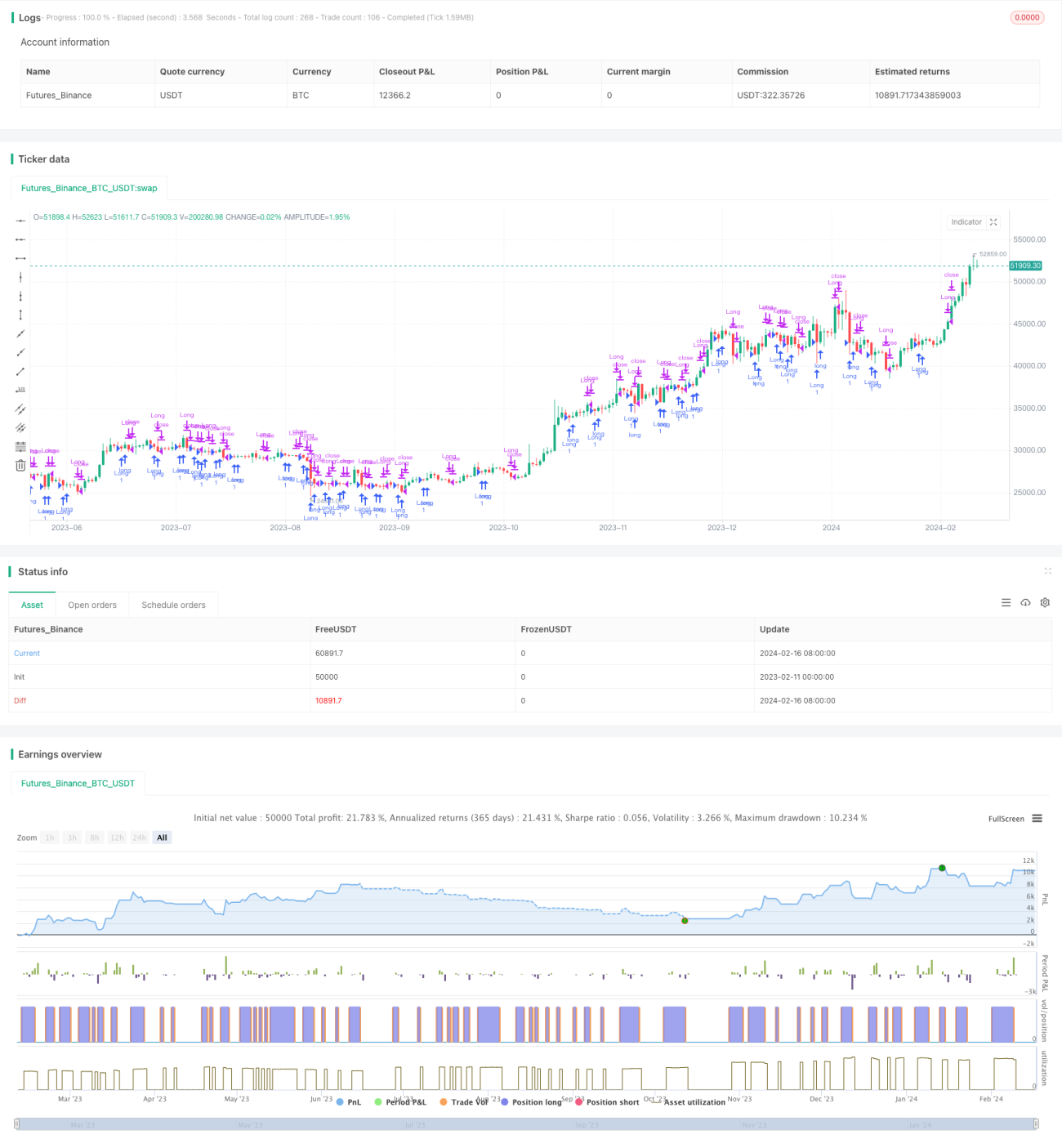

本戦略は全体的に比較的シンプルで直接的なアプローチであり、反転機会を捉えることで超過収益を狙います。ただし一定のリスクも存在するため、実運用での検証には注意が必要です。パラメータや戦略構造の最適化により、より安定性が高く実戦的なものに改善できます。

Source

Pine

/*backtest

start: 2023-02-11 00:00:00

end: 2024-02-17 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("High Volume Low Breakout (Compounded Position Size)", overlay=true, initial_capital=1000)

// Define input for volume thresholdStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1