ABCDパターンに基づき、ストップロストレーリングとテイクプロフィットトレーリングを備えた新しい量的取引戦略

一、戦略概要

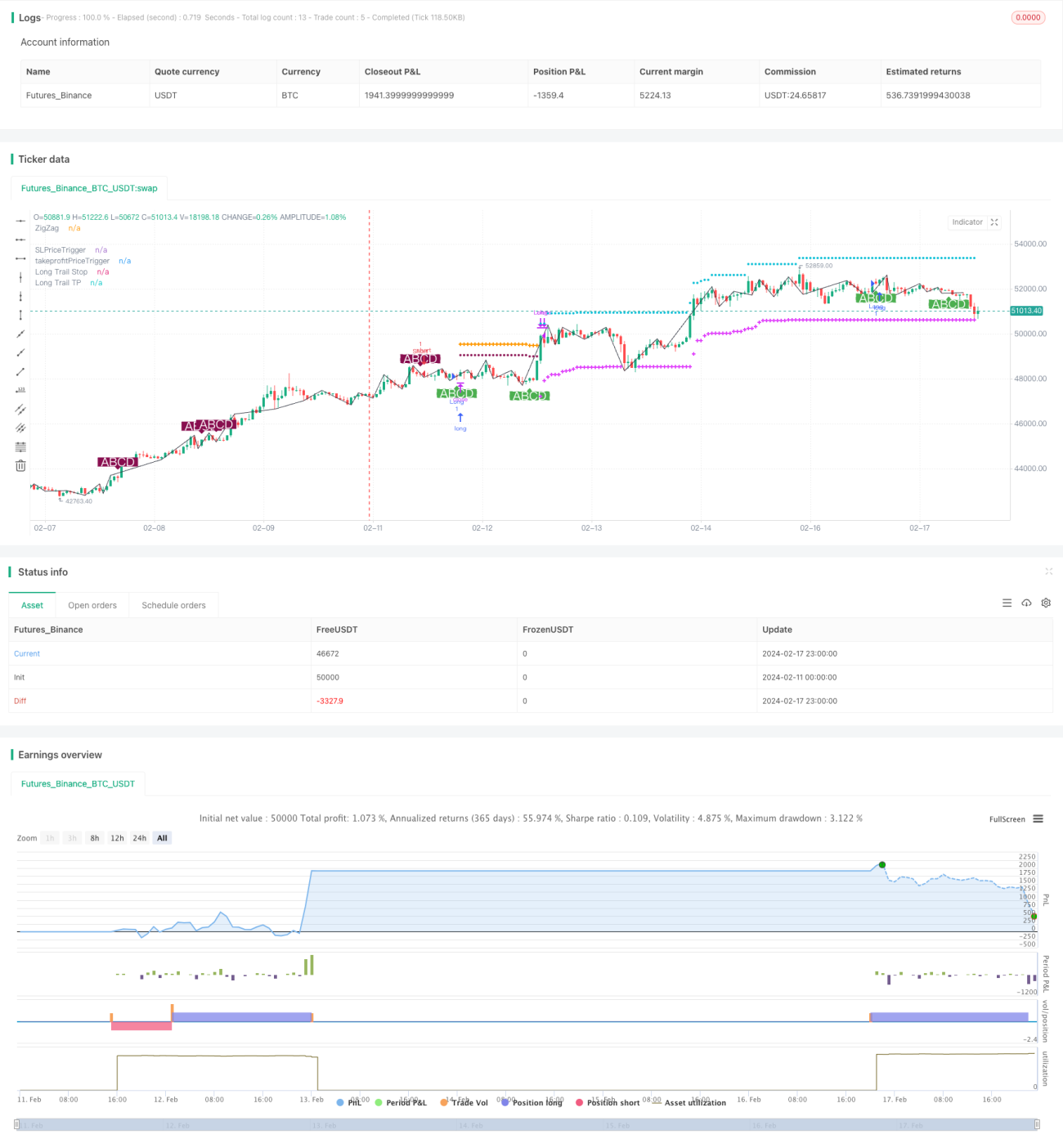

本戦略の名称は「最適ABCDパターン取引戦略(ストップロストレーリングおよびテイクプロフィットトレーリング付き)」です。これは明確なABCD価格パターンモデルに基づいて取引を行う定量戦略です。主な考え方は、完全なABCDパターンを識別した後、パターンの方向に従って買いまたは売りを行い、ストップロスとテイクプロフィットのトレーリングを設定してポジションを管理することです。

二、戦略原理

-

ボリンジャーバンドを補助的に使用して価格の天底(トップとボトム)の分岐点を識別し、価格のジグザグ曲線を取得します。

-

ジグザグ曲線上で完全なABCDパターンモデルを識別します。点A、B、C、Dは一定の比率関係を満たす必要があります。条件を満たすABCDパターンが識別されたら、買いまたは売りを行います。

-

買いまたは売りを行った後、ストップロストレーリングを設定してリスクを管理します。ストップロスは最初は固定ストップロスを使用し、利益が一定の割合に達した後にトレーリングストップロスに切り替えて利益の一部を確保します。

-

同様に、テイクプロフィットラインにもトレーリングを設定し、十分な利益を得た後に適時に利確して利益の吐き出しを防ぎます。テイクプロフィットトレーリングも2段階に分かれており、最初は固定テイクプロフィットで一部の利益を獲得し、その後トレーリングテイクプロフィットに切り替えて価格を追跡し続けます。

-

価格がトレーリングストップロスまたはテイクプロフィットに達した場合、ポジションを決済し、1回の取引サイクルを完了します。

三、戦略の優位性分析

-

ボリンジャーバンドを補助的に使用してジグザグ曲線を識別することで、従来のジグザグ曲線のバックテスト問題を回避し、取引シグナルの信頼性を高めます。

-

ABCDパターン取引モデルは成熟して安定しており、取引機会が比較的豊富です。また、ABCDパターンの方向性が明確であり、エントリー方向の判断が容易です。

-

2段階のストップロストレーリングとテイクプロフィットトレーリングを設定することで、リスク管理と利益獲得をより適切に行えます。トレーリングストップロス/テイクプロフィットにより、戦略の柔軟性が向上します。

-

戦略のパラメータ設計は合理的で、ストップロス/テイクプロフィットのパーセンテージやトレーリング開始パーセンテージをカスタマイズでき、柔軟に使用できます。

-

本戦略は、FX、暗号通貨、株価指数などのあらゆる銘柄に適用可能です。

四、戦略のリスク分析

-

ABCDパターンは比較的明確ですが、取引機会は限られており、十分な取引頻度を保証できません。

-

レンジ相場では、ストップロスやテイクプロフィットが頻繁にトリガーされる可能性があります。その場合、パラメータを適宜調整し、ストップロス/テイクプロフィットの範囲を拡大する必要があります。

-

取引銘柄の流動性に注意する必要があります。流動性が低い銘柄では、ストップロスやテイクプロフィットが正確に実行されにくくなります。

-

戦略は取引コストに敏感であるため、手数料が低いブローカーや口座を選択する必要があります。

-

一部のパラメータはさらに最適化できます。例えば、トレーリングストップロスとテイクプロフィットの開始条件について、より多くの値をテストして最適なポイントを見つけることができます。

五、戦略の最適化方向

-

他のインジケーターと組み合わせて、より多くのフィルター条件を設定し、一部のHWパターンを回避できます。これにより、無駄な取引の発生を減らせます。

-

市場の三区分構造(三段階)の判断を追加し、第三段階の相場でのみ取引機会を探します。これにより、戦略の勝率を向上させることができます。

-

初期資金規模をテストして最適化し、最適な初期資金水準を見つけます。大きすぎても小さすぎても最適なリターン率を得るのに不利です。

-

サンプル外データをテストして、パラメータのロバスト性を検証できます。これは戦略の中長期的な安定性を理解するために非常に重要です。

-

トレーリングストップロス/テイクプロフィットの開始条件とスリッページの大きさを引き続き最適化し、戦略の実行効率を向上させます。設定の最適化に終わりはありません。

六、戦略まとめ

本戦略は主にABCD価格パターンに依存して判断およびエントリーを行います。2段階のストップロストレーリングとテイクプロフィットトレーリングを設定してリスクとリターンを管理します。戦略は比較的成熟して安定していますが、取引頻度は低くなる可能性があります。フィルター条件を追加することで、より効率的な取引機会を得ることができます。さらに、パラメータと資金規模の最適化を続けることで、戦略の安定した収益性をさらに向上させることができます。全体的に、本戦略は考え方が明確で、理解・実装が容易であり、深く研究・応用する価値のある定量取引戦略です。

- 1