移動平均線クロス反転戦略

1

Follow

1802

Followers

概要

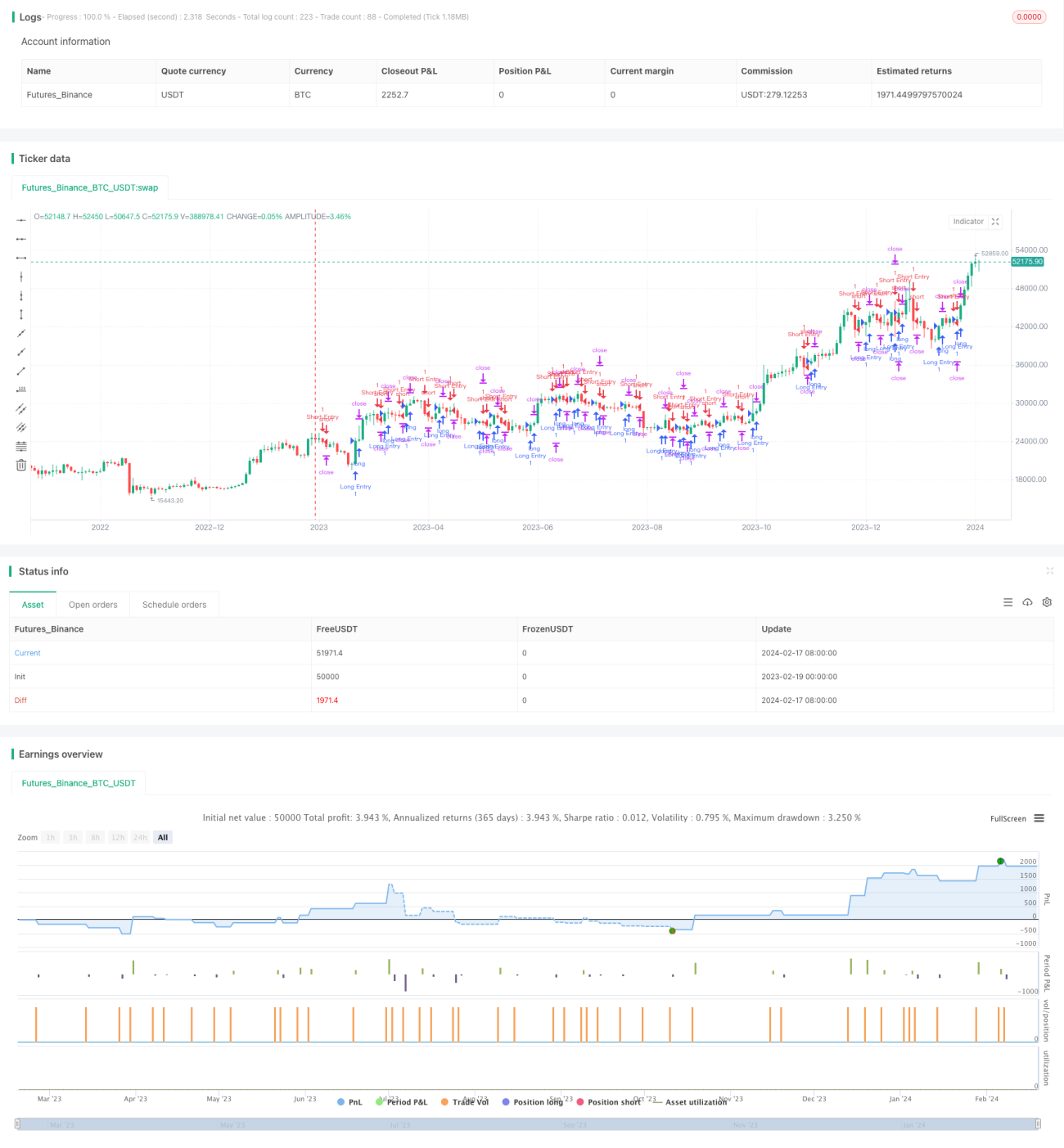

本戦略は、単純移動平均線に基づくクロスラインリバーサル戦略です。期間1と期間5の単純移動平均線を使用し、短期移動平均線が長期移動平均線を下から上にクロスしたときに買い、上から下にクロスしたときに売りを行う、典型的なトレンドフォロー戦略です。

戦略原理

本戦略では、クローズ価格の1日単純移動平均線sma1と5日単純移動平均線sma5を計算し、sma1がsma5を上抜けたときに買いエントリー、sma1がsma5を下抜けたときに売りエントリーします。買いの後は、ストップロスをエントリー価格の5ドル下に、利確をエントリー価格の150ドル上に設定します。売りの後は、ストップロスをエントリー価格の5ドル上に、利確をエントリー価格の150ドル下に設定します。

優位性分析

- 二本の移動平均線を使用して市場トレンド方向を判断し、ストップロス後にすぐに逆方向のエントリーを避ける

- 移動平均線のパラメータはシンプルで合理的、バックテスト結果は良好

- ストップロスの幅が小さく、一定の相場変動に耐えられる

- 利確の幅が大きく、十分な利益を得られる

リスク分析

- 二本の移動平均線戦略は騙されやすく、相場がレンジのときにストップロスの確率が高い

- トレンド相場を効果的に追跡できず、長期の利益能力が限られる

- パラメータ最適化の余地が限られ、オーバーフィットしやすい

- 特定の取引銘柄に依存し、異なる銘柄ではパラメータ調整が必要

最適化の方向性

- 他の指標によるフィルターを追加し、誤ったシグナルを避ける

- ストップロスと利確の幅を動的に調整する

- 移動平均線のパラメータを最適化する

- ボラティリティ指標と組み合わせて、ポジションサイズを管理する

まとめ

本戦略はシンプルな二本移動平均線戦略として、操作が簡単で実装しやすい特徴を持ち、戦略アイデアを迅速に検証できます。しかし、その耐性と利益空間は限られており、パラメータとフィルター条件を最適化して、より多くの市場環境に適応させる必要があります。初心者向けの最初の定量戦略として、基本的な要素を含んでおり、シンプルなフレームワークとして反復的な改善が可能です。

Source

Pine

Related strategies

Comment

All comments (0)

No data

- 1