モメンタムと標準偏差に基づくゴールド取引戦略

1

Follow

1802

Followers

概要

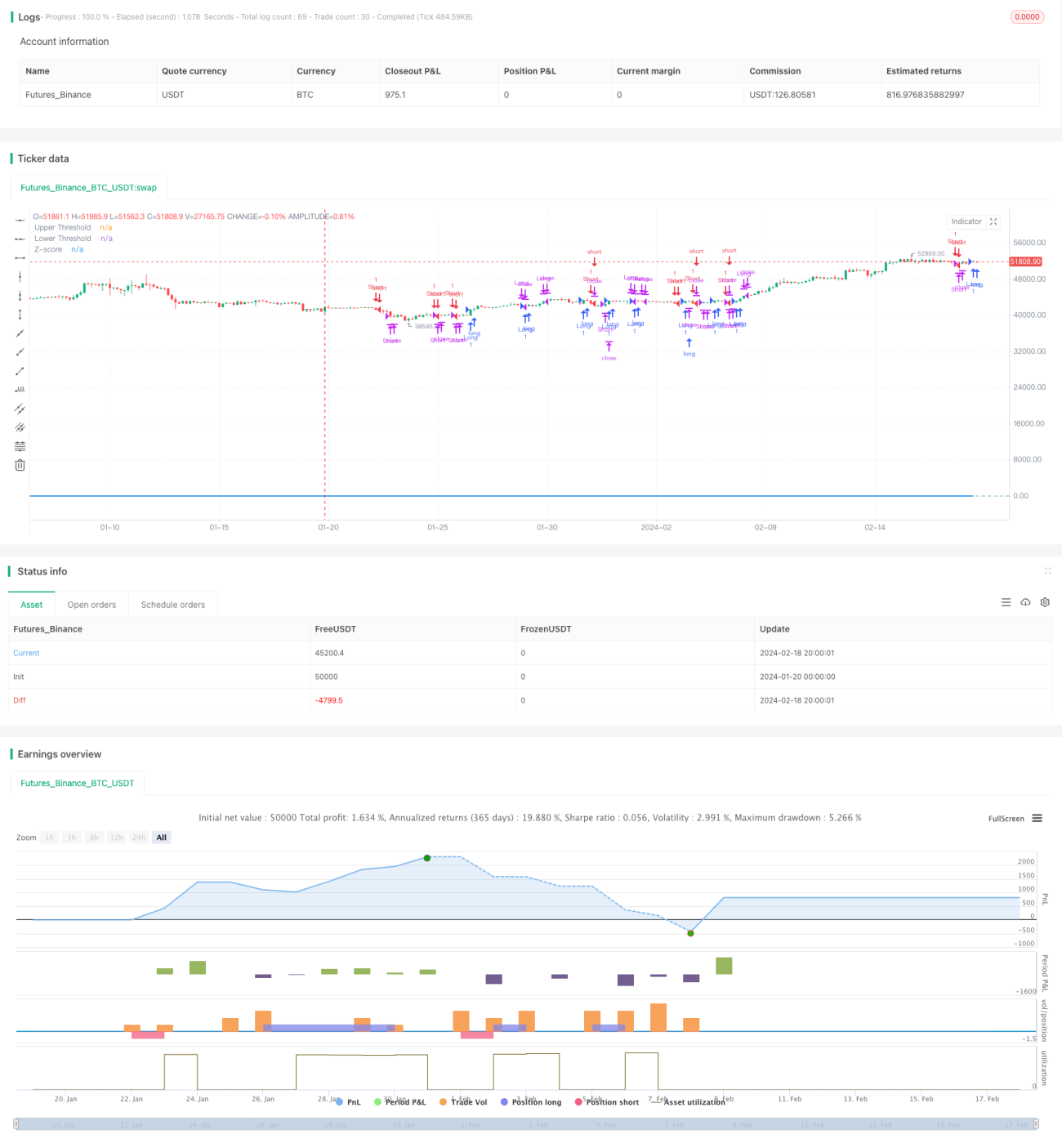

本戦略は、ゴールド価格の21日指数移動平均線からの乖離度を計算し、標準偏差を用いて市場の買われ過ぎ・売られ過ぎを判断します。乖離度が一定の標準偏差に達した時点でトレンドフォロー戦略を採用し、同時にストップロスメカニズムを設定してリスクを管理します。

戦略の原理

- 21日指数移動平均線を中心軸として計算

- ゴールド価格と移動平均線の乖離度を計算

- 乖離度を標準化し、Zスコアに変換

- Zスコアが0.5を上抜けた場合に買い、Zスコアが-0.5を下抜けた場合に売り

- Zスコアが閾値0.5/-0.5まで戻った場合にポジションをクローズ

- Zスコアが3/-3を超えた場合にストップロス

優位性分析

これは価格モメンタムと標準偏差を用いて市場の買われ過ぎ・売られ過ぎを判断するトレンドフォロー戦略であり、以下のような優位性があります。

- 移動平均線をダイナミックなサポート/レジスタンスとして使用することで、トレンドを捉えられる

- 標準偏差とZスコアが買われ過ぎ・売られ過ぎを的確に判断し、偽シグナルを低減

- 指数移動平均線を採用しているため、直近の価格の影響が大きく、より敏感に反応

- Zスコアによって価格の乖離度が標準化され、判断ルールが統一・明確になる

- ストップロスメカニズムを設定することで、早期に損切りを行いリスクを管理できる

リスク分析

本戦略には以下のようなリスクも存在します。

- 移動平均線を判断基準とするため、価格に明確なギャップやブレイクアウトが発生した場合、誤ったシグナルが生じる可能性がある

- 標準偏差とZスコアの判断閾値は適切に設定する必要があり、大きすぎても小さすぎても戦略パフォーマンスに影響を与える

- ストップロスの設定が不適切だと、過度にアグレッシブになり不要な損失を招く恐れがある

- 突発的な事象により価格が大きく変動した場合、ストップロスが発動しトレンドの機会を逃す可能性がある

解決方法:

- 移動平均線のパラメータを適切に設定し、主要トレンドを識別する

- バックテストにより標準偏差パラメータを最適化し、最適な閾値を探す

- トレーリングストップを設定し、ストップロスの妥当性を検証する

- 事象発生後、速やかに市場状況を再評価し、戦略パラメータを調整する

最適化の方向性

本戦略は以下の点から最適化が可能です。

- 単純な標準偏差の代わりにATRなどのボラティリティ指標を用いて、リスク選好をより適切に判断する

- 異なるタイプの移動平均線を試し、より適切な中心軸指標を見つける

- 移動平均線のパラメータを最適化し、最適な期間を特定する

- Zスコアの閾値を最適化し、最良の戦略パフォーマンスパラメータポイントを探す

- ボラティリティに基づくストップロス方法を追加し、よりスマートで合理的な損切りを実現する

まとめ

本戦略は全体的に基本的かつ合理的なトレンドフォロー戦略です。移動平均線を用いて主要トレンドの方向を判断し、価格乖離度を標準化することで市場の買われ過ぎ・売られ過ぎを明確に捉え、取引シグナルを生成します。適切なストップロス方法を設定することで、収益を確保しつつリスクを管理しています。さらにパラメータを最適化し、追加の条件判断を増やすことで、より安定・信頼性の高い戦略となり、高い応用価値を持ちます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1