定量取引プラットフォームに基づく適応的グリッド取引戦略

概要

本戦略は、定量取引プラットフォームに基づく適応型グリッド取引戦略です。この戦略では、自動または手動でグリッド取引範囲を設定し、その範囲内に等間隔で売買注文を配置することでグリッド取引を実行します。価格がグリッドの上限または下限を突破した場合、戦略は自動的にグリッドの範囲を調整します。

戦略の原理

-

グリッドの上限価格と下限価格を設定します。過去の価格の最高値と最安値を一定期間内で自動計算して上限・下限とするか、固定の上限・下限価格を手動で設定できます。

-

上限価格と下限価格、およびグリッド数に基づいて、各グリッドの価格間隔を計算します。

-

上限価格と下限価格の間で、等間隔に複数の売買ポイントをグリッドとして配置します。

-

市場価格がグリッド下限を突破した場合、最新の未決済注文があるグリッドの次のグリッドに買い注文を配置します。市場価格がグリッド上限を突破した場合、最新の未決済注文があるグリッドの前のグリッドに売り注文を配置します。

-

これにより、グリッドの上限と下限の間で継続的に売買操作を行います。価格トレンドが反転すると、以前の注文は徐々に利益確定または損切りされます。

戦略の利点

-

グリッド取引は、横ばいやレンジ相場で利益を上げることができます。

-

グリッド範囲を適応的に調整するため、市場の変動に応じて自動調整され、手動介入が不要です。

-

投資資金を事前に設定し、各グリッドに比例配分することで、1注文あたりのリスクを制御できます。

-

ロジックがシンプルで理解しやすく、パラメータ調整も柔軟です。

リスクと対策

-

上限・下限突破による損失

- 解決策: ストップロス位置を適切に設定する。

-

トレンド相場での連続損失

- 解決策: トレンドを識別し、取引を一時停止する。

-

パラメータ設定の不適切

- 解決策: グリッド数や価格間隔パラメータを調整する。

最適化の方向性

-

機械学習を活用して価格変動範囲やトレンドを予測し、グリッドパラメータを動的に調整する。

-

トレンド相場ではトレンド取引に切り替え、グリッド取引による損失を回避する。

-

資金使用率や収益率などの指標を組み合わせてリスク管理を行う。

-

複数の銘柄に拡大し、資金運用の幅を広げる。

まとめ

本戦略は、自動調整可能なパラメータ適応型グリッド戦略であり、レンジ相場の株式、暗号通貨、外国為替に適しています。パラメータ調整により、市場のさまざまな相場に適応でき、実戦価値があります。

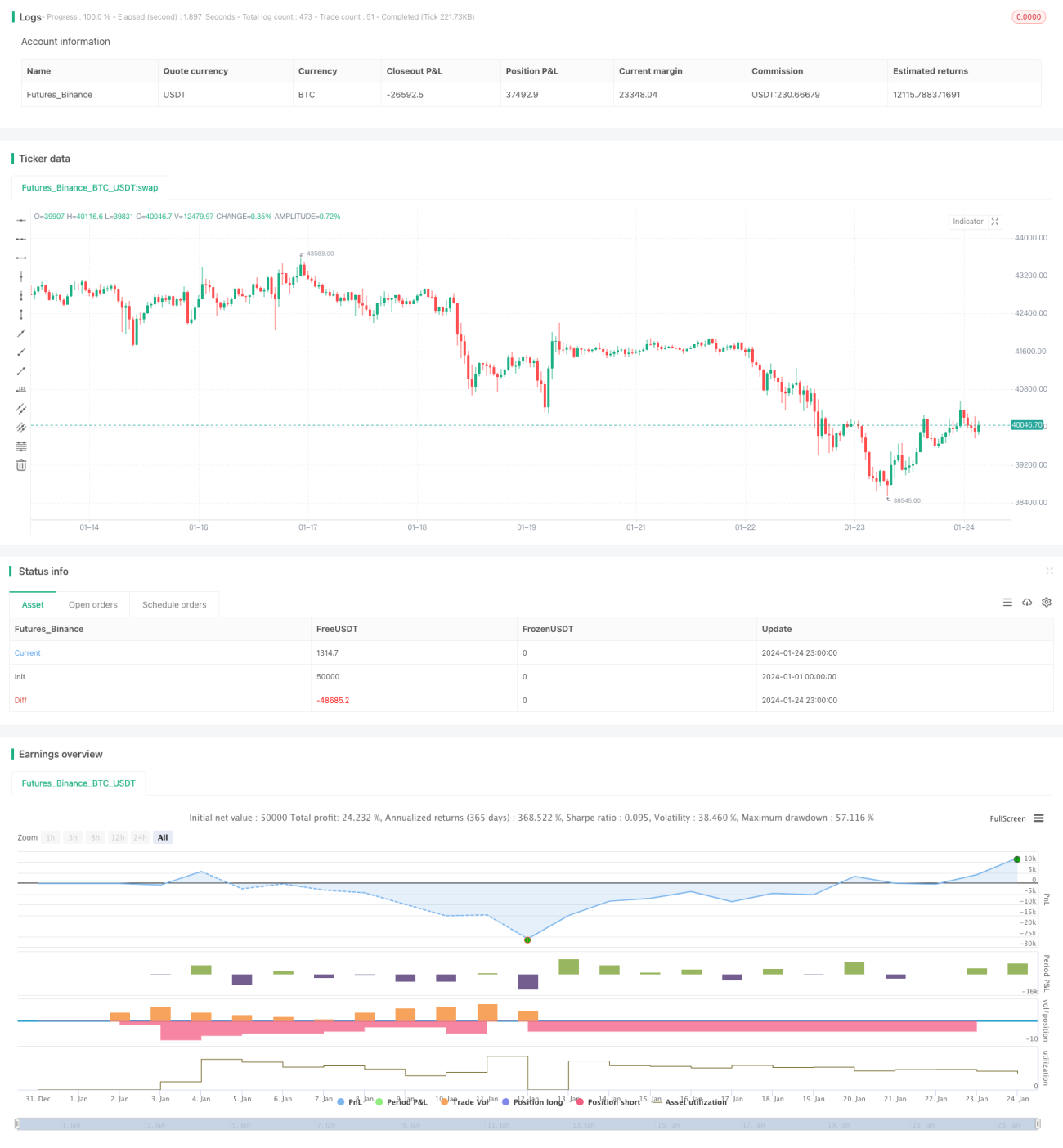

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-24 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//hk4jerry

strategy("Grid Bot Backtesting", overlay=false, pyramiding=3000, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.025)- 1