추세 필터링 이동 평균선 교차 퀀트 전략

개요

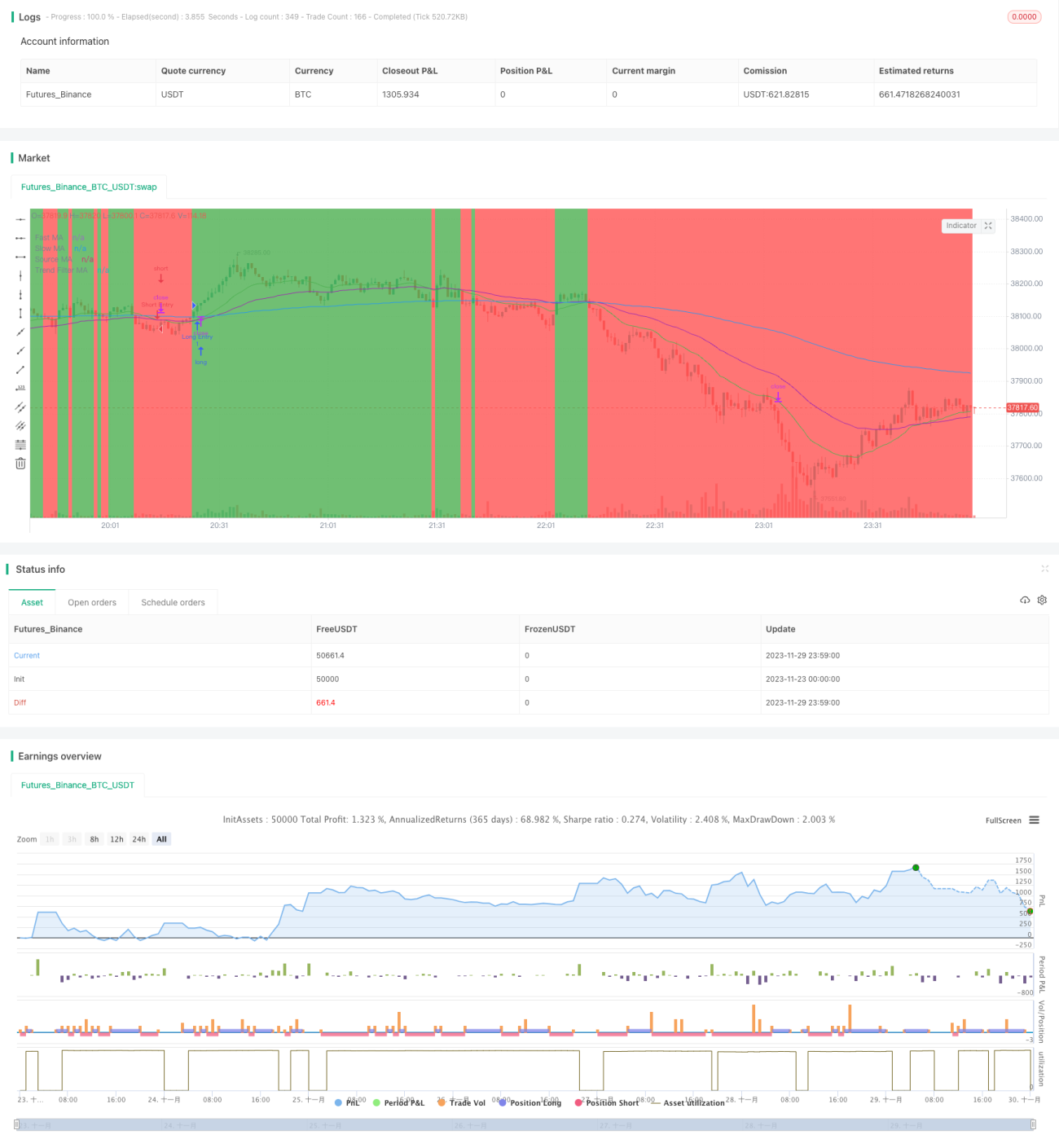

추세 필터 이동평균선 교차 퀀트 전략은 중장기 퀀트 트레이딩 전략입니다. 이 전략은 단기 이동평균선과 장기 이동평균선의 교차를 통해 시장의 추세 방향을 판단하고, 유효한 추세가 확인된 상태에서 진입합니다. 동시에, 더 긴 주기의 이동평균선을 추세 필터로 설정하여, 가격이 해당 이동평균선을 돌파할 때만 유효한 트레이딩 신호가 생성되도록 합니다.

전략 원리

이 전략은 기본적으로 이동평균선의 교차 원리에 기반합니다. 구체적으로, 서로 다른 두 주기의 이동평균선(일반적으로 20일선과 50일선)을 계산합니다. 20일선이 아래에서 위로 50일선을 돌파하면 매수 신호가 발생하고, 20일선이 위에서 아래로 50일선을 돌파하면 매도 신호가 발생합니다. 이러한 단순한 교차 신호는 중장기 돌파를 포착할 수 있다고 간주됩니다.

또한, 이 전략은 200일 이동평균선을 전체 추세 판단 지표로 설정합니다. 가격이 200일선을 돌파할 때만 위의 단순 교차 신호가 유효한 것으로 간주됩니다. 이는 횡보장에서 많은 무효 신호가 발생하는 것을 방지하는 추세 필터 메커니즘을 구성합니다.

전략 장점 분석

- 중장기 운용으로 과도한 거래를 피하고 거래 비용 및 슬리피지 리스크를 줄입니다.

- 이동평균선 교차 판단이 명확하여 이해하고 구현하기 쉽습니다.

- 추세 필터 메커니즘은 대부분의 무효 신호를 걸러내어 승률을 높입니다.

- 이동평균선 파라미터를 유연하게 조정할 수 있어 다양한 종목과 시간 주기에 적용 가능합니다.

- 손절 및 이익실현을 설정하여 개별 거래의 손익을 통제할 수 있습니다.

전략 리스크 분석

- 가격이 이동평균선 부근에서 변동할 때 여러 번의 무효 신호가 발생하여 과도한 거래로 이어질 수 있습니다.

- 장기 이동평균선은 시장에 뒤처져 추세 전환점을 놓칠 수 있습니다.

- 이동평균선 지표 구축에 충분한 과거 데이터가 필요하므로, 신규 종목이나 단기 주기에는 적용이 어렵습니다.

- 전략 파라미터는 반복적인 테스트와 최적화가 필요하며, 부적절한 설정은 전략 실패로 이어질 수 있습니다.

리스크에 대한 대응 방안:

- 더 긴 주기의 이동평균선을 사용하거나 추세 필터 조건을 추가합니다.

- 에너지 지표, 변동성 지표 등 다른 지표를 결합하여 큰 추세를 판단합니다.

- 이동평균선 주기 파라미터의 적응성을 향상시킵니다.

- 파라미터 최적화 및 피드백 메커니즘을 추가하여 전략 파라미터를 동적으로 조정합니다.

전략 최적화 방향

- 선형 가중 이동평균선 등 다양한 유형의 이동평균선을 시도합니다.

- 적응형 이동평균선 주기 기능을 추가합니다.

- 변동성 관련 지표를 결합하여 추세 구간을 판단하고 이동평균선 교차의 유효성을 높입니다.

- 머신러닝 알고리즘을 추가하여 전략 파라미터의 자동 최적화를 구현합니다.

- 다중 종목 조합 전략을 탐구하여 종목 간 상관관계를 활용한 수익 창출을 모색합니다.

결론

추세 필터 이동평균선 교차 전략은 전반적으로 간단하고 실용적인 중장기 퀀트 전략입니다. 이동평균선 교차를 통해 중장기 추세를 판단하고 추세 필터를 결합하여 무효 신호를 줄입니다. 이 전략은 이해하고 구현하기 쉬워 퀀트 트레이딩 초보자에게 적합합니다. 개선 가능성은 이동평균선 최적화와 다른 지표 및 머신러닝 알고리즘과의 통합에 있습니다. 기본 전략으로서 더 고급 퀀트 트레이딩 차익거래 알고리즘에 트레이딩 신호를 제공할 수 있습니다.

- 1