양방향 이동평균 회귀 거래 전략

개요

쌍방향 이동평균 회귀 트레이딩 전략(Bidirectional Moving Average Reversion Trading Strategy)은 가격 평균 회귀 원리를 활용하여 구축된 퀀트 트레이딩 전략입니다. 이 전략은 여러 개의 이동평균선을 설정하여 가격 반전 기회를 포착하며, 가격이 이동평균선에서 일정 폭 이상 이탈하면 진입하고, 가격이 이동평균선으로 회귀할 때 청산하여 차익을 얻습니다.

전략 원리

이 전략은 주로 가격 평균 회귀 이론에 기반합니다. 가격은 항상 평균값을 중심으로 변동하며, 평균값에서 심각하게 이탈할수록 평균으로 회귀할 가능성이 높아진다는 원리를 이용합니다. 구체적으로, 이 전략은 세 그룹의 이동평균선을 동시에 설정합니다: 진입 이동평균선, 청산 이동평균선, 한계 이동평균선입니다. 가격이 진입 이동평균선에 도달하면 해당하는 매수 또는 매도 포지션이 열립니다. 가격이 청산 이동평균선에 도달하면 이전 포지션을 청산합니다. 마지막으로, 가격이 계속 움직여 회귀하지 않을 경우 한계 이동평균선이 손실을 통제합니다.

코드 로직상 진입 이동평균선은 매수선과 매도선으로 나뉘며, 각각 장기선과 단기선으로 구성됩니다. 이 선들과 가격 간의 이탈 정도가 포지션 크기를 결정합니다. 또한, 청산 이동평균선은 별도의 이동평균선으로 청산 시점을 결정합니다. 가격이 이 이동평균선까지 도달하면 포지션이 청산됩니다.

장점 분석

쌍방향 이동평균 회귀 전략의 장점은 주로 다음과 같습니다:

- 가격 반전 포착, 추세 횡보 시장에 적합

- 한계 손실을 통한 위험 통제

- 사용자 정의 가능한 파라미터 조합, 적응성 높음

- 이해하기 쉽고 파라미터 최적화 용이

이 전략은 변동성이 낮고 가격 변동 범위가 작은 종목, 특히 횡보 국면에 진입한 종목에 적합합니다. 가격의 일시적 반전 기회를 효과적으로 포착합니다. 또한 위험 통제 조치가 비교적 완비되어 있어 가격이 회귀하지 않더라도 손실을 일정 범위 내로 통제할 수 있습니다.

위험 분석

쌍방향 이동평균 회귀 전략에는 몇 가지 위험도 존재합니다:

- 추세 추종 위험. 가격이 급격한 추세를 보일 때 이 전략은 연속적으로 포지션을 열어 결국 폭락(청산)할 수 있습니다.

- 가격 변동폭 과다 위험. 가격 변동폭이 너무 클 경우 포지션이 한계 손실에 도달하여 강제 청산될 수 있습니다.

- 파라미터 최적화 위험. 이 전략의 파라미터 설정은 수익성에 큰 영향을 미치며, 파라미터 설정이 부적절할 경우 수익 확률이 크게 낮아집니다.

위의 위험에 대해 다음과 같은 측면에서 최적화할 수 있습니다:

- 진입 제한 강화, 지나치게 빈번한 진입 방지

- 포지션 규모 적절히 축소, 폭락 위험 방지

- 이동평균선 주기, 청산선 파라미터 등 설정 최적화

최적화 방향

이 전략은 최적화 여지가 크며, 주로 다음과 같은 각도에서 진행할 수 있습니다:

- 진입 조건 로직 추가, 추세 시장에서의 추세 추종 방지

- 포지션 축소 로직 추가, 가격 급변동으로 인한 위험 방지

- 다양한 유형의 이동평균선 지표 시도, 더 나은 파라미터 조합 탐색

- 머신러닝 방법을 이용한 자동 파라미터 최적화

- 자동 손절매 전략 추가, 위험 통제 강화

요약

쌍방향 이동평균 회귀 트레이딩 전략은 이동평균선에서 이탈한 가격이 회귀하는 기회를 포착하여 수익을 냅니다. 위험을 효과적으로 통제하며, 파라미터 최적화를 통해 더 나은 수익을 얻을 수 있습니다. 이 전략에도 몇 가지 위험이 존재하지만, 진입 로직 개선, 포지션 규모 축소 등의 방법으로 통제할 수 있습니다. 이 전략은 간단하고 이해하기 쉬우며, 퀀트 트레이더가 추가로 연구하고 최적화할 가치가 있습니다.

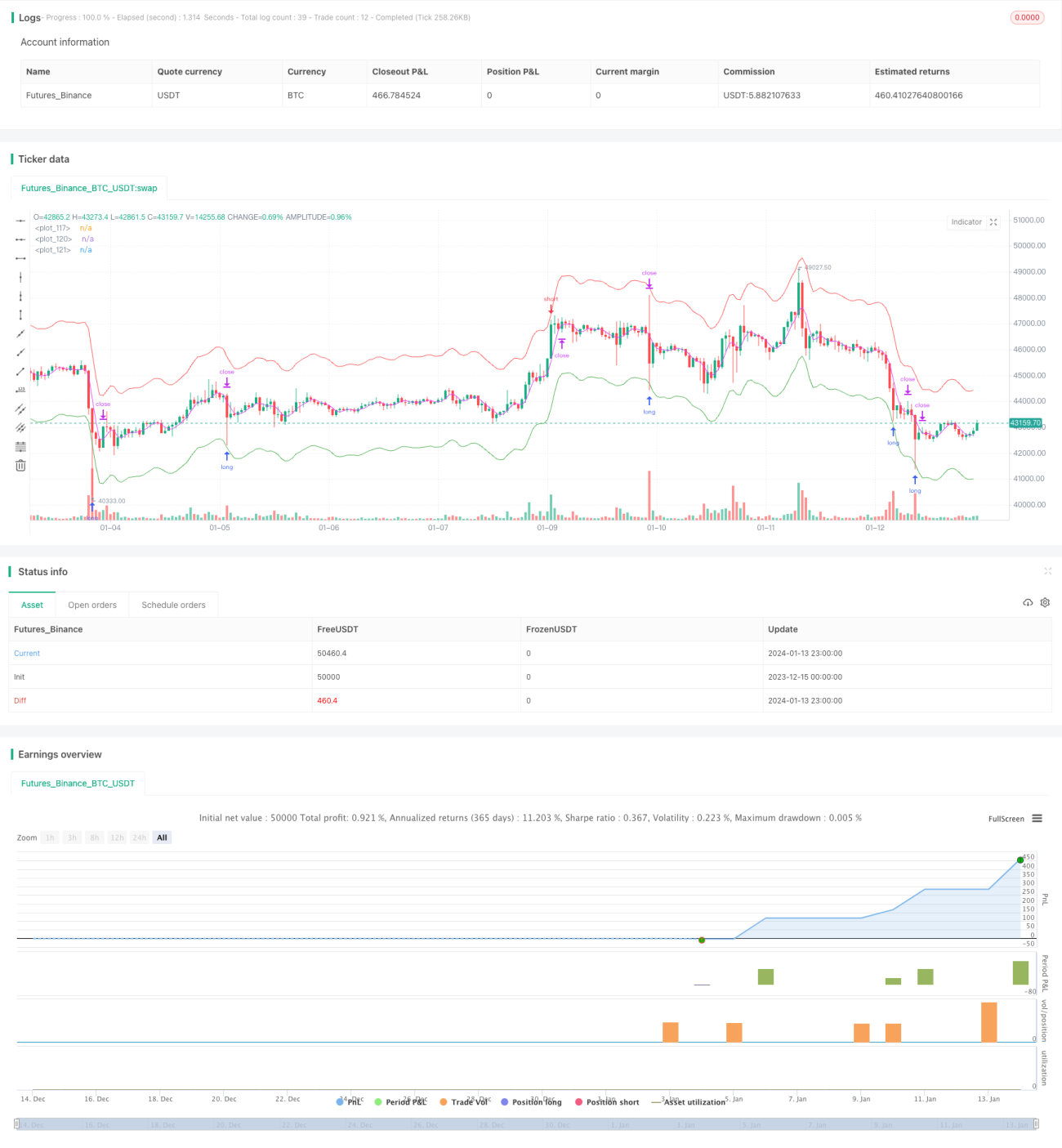

/*backtest

start: 2023-12-15 00:00:00

end: 2024-01-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title = "hamster-bot MRS 2", overlay = true, default_qty_type = strategy.percent_of_equity, initial_capital = 100, default_qty_value = 30, pyramiding = 1, commission_value = 0.1, backtest_fill_limits_assumption = 1)

info_options = "Options"

- 1