RSI와 이동평균선을 기반으로 한 다중 시간 프레임 거래 전략

개요

이 전략은 스토캐스틱 지표, RSI, 단순 이동 평균(SMA) 및 가중 이동 평균(WMA)을 결합하여 매수·매도 신호를 찾습니다. 동시에 5분 및 1시간 시간 프레임에서 추세 방향을 판단합니다. 안정화된 추세에서 빠른 RSI선이 느린 RSI선을 상향 또는 하향 돌파할 때 거래 신호가 발생합니다.

전략 원리

이 전략은 먼저 1시간과 5분 두 시간 프레임에서 각각 144주기 가중 이동 평균(WMA)과 5주기 단순 이동 평균(SMA)을 계산합니다. 5분 SMA가 WMA 위에 있을 때만 강세 시장으로 간주합니다. 그런 다음 전략은 RSI의 다중·공포 지표와 해당 K선 및 D선을 계산합니다. K선이 과매수 영역에서 D선을 하향 돌파하면 매도 신호가 발생하고, K선이 과매도 영역에서 D선을 상향 돌파하면 매수 신호가 발생합니다.

장점 분석

이것은 매우 효과적인 추세 추종 전략입니다. 두 가지 시간 프레임을 동시에 결합하여 추세를 판단하므로 잘못된 신호를 크게 줄입니다. 또한 RSI, SMA 및 WMA를 포함한 여러 지표를 필터링하여 신호를 더욱 신뢰할 수 있게 만듭니다. RSI가 KDJ를 구동하도록 함으로써 일반 KDJ 전략에서 발생하기 쉬운 가짜 신호 문제도 수정했습니다. 또한 이 전략에는 손절매와 이익 실현 설정이 포함되어 수익을 고정하고 위험을 효과적으로 통제할 수 있습니다.

위험 분석

이 전략의 가장 큰 위험은 추세 판단 오류입니다. 시장 전환점에서 단기 및 장기 이동 평균이 동시에 상승 또는 하락 반전하여 잘못된 신호를 생성할 수 있습니다. 또한 변동성 장세에서는 RSI가 많은 얽힌 거래 신호를 생성할 수도 있습니다. 그러나 이러한 위험은 SMA 및 WMA 주기와 RSI 매개변수를 적절히 조정하여 완화할 수 있습니다.

최적화 방향

이 전략은 다음과 같은 측면에서 최적화할 수 있습니다:

- 다양한 길이의 SMA, WMA 및 RSI를 테스트하여 최적의 매개변수 조합을 찾습니다.

- MACD, 볼린저 밴드 등 다른 지표를 추가하여 신호 신뢰성을 검증합니다.

- 손절매 및 이익 실현 전략을 최적화하고 고정 비율 손절, 잔액 슬리피지 손절, 트레일링 스탑 등 방법을 테스트합니다.

- 자금 관리 모듈을 추가하여 단일 거래 규모와 전체 위험 노출을 통제합니다.

- 머신러닝 알고리즘을 추가하여 대규모 백테스팅을 통해 최고 성과의 매개변수를 찾습니다.

요약

이 전략은 이동 평균과 스토캐스틱 지표의 장점을 최대한 활용하여 비교적 신뢰할 수 있는 추세 추종 시스템을 구축했습니다. 여러 시간 프레임과 지표의 검증을 통해 중장기 추세 방향을 원활하게 포착할 수 있습니다. 또한 손절매 및 이익 실현 설정으로 어느 정도의 시장 변동성을 견딜 수 있습니다. 그러나 더 많은 지표를 결합하여 사용하거나 머신러닝 방법을 도입하여 최적의 매개변수를 찾는 등 개선 여지가 남아 있습니다. 전반적으로 매우 유망한 거래 전략입니다.

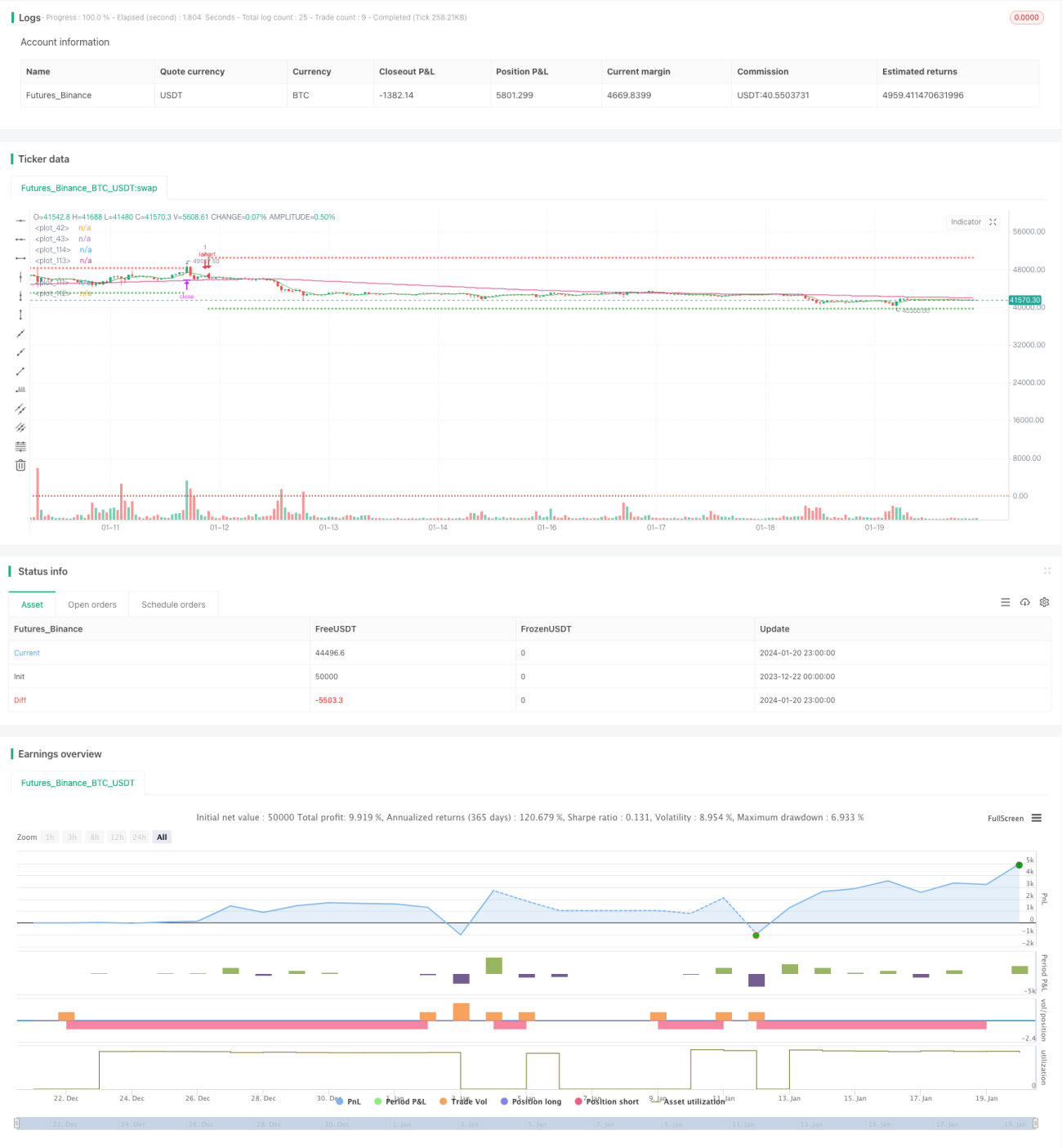

/*backtest

start: 2023-12-22 00:00:00

end: 2024-01-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © bufirolas

// Works well with a wide stop with 20 bars lookback- 1