모멘텀 되돌림 전략 기반

개요

이 전략은 시장에서 잠재적인 되돌림 기회를 식별하는 것을 목표로 합니다. 본 전략은 장기 이동평균선(MA1)과 단기 이동평균선(MA2)으로 구성된 이중 이동평균선 시스템을 사용합니다. 주요 목표는 종가가 MA1보다 낮지만 MA2보다 높을 때, 이는 큰 추세 내에서 잠재적인 되돌림 기회를 나타내므로 매수(long) 포지션을 취하는 것입니다.

전략 원리

이 전략은 두 개의 이동평균선(장기 MA1, 단기 MA2)을 사용합니다. 원리는 단기 가격이 하락하여 장기 추세의 지지선을 테스트한다면, 이는 매수 기회가 될 수 있다는 것입니다. 구체적으로, 종가가 장기 지지선(MA1) 위에 있으면 큰 추세가 여전히 양호함을 의미하고, 종가가 단기 이동평균선(MA2) 아래로 떨어졌지만 장기 이동평균선(MA1) 위에 안정적으로 머물러 있다면 이는 전형적인 되돌림 기회입니다. 이때 매수하고 손절매를 설정한 후, 가격이 다시 단기선 위로 올라오기를 기다립니다.

장점 분석

본 전략의 장점은 다음과 같습니다:

- 구현이 간단하고 이해하기 쉬우며 매개변수 조정이 유연함

- 이중 이동평균선 시스템을 활용하여 큰 추세를 식별하고 역추세 거래를 피함

- 맞춤형 시간 필터를 통해 특정 시간대의 시장 이상 현상을 방지

- 포지션 크기를 조정하여 다양한 위험 선호도에 대응 가능

- 손절매 메커니즘을 사용하여 손실 위험을 제한

리스크 분석

본 전략에는 다음과 같은 리스크도 존재합니다:

- 되돌림 실패로 가격이 계속 하락하여 손절매가 작동하지 않을 수 있음

- 큰 추세가 전환되어 기존 지지선이 깨질 수 있음

- 시장에 급격한 변동성이 발생하여 이동평균선이 이격될 수 있음

- 시간대 선택이 부적절하여 거래 기회를 놓칠 수 있음

이에 따라 다음과 같은 측면에서 최적화 및 개선이 가능합니다:

- 이동평균선 매개변수 최적화로 거래 신호 품질 개선

- 손절매 수준 최적화로 위험을 최소화하면서 수익 확보

- 시간 필터 조정으로 최적의 거래 시간대 설정

- 다양한 종목 및 시장 환경 테스트

최적화 방향

본 전략은 다음과 같은 측면에서 최적화할 수 있습니다:

- 이동평균선 매개변수 최적화로 최적의 조합 탐색

- 추적 손절매, 변동성 손절매 등 다양한 손절매 메커니즘 테스트

- 거래량 필터, 변동성 필터 등 추가 필터 도입

- 골든크로스 시 추가 매수, 데드크로스 시 축소 등 포지션 관리 메커니즘 추가

- 자동 이익 실현 메커니즘 추가

- 백테스트 및 주요 지표 계산을 통해 최적 매개변수 결정

요약

본 전략은 전반적으로 간단하고 실용적인 단기 되돌림 전략입니다. 이중 이동평균선을 사용하여 되돌림 기회를 식별하고 이동 손절매로 리스크를 관리합니다. 이해하고 구현하기 쉬우며 매개변수 조정이 유연하여 다양한 위험 선호도를 충족할 수 있습니다. 다음 단계로는 이동평균선 매개변수, 손절매 메커니즘, 필터 등 여러 측면에서 개선하여 전략을 더욱 견고하게 만들 수 있습니다.

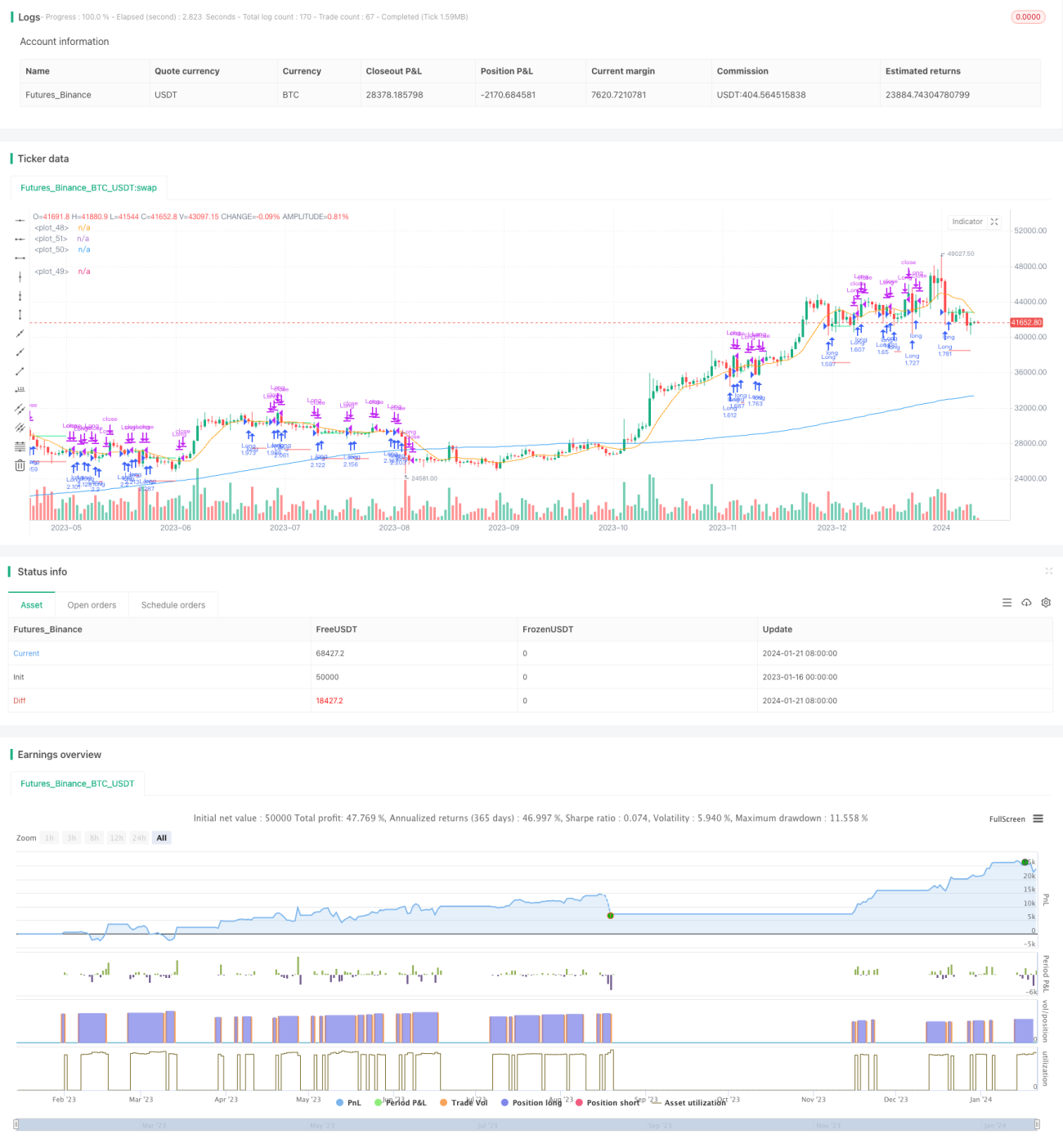

/*backtest

start: 2023-01-16 00:00:00

end: 2024-01-22 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © ZenAndTheArtOfTrading / www.PineScriptMastery.com

// @version=5

strategy("Simple Pullback Strategy", - 1