개요

불장 추적 시스템은 추세 추종 기반의 기계적 거래 시스템입니다. 4시간 차트의 추세 지표를 사용하여 거래 신호를 필터링하고, 진입은 15분 차트의 지표에 따라 판단합니다. 주요 지표는 RSI, 스토캐스틱, MACD입니다. 이 시스템의 장점은 여러 시간 프레임을 결합하여 가짜 신호를 효과적으로 걸러낼 수 있고, 더 낮은 시간 프레임의 지표를 사용하여 비교적 정확한 진입 타이밍을 잡을 수 있다는 점입니다. 그러나 이 시스템에는 과도한 거래와 가짜 돌파 문제가 발생하기 쉬운 위험도 존재합니다.

원리

이 시스템의 핵심 로직은 서로 다른 시간 프레임의 지표를 결합하여 추세 방향과 진입 타이밍을 식별하는 것입니다. 구체적으로 4시간 차트의 RSI, 스토캐스틱, EMA가 모두 조건을 충족해야 전반적인 추세 방향을 판단합니다. 이는 대부분의 노이즈를 효과적으로 걸러낼 수 있습니다. 동시에 15분 차트의 RSI, 스토캐스틱, MACD, EMA도 동일하게 상승 또는 하락 신호를 보여 구체적인 진입 타이밍을 결정합니다. 이를 통해 좋은 매수/매도 포인트를 찾을 수 있습니다. 4시간과 15분 판단이 모두 일치할 때만 이 시스템은 거래 신호를 발행합니다.

장점

- 여러 시간 프레임 조합으로 가짜 신호를 효과적으로 필터링하고 주요 추세를 식별 가능

- 15분 단위 세부 지표로 비교적 정확한 진입 타이밍 확보

- RSI, 스토캐스틱, MACD 등 주류 기술 지표를 조합하여 이해하기 쉽고 최적화도 용이

- mStop 이익실현, 손절, 트레일링 스탑 등 엄격한 리스크 관리 수단을 적용하여 단일 거래 리스크를 효과적으로 통제

리스크

- 과도한 거래 리스크: 시스템이 단기 시간 프레임에 민감하여 많은 거래 신호가 발생, 과도한 거래 유발 가능

- 가짜 돌파 리스크: 단기 지표 판단에 오류가 발생하여 가짜 돌파 신호 생성 가능

- 지표 무효화 리스크: 기술 지표 자체에 한계가 있어 극단적인 시장 상황에서 무용화 가능

이에 따라 다음과 같은 측면에서 시스템을 최적화할 수 있습니다:

- 지표 파라미터 조정으로 다양한 시장 환경에 적합

- 필터 조건 추가로 거래 빈도 감소 및 과도한 거래 방지

- 이익실현/손절 전략 최적화로 시장 변동 폭에 더 부합하도록 조정

- 다양한 지표 조합 테스트로 최적 해 찾기

요약

불장 추적 시스템은 전반적으로 매우 실용적인 추세 추종 기계적 거래 시스템입니다. 여러 시간 프레임의 지표 조합을 활용하여 시장 추세와 핵심 진입 타이밍을 식별합니다. 합리적인 파라미터 설정과 지속적인 최적화 테스트를 통해 이 시스템은 대부분의 시장 환경에 적응하여 안정적인 수익 효과를 낼 수 있습니다. 그러나 잠재적인 위험들을 인식하고 적극적인 조치로 예방 및 해소해야 합니다.

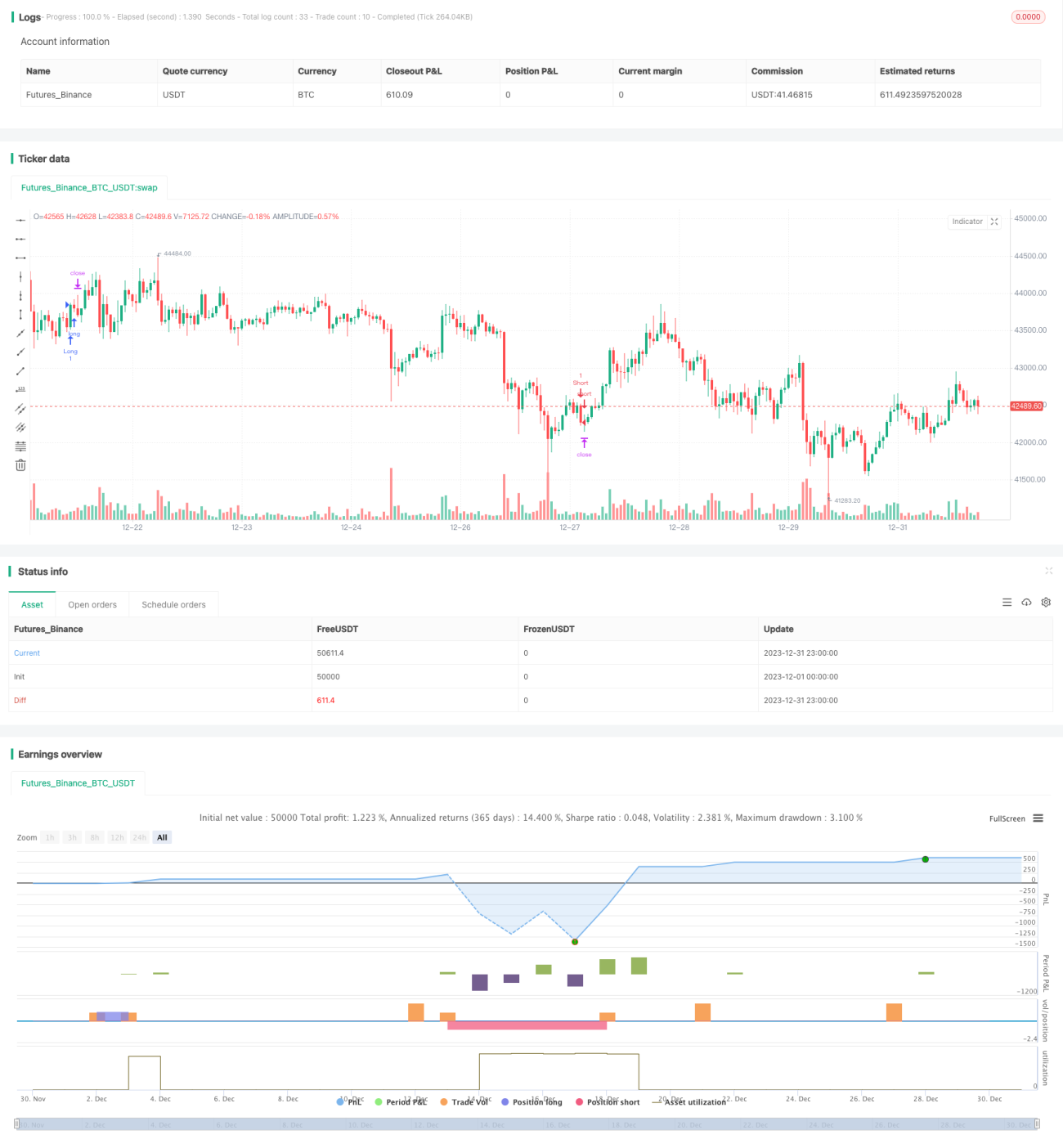

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Cowabunga System from babypips.com", overlay=true)

// 4 Hour Stochastics

length4 = input(162, minval=1, title="4h StochLength"), smoothK4 = input(48, minval=1, title="4h StochK"), smoothD4 = input(48, minval=1, title="4h StochD")- 1