고거래량 돌파 복리 포지션 전략

1

Follow

1802

Followers

개요

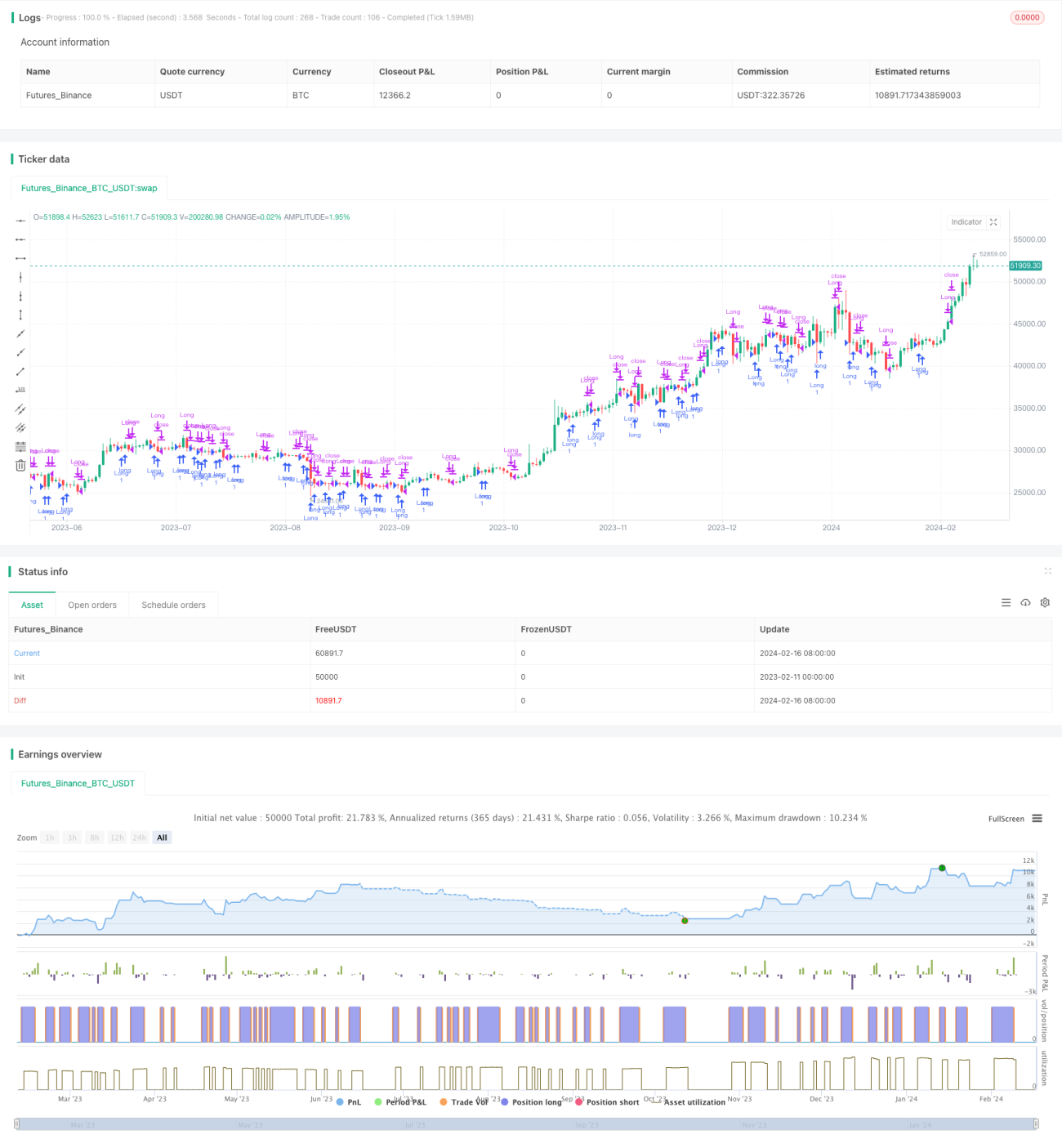

본 전략의 핵심 아이디어는 높은 거래량 상황에서 돌파를 추적하고, 위험 예산 비율과 250배의 시뮬레이션 레버리지를 설정하여 복리 포지션을 실현하는 것입니다. 높은 매도 압력 이후 잠재적인 반전 기회를 포착하는 것을 목표로 합니다.

전략 원리

다음 조건이 모두 충족될 때 매수 진입합니다:

- 거래량이 사용자 정의 임계값(volThreshold)을 초과

- 현재 캔들의 최저가가 이전 캔들의 최저가보다 낮음(lowLowerThanPrevBar)

- 현재 캔들의 종가가 음수이고 이전 캔들의 종가보다 높음(negativeCloseWithHighVolume)

- 미청산 매수 포지션이 없음(strategy.position_size == 0)

포지션 크기 계산 방법:

- 계정 자본(equity)의 위험 비율(riskPercentage)에 따라 위험 금액 계산

- 위험 금액에 시뮬레이션 레버리지 배수(leverage, 기본값 250배)를 곱하여 계약 수량 획득

청산 원칙:

매수 포지션 손익 비율 posProfitPct이 손절매 라인(-0.14%) 또는 이익실현 라인(4.55%)에 도달하면 포지션을 청산합니다.

장점 분석

본 전략의 장점은 다음과 같습니다:

- 높은 거래량으로 인한 추세 반전 기회 포착

- 복리 포지션 관리 채택으로 수익 성장이 빠름

- 손절매 및 이익실현 설정이 합리적, 위험 통제에 유리

위험 분석

해당 전략에는 다음과 같은 위험도 존재합니다:

- 250배 레버리지는 손실을 확대함

- 슬리피지, 수수료 및 증거금 등 실제 거래 요소를 고려하지 않음

- 반복적인 백테스트로 매개변수 최적화 및 실전 검증 필요

다음 방법으로 위험을 낮출 수 있습니다:

- 적절히 레버리지 배수 낮추기

- 손절매 폭 증가

- 실제 거래 비용 고려

최적화 방향

본 전략은 다음과 같은 측면에서 최적화할 수 있습니다:

- 동적으로 레버리지 크기 조정

- 손절매 및 이익실현 조건 최적화

- 추세 필터 추가

- 주식의 구체적 특성에 맞춰 매개변수 조정

요약

본 전략은 전반적으로 비교적 간단하고 직접적이며, 반전 기회를 포착하여 초과 수익을 얻습니다. 그러나 일부 위험도 존재하므로 신중한 실전 검증이 필요합니다. 매개변수 및 전략 구조 최적화를 통해 더 안정적이고 실전성이 강해질 수 있습니다.

Source

Pine

/*backtest

start: 2023-02-11 00:00:00

end: 2024-02-17 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("High Volume Low Breakout (Compounded Position Size)", overlay=true, initial_capital=1000)

// Define input for volume thresholdStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1