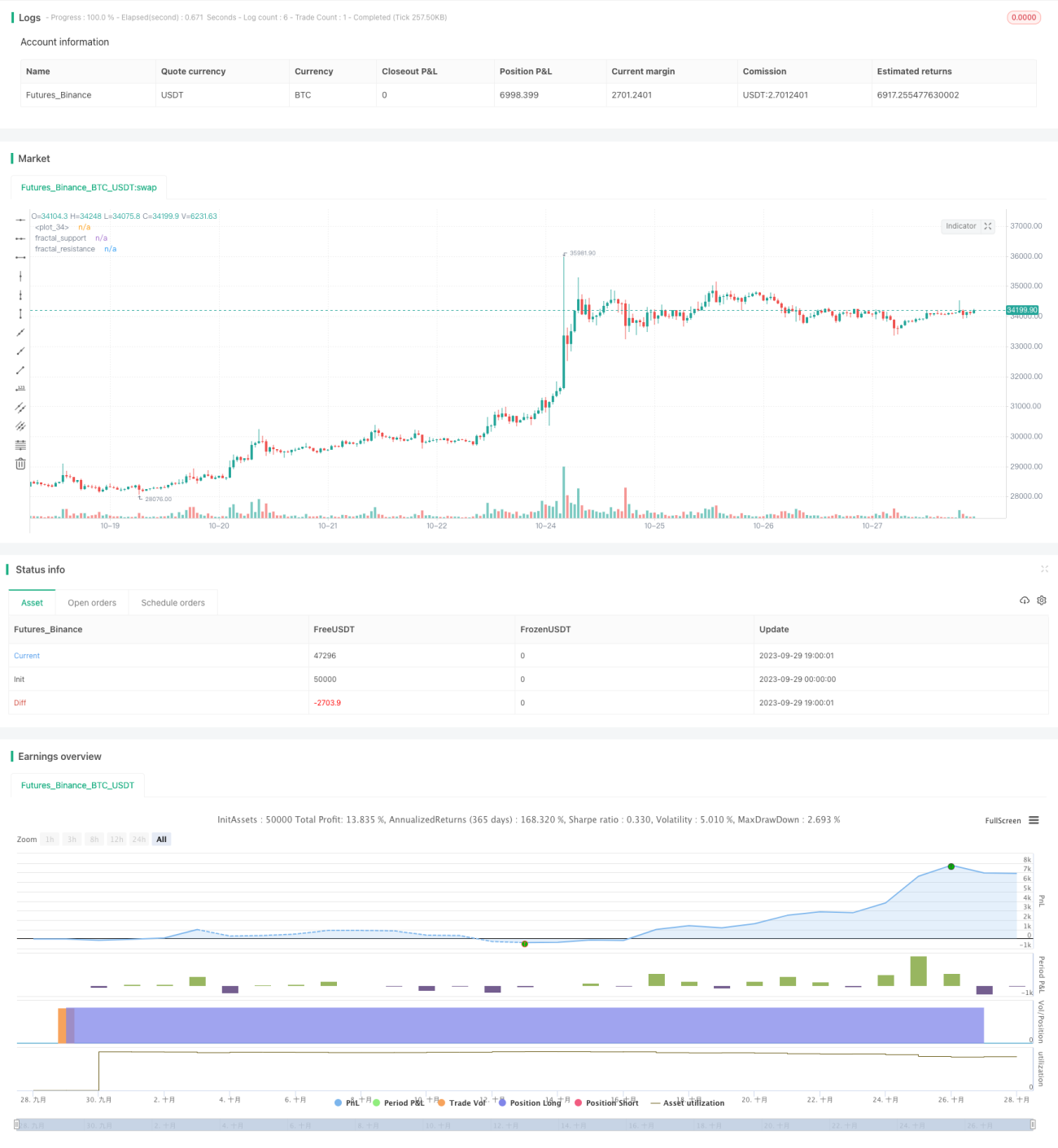

Strategi Perdagangan Pembalikan Berasaskan Sokongan/Rintangan Umum

Gambaran Keseluruhan

Strategi ini menggunakan dagangan songsang berdasarkan faktor bull/bear yang dikenal pasti melalui penunjuk, dan juga menetapkan sasaran keuntungan. Faktor bull/bear teras adalah berdasarkan "sokongan/rintangan umum" yang diperluaskan daripada volum dagangan, sesuai untuk instrumen dengan volum dan turun naik yang tinggi. Kelebihan strategi ini ialah ia dapat menangkap peluang pembalikan arah aliran jangka sederhana hingga pendek yang besar dan meraih keuntungan dengan cepat; namun, ia juga mempunyai risiko terperangkap dalam kedudukan yang rugi.

Prinsip Strategi

-

Mengenal pasti faktor bull/bear berdasarkan "sokongan/rintangan umum" dari volum dagangan

-

Menggunakan corak lilin untuk mengenal pasti sokongan/rintangan klasik, dengan volum besar digunakan untuk menapis penembusan palsu

-

Sokongan/rintangan umum lebih komprehensif berbanding corak klasik

-

Penembusan sokongan umum adalah isyarat faktor bull, penembusan rintangan umum adalah isyarat faktor bear

-

-

Dagangan songsang

-

Selepas isyarat faktor dikeluarkan, lakukan operasi songsang

-

Jika sudah ada kedudukan, kurangkan kedudukan secara songsang atau buka kedudukan songsang

-

-

Tetapkan sasaran keuntungan

-

Tetapkan henti rugi berdasarkan ATR

-

Tetapkan berbilang sasaran keuntungan seperti 1R/2R/3R

-

Kurangkan kedudukan secara berperingkat apabila mencapai sasaran keuntungan yang berbeza

-

Analisis Kelebihan

-

Dapat menangkap pembalikan arah yang besar dalam jangka sederhana hingga pendek

Penembusan sokongan/rintangan mewakili isyarat pembalikan arah aliran yang kukuh, dengan kebolehpercayaan tertentu, dan dapat menangkap pembalikan besar dalam jangka sederhana hingga pendek.

-

Meraih keuntungan dengan cepat, pengeluaran minimum

Melalui tetapan henti rugi dan pelbagai sasaran keuntungan, keuntungan cepat dapat dicapai dan pengeluaran individu dihadkan.

-

Sesuai untuk instrumen dengan dana institusi yang besar dan turun naik yang tinggi

Strategi ini bergantung pada penunjuk volum, memerlukan aliran masuk dana institusi yang mencukupi untuk menyokong arah aliran; pada masa yang sama, memerlukan ruang turun naik untuk merealisasikan keuntungan.

Analisis Risiko

-

Risiko terperangkap dalam pasaran berayun

Apabila pasaran berayun, operasi keluar henti rugi dan masuk semula secara songsang boleh menyebabkan kerap terperangkap.

-

Risiko kegagalan sokongan/rintangan

Sokongan/rintangan umum tidak semestinya boleh dipercayai, terdapat kebarangkalian ujian gagal dan pembalikan.

-

Risiko kedudukan sebelah

Strategi ini adalah semata-mata songsang, tidak mengambil kira pengesanan arah aliran, berpotensi terlepas peluang arah yang besar.

-

Dari segi pengurusan risiko

-

Keadaan faktor dagangan songsang boleh dilonggarkan sedikit, tidak perlu membalikkan setiap penembusan

-

Boleh digabungkan dengan penunjuk lain untuk penapisan, seperti perbezaan harga dan volum

-

Strategi henti rugi boleh dioptimumkan untuk mengurangkan kebarangkalian terperangkap

-

Hala Tuju Pengoptimuman

-

Optimumkan parameter julat

Optimumkan parameter sokongan/rintangan umum untuk mengenal pasti faktor yang lebih boleh dipercayai

-

Optimumkan strategi keuntungan

Boleh menambah lebih banyak peringkat sasaran keuntungan, atau menggunakan keuntungan sasaran tidak tetap

-

Optimumkan strategi henti rugi

Laraskan parameter ATR atau gunakan henti rugi berdasarkan statistik untuk mengurangkan kos transaksi akibat henti rugi yang terlalu agresif

-

Gabungkan arah aliran dan faktor lain

Boleh memperkenalkan purata bergerak dan sebagainya untuk pertimbangan arah aliran, mengelakkan pertentangan serius dengan arah aliran; juga boleh memperkenalkan faktor bantuan lain

Kesimpulan

Inti strategi ini adalah menggunakan dagangan songsang untuk menangkap pergerakan besar jangka sederhana hingga pendek. Ideanya mudah dan langsung, dengan pelarasan parameter boleh mencapai prestasi pasaran sebenar yang baik. Walau bagaimanapun, strategi songsang agresif, mempunyai risiko pengeluaran dan terperangkap, memerlukan pengoptimuman lanjut pada strategi henti rugi dan keuntungan, serta penggabungan pertimbangan arah aliran yang sesuai untuk mengurangkan kerugian yang tidak perlu.

- 1