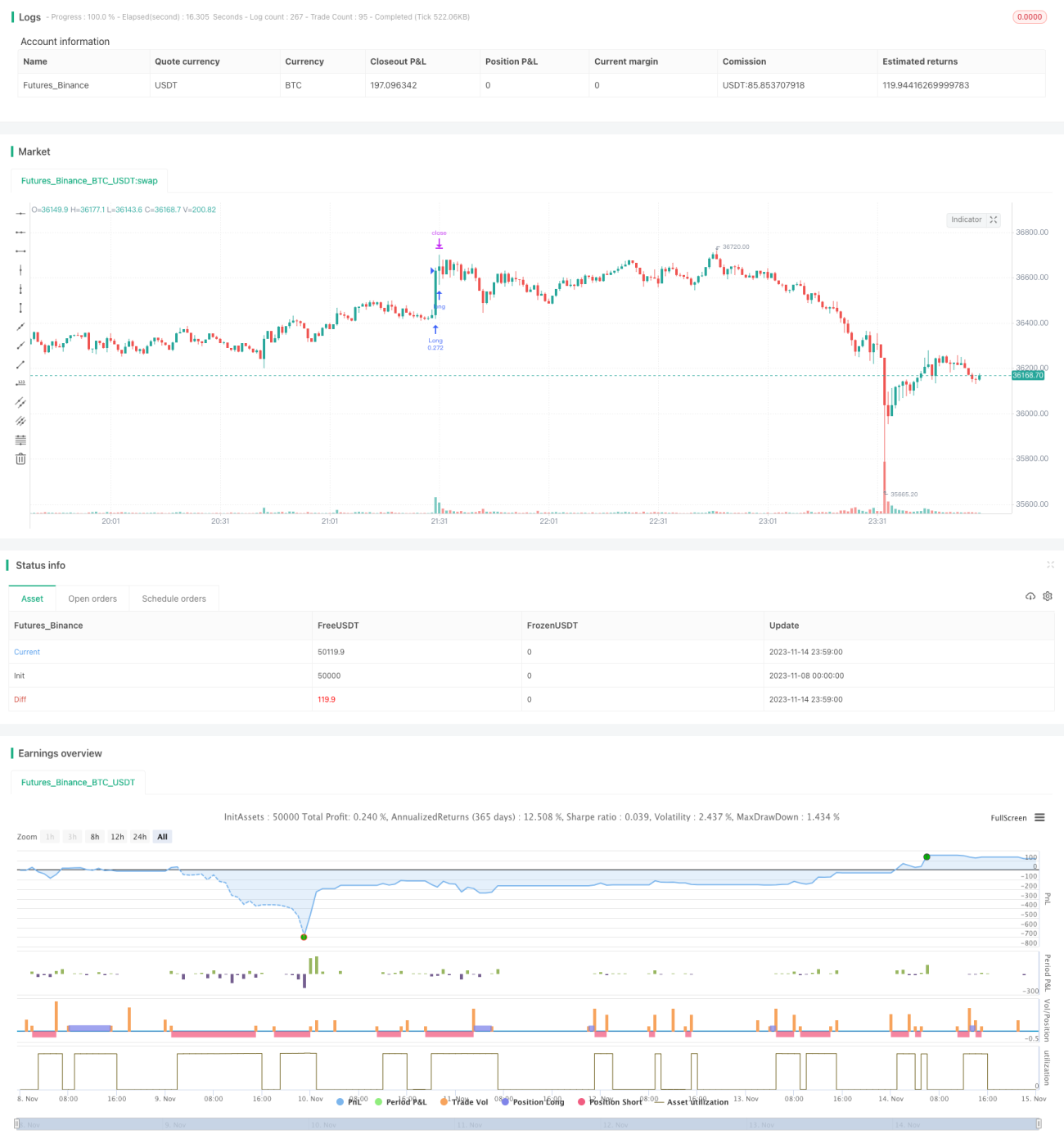

Strategi Pelbagai Trend

Gambaran Keseluruhan

Strategi ini menggunakan pelbagai indikator untuk mengenal pasti arah trend, mengikuti pendekatan penjejakan trend bagi menangkap peluang trend dalam jangka masa sederhana dan pendek. Strategi ini direka khusus untuk menjejak trend, bertujuan meningkatkan kadar kemenangan dan mengurangkan pengunduran.

Prinsip Strategi

- Menggunakan indikator WVAP untuk menilai nisbah harga;

- Indikator RSI untuk menilai momentum beli dan jual;

- Indikator QQE untuk mengenal pasti penembusan harga;

- Indikator ADX untuk menilai kekuatan trend;

- Coral Trend Indicator untuk menilai arah asas;

- Indikator LSMA untuk membantu menilai trend;

- Menggabungkan isyarat daripada pelbagai indikator untuk menghasilkan isyarat dagangan.

Strategi ini bergantung terutamanya pada RSI, QQE, ADX dan beberapa indikator lain untuk menilai arah dan kekuatan trend, serta menggunakan lengkung Coral Trend Indicator sebagai piawaian penilaian trend asas. Apabila indikator seperti RSI memberikan isyarat beli, dan Coral Trend Indicator juga menunjukkan lengkung menaik, maka kebarangkalian tinggi trend adalah menaik, dan strategi akan memilih untuk membeli. Indikator seperti WVAP digunakan terutamanya untuk menilai sama ada harga berada pada tahap yang munasabah, bagi mengelakkan pembelian di paras tinggi.

Kelebihan Strategi

- Gabungan pelbagai indikator meningkatkan ketepatan penilaian;

- Menekankan penjejakan trend, meningkatkan kebarangkalian keuntungan;

- Menggunakan pendekatan penembusan, menyaring pasaran julat dagangan;

- Menggabungkan indikator asas, mengelakkan dagangan berlawanan arah trend;

- Masa dagangan dan saiz lot yang ditetapkan adalah munasabah, mengurangkan risiko;

- Logik strategi jelas, mudah difahami dan dioptimumkan.

Kelebihan terbesar strategi ini ialah gabungan pelbagai indikator yang dapat mengurangkan kebarangkalian kesilapan daripada indikator tunggal, serta meningkatkan ketepatan penilaian. Pada masa yang sama, ia menekankan penjejakan trend dan pendekatan penembusan, yang membantu dalam menyaring peluang jangka sederhana dan pendek yang boleh dipercayai. Selain itu, strategi ini menggabungkan indikator asas, yang dapat mengelakkan dagangan berlawanan arah. Semua rekaan ini meningkatkan kestabilan strategi dan kebarangkalian keuntungan.

Risiko Strategi

- Terdapat kelewatan dalam penilaian beli dan jual, yang mungkin menyebabkan terlepas masa masuk yang terbaik;

- Kawalan pengunduran tidak sempurna, terdapat risiko pengunduran yang besar;

- Apabila arah asas berubah, strategi mungkin terlepas isyarat;

- Tidak mengambil kira kos dagangan, dalam aplikasi sebenar terdapat risiko penurunan keuntungan.

Risiko terbesar strategi ini ialah gabungan pelbagai indikator mungkin menyebabkan kelewatan penilaian, menyebabkan terlepas masa masuk yang terbaik dan seterusnya menjejaskan ruang keuntungan. Selain itu, kawalan pengunduran strategi ini tidak ideal, dengan risiko pengunduran yang besar. Apabila arah asas pasaran berubah tetapi indikator belum mencerminkannya, ia juga mudah menyebabkan kerugian. Dalam aplikasi sebenar, kos dagangan juga akan memberi kesan tertentu terhadap keuntungan.

Arah Pengoptimuman Strategi

- Menambah strategi henti rugi, mengoptimumkan kawalan pengunduran;

- Mengoptimumkan tetapan parameter, memendekkan kelewatan indikator;

- Menambah aplikasi indikator asas, meningkatkan ketepatan;

- Menggabungkan algoritma pembelajaran mesin untuk mencapai pengoptimuman parameter dinamik.

Tumpuan pengoptimuman strategi ini harus mempertimbangkan kawalan pengunduran, dengan menambah strategi henti rugi bergerak untuk mengunci keuntungan dan mengurangkan pengunduran. Pada masa yang sama, tetapan parameter boleh dioptimumkan untuk memendekkan kelewatan indikator, meningkatkan kepekaan strategi terhadap perubahan pasaran. Selain itu, indikator penilaian asas boleh ditambah lagi untuk meningkatkan ketepatan. Jika kaedah pembelajaran mesin dapat digunakan untuk mencapai pengoptimuman parameter dinamik, ia juga akan meningkatkan kestabilan strategi dengan ketara.

Rumusan

Strategi ini menggabungkan pelbagai indikator untuk menilai arah trend, direka dengan pendekatan penjejakan trend, bertujuan meningkatkan ketepatan penilaian dan kebarangkalian keuntungan. Strategi ini mempunyai kelebihan seperti gabungan indikator, penekanan pada penjejakan trend, dan penggabungan asas, tetapi juga mempunyai kelemahan seperti kelewatan dalam penilaian dan kawalan pengunduran yang tidak mencukupi. Pada masa hadapan, ia boleh diperbaiki melalui pengoptimuman tetapan parameter, penyempurnaan strategi henti rugi, penambahan indikator asas, dan lain-lain, supaya strategi mencapai prestasi yang lebih baik dalam aplikasi sebenar.

- 1