Gunakan strategi penjejakan keseimbangan purata bergerak Hull

Gambaran Keseluruhan

Strategi Jejak Keseimbangan menggunakan Purata Bergerak Hull sebagai penunjuk kemasukan utama untuk menilai arah aliran harga. Pada masa yang sama, strategi ini menggabungkan pelbagai penunjuk lain seperti garis dasar, penunjuk pengesahan dan lain-lain untuk mengesahkan arah aliran harga dan menapis isyarat palsu. Selepas kemasukan, strategi menggunakan Purata Julat Sebenar (ATR) untuk mengira henti rugi dinamik bagi menjejak keuntungan aliran.

Prinsip Strategi

Teras Strategi Jejak Keseimbangan ialah Purata Bergerak Hull. Purata Bergerak Hull lebih sensitif terhadap perubahan harga dan boleh menilai arah aliran dengan berkesan. Apabila harga menembusi ke atas garis Hull, ia mengesahkan pembentukan aliran menaik, jadi buka posisi beli; apabila harga menembusi ke bawah garis Hull, ia mengesahkan pembentukan aliran menurun, jadi buka posisi jual.

Selain itu, strategi ini juga memperkenalkan penunjuk garis dasar untuk menilai aliran jangka panjang dan pendek; penunjuk pengesahan untuk menapis penembusan palsu. Isyarat dagangan hanya akan dicetuskan apabila kedua-dua penunjuk garis dasar dan pengesahan mengesahkan arah aliran.

Selepas kemasukan, strategi menggunakan ATR dan Purata Bergerak Eksponen Hull untuk mengira Purata Julat Sebenar bagi menetapkan kedudukan henti rugi. Apabila aliran berterusan, garis henti rugi akan terus beralih ke atas/bawah untuk mengunci keuntungan aliran.

Analisis Kelebihan

Strategi Jejak Keseimbangan menggabungkan kelebihan penentuan aliran dan pengurusan risiko, dan boleh memperoleh pulangan yang baik dalam pasaran yang sedang dalam aliran. Berbanding dengan strategi henti rugi tetap, ia boleh menggunakan henti rugi bergerak untuk menjejak pergerakan aliran, mengelakkan henti rugi akibat turun naik pasaran biasa.

Gabungan pelbagai penunjuk juga menjadikan strategi ini lebih sensitif terhadap perubahan pasaran, sambil dapat menapis isyarat palsu dengan berkesan. Tambahan pula, strategi ini menyediakan beberapa parameter untuk pelarasan, dan pengguna boleh mengoptimumkannya berdasarkan penilaian mereka terhadap pasaran.

Analisis Risiko

Strategi ini bergantung terutamanya pada penunjuk aliran, dan mudah menghasilkan isyarat palsu dan henti rugi dalam pasaran yang mendatar (sideways). Selain itu, gabungan pelbagai penunjuk juga mungkin menyebabkan konflik isyarat. Penetapan parameter yang tidak sesuai juga boleh menyebabkan prestasi strategi yang lemah.

Pertimbangan boleh diberikan untuk menambah modul penilaian tambahan dalam strategi, seperti menghentikan dagangan apabila penunjuk bercanggah; atau menggunakan mekanisme undian untuk menggabungkan hasil penilaian pelbagai penunjuk. Dari segi penetapan parameter, parameter optimum boleh didapati melalui kaedah pengoptimuman ujian balik.

Arah Pengoptimuman

Strategi Jejak Keseimbangan boleh dioptimumkan dari beberapa arah berikut:

- Menambah modul penilaian, seperti modul turun naik (volatility), untuk menghentikan dagangan semasa turun naik tinggi;

- Menambah modul pembelajaran mesin, menggunakan algoritma pembelajaran mesin untuk menentukan pemberat penunjuk;

- Mengoptimumkan parameter penunjuk untuk mencari kombinasi parameter terbaik;

- Mengoptimumkan algoritma henti rugi bergerak supaya henti rugi dapat menjejak aliran dengan lebih baik;

- Menambah modul pengurusan risiko, seperti mengatasi henti rugi, pelarasan saiz posisi dinamik, dan lain-lain.

Kesimpulan

Secara keseluruhan, Strategi Jejak Keseimbangan adalah strategi penjejak aliran yang cemerlang. Ia berjaya menggabungkan penentuan aliran dengan henti rugi dinamik, dan boleh menjejak keuntungan aliran dengan berkesan. Melalui pengoptimuman lanjut, diharapkan prestasi strategi yang lebih baik dapat dicapai. Strategi ini memberikan rujukan yang baik untuk pembinaan strategi dagangan kuantitatif.

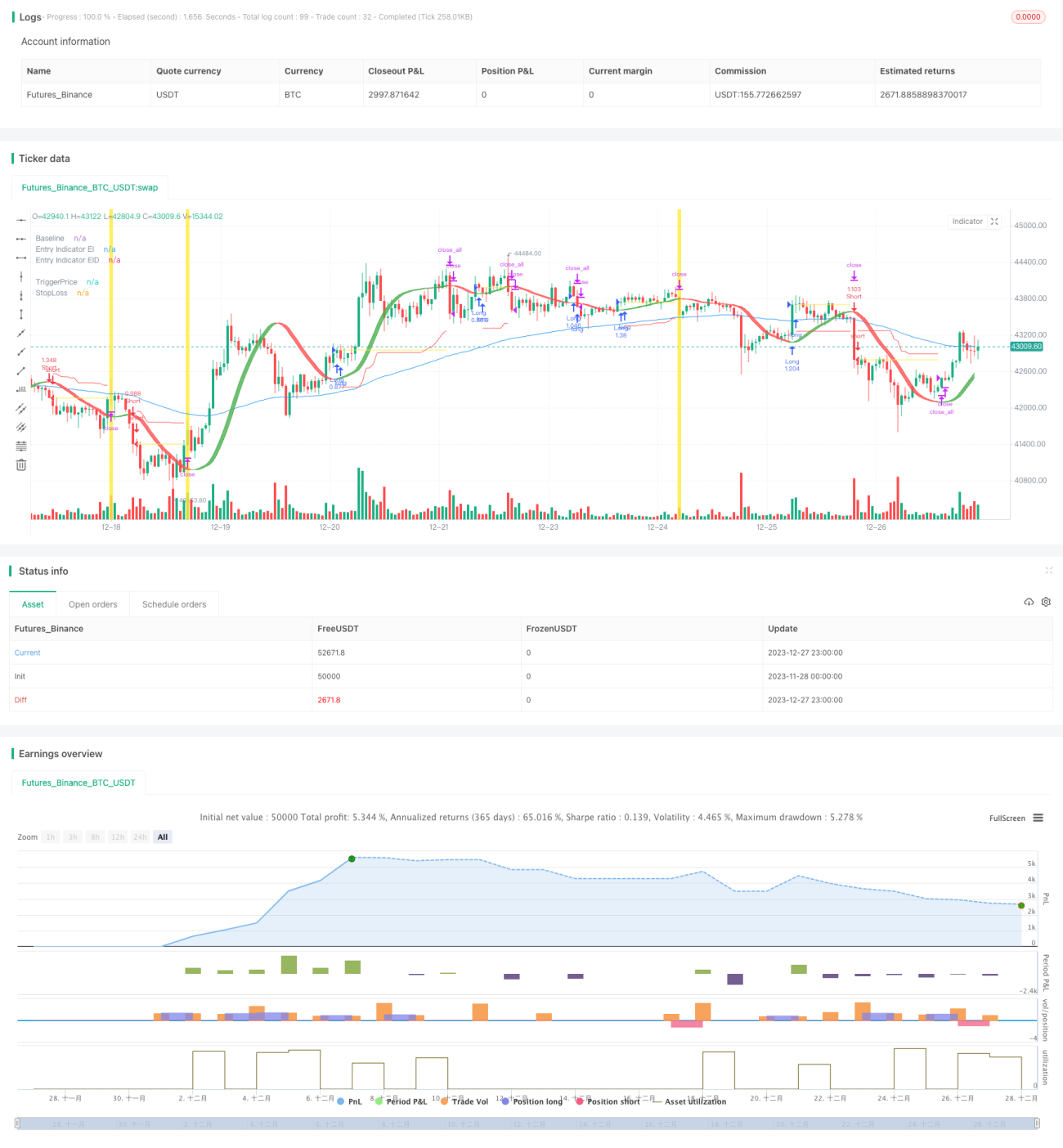

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1