Strategi Lanjutan Supertrend

Gambaran Keseluruhan

Strategi Supertrend Lanjutan adalah strategi yang dioptimumkan dan dinaik taraf berdasarkan indikator Supertrend klasik. Ia menggabungkan pergerakan harga, turun naik, dan pelbagai penunjuk teknikal untuk meningkatkan kualiti isyarat, mengurangkan bunyi, dan menangkap perubahan arah aliran pasaran dengan lebih tepat.

Prinsip Strategi

Inti strategi Supertrend Lanjutan adalah garis Supertrend. Ia dikira berdasarkan julat sebenar dan momentum harga untuk menilai potensi arah aliran dan titik perubahan harga. Apabila harga berada di atas garis Supertrend, ia menunjukkan arah aliran menaik; sebaliknya, ia menunjukkan arah aliran menurun.

Berbeza dengan indikator Supertrend klasik yang hanya mempertimbangkan harga penutup dan julat sebenar, strategi lanjutan ini juga menggabungkan pelbagai dimensi seperti volum dagangan, osilator momentum, dan data asas untuk mengesahkan kebolehpercayaan isyarat. Pendekatan multivariat ini memastikan isyarat dagangan yang dihasilkan lebih tepat dan boleh dipercayai, serta kurang terjejas oleh bunyi pasaran.

Analisis Kelebihan

Kelebihan utama strategi Supertrend Lanjutan adalah:

-

Penilaian arah aliran pasaran yang lebih tepat, menapis penembusan palsu. Strategi ini menunggu beberapa faktor penunjuk konsisten sebelum menghasilkan isyarat dagangan, yang dapat meningkatkan kadar kejayaan dengan ketara.

-

Mengurangkan gangguan bunyi pasaran. Dengan menggunakan gabungan penapis, sejumlah besar data pasaran yang tidak penting dapat diabaikan, menjadikan penilaian lebih jelas.

-

Pengurusan risiko yang optimum. Isyarat dagangan yang jelas membantu pedagang merancang titik henti rugi dan ambil untung dengan lebih baik, sekali gus mempunyai kawalan risiko yang lebih baik.

-

Kebolehsuaian yang tinggi. Selain mengenal pasti arah aliran, strategi ini juga boleh digabungkan dengan alat teknikal lain untuk membina sistem dagangan yang menyeluruh dan cekap.

Analisis Risiko

Strategi Supertrend Lanjutan juga mempunyai risiko utama berikut:

-

Risiko penetapan parameter. Gabungan parameter penunjuk yang tidak betul boleh menyebabkan strategi gagal atau menghasilkan terlalu banyak isyarat palsu.

-

Risiko kesilapan penilaian arah aliran. Tiada strategi yang dapat mengelakkan sepenuhnya risiko kesilapan penilaian; apabila arah aliran berubah secara tidak dijangka, kerugian mungkin berlaku.

-

Risiko pengoptimuman berlebihan. Apabila parameter dilaraskan ke tahap yang sangat tepat, ia akan terlalu bergantung pada data sejarah dan tidak dapat menyesuaikan diri dengan perubahan pasaran.

-

Risiko kos dagangan. Apabila kekerapan dagangan meningkat, kos dagangan seperti yuran dan gelinciran juga akan meningkat dengan ketara.

Penyelesaian yang sepadan:

-

Optimumkan tetapan parameter, lakukan ujian semula secara berkala untuk memeriksa kestabilan parameter.

-

Tetapkan henti rugi dan ambil untung untuk mengawal kerugian setiap dagangan.

-

Elakkan pengoptimuman berlebihan, kekalkan keupayaan generalisasi parameter.

-

Kira nisbah risiko-keuntungan isyarat untuk mengawal kos dagangan.

Hala Tuju Pengoptimuman

Strategi Supertrend Lanjutan boleh dioptimumkan dari beberapa aspek berikut:

-

Laraskan parameter mengikut pasaran yang berbeza agar lebih sesuai dengan ciri pasaran tersebut. Sebagai contoh, dalam pasaran yang tidak menentu, kitaran pengiraan boleh dipendekkan.

-

Tambah mekanisme penapisan adaptif. Apabila pasaran memasuki keadaan tertentu, parameter penunjuk dilaraskan secara automatik atau beberapa penapis dilumpuhkan.

-

Terokai kaedah pembelajaran mesin, gunakan rangkaian neural dan model latihan lain untuk mengoptimumkan parameter secara dinamik.

-

Gabungkan penunjuk sentimen dan berita, gunakan data tidak berstruktur untuk meningkatkan prestasi.

-

Tambah fungsi penskalaan kedudukan sasaran. Apabila kadar kemenangan sangat tinggi, keuntungan yang lebih besar boleh diperoleh dengan menambah lot.

Kesimpulan

Strategi Supertrend Lanjutan mengoptimumkan dan menambah baik indikator Supertrend klasik dengan memperkenalkan pelbagai penapis dan penunjuk pengesahan, yang membolehkan penilaian arah aliran pasaran yang lebih tepat dan kualiti isyarat yang lebih tinggi. Berbanding dengan penunjuk tunggal, strategi ini menawarkan penyelesaian dagangan yang lebih stabil, menyeluruh, dan cekap. Walau bagaimanapun, risiko pelarasan parameter yang tidak betul dan kesilapan penilaian perlu diberi perhatian, dan langkah kawalan risiko yang sesuai perlu diambil. Dengan pengoptimuman berterusan dan penggunaan bersama alat lain, strategi Supertrend Lanjutan mempunyai potensi aplikasi yang besar.

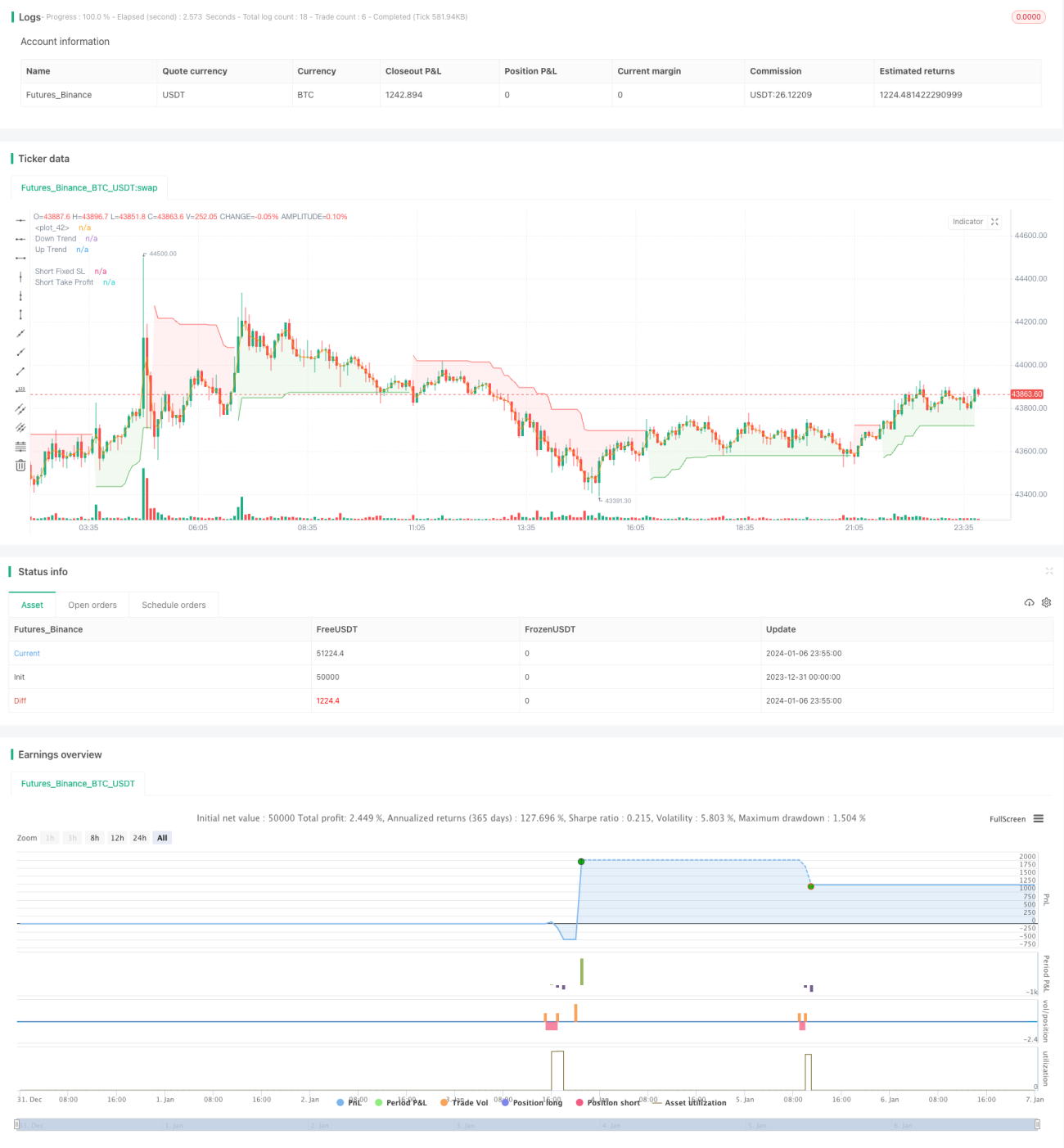

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1