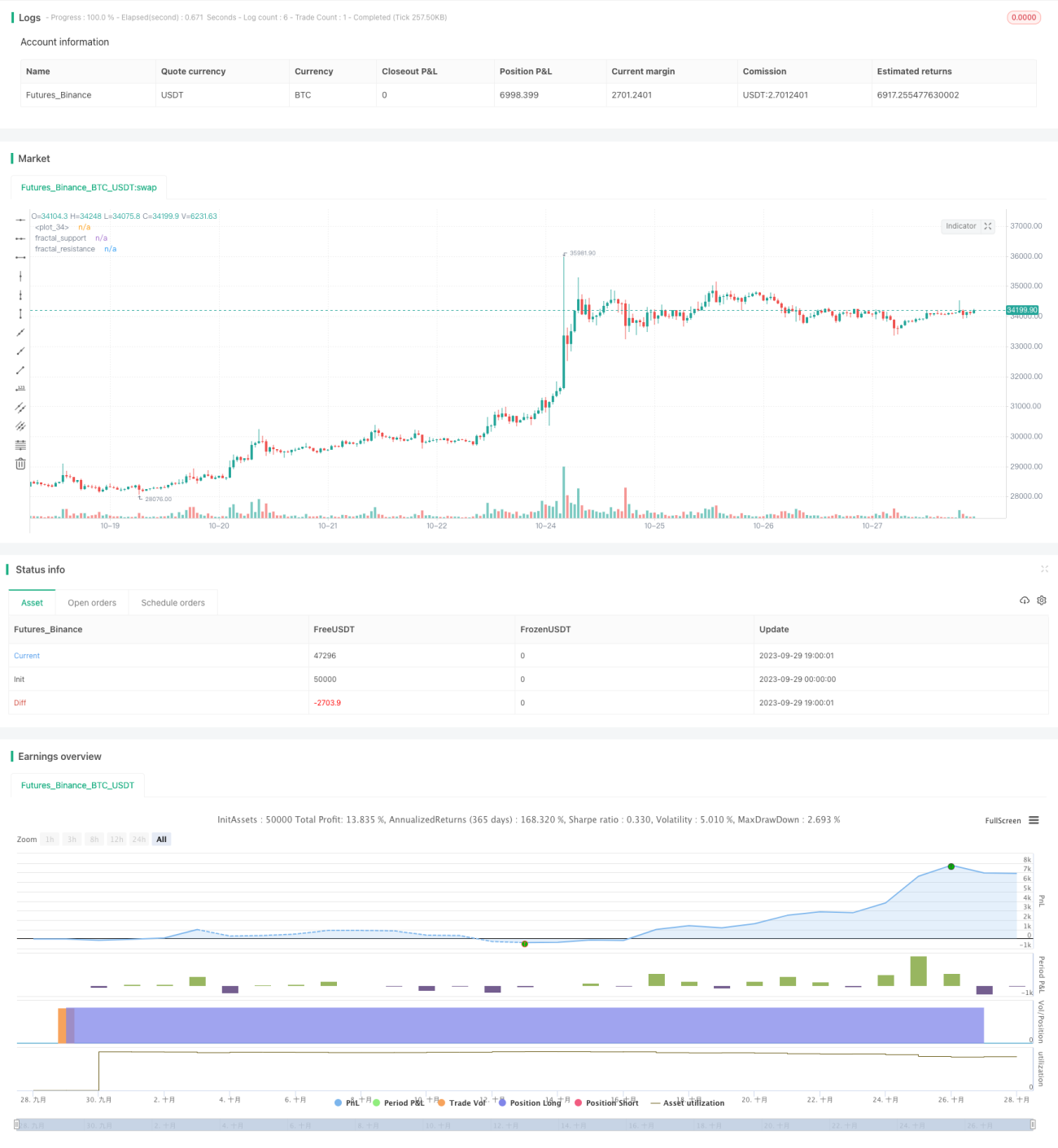

Estratégia de Reversão Baseada em Suporte/Resistência Generalizado

Visão Geral

Esta estratégia utiliza operações de reversão baseadas em fatores de alta/baixa (bullish/bearish factors) de indicadores, ao mesmo tempo que define pontos de lucro alvo. O núcleo do fator de alta/baixa é o "suporte/resistência generalizado", uma extensão baseada em volume, adequado para ativos com alto volume de negociação e volatilidade. A vantagem da estratégia é que ela pode capturar grandes oportunidades de reversão de tendência de curto a médio prazo e obter lucros rapidamente; no entanto, também existe o risco de ficar preso.

Princípio da Estratégia

-

Identificação do fator de alta/baixa com base no "suporte/resistência generalizado" baseado em volume

- Utiliza padrões de candlestick para identificar suporte/resistência clássicos, filtrando falsos rompimentos com alto volume.

- O suporte/resistência generalizado tem melhor abrangência do que os padrões clássicos.

- Rompimento do suporte generalizado gera sinal de fator de alta; rompimento da resistência generalizada gera sinal de fator de baixa.

-

Operações de reversão

- Após o sinal do fator, realiza-se a operação oposta.

- Se já houver posição, reduz-se a posição na direção oposta ou abre-se posição reversa.

-

Definição de metas de lucro

- Utiliza ATR para definir stop loss.

- Define múltiplos alvos de lucro, como 1R, 2R, 3R, etc.

- Reduz posições gradualmente ao atingir diferentes alvos de lucro.

Análise de Vantagens

-

Capaz de capturar grandes reversões de curto a médio prazo

O rompimento de suporte/resistência representa um sinal forte de reversão de tendência, com certa confiabilidade, permitindo capturar movimentos significativos de reversão de curto a médio prazo. -

Lucros rápidos e baixo drawdown

Através da definição de stop loss e múltiplos alvos de lucro, é possível obter lucros rapidamente e limitar o drawdown do ativo. -

Adequado para ativos com grande fluxo de capital institucional e alta volatilidade

A estratégia depende de indicadores de volume, exigindo influxo suficiente de capital institucional para sustentar a tendência; além disso, precisa de um certo espaço de volatilidade para obter lucros.

Análise de Riscos

-

Risco de ficar preso em movimentos laterais

Em mercados laterais, as operações de saída com stop loss e reentrada reversa podem causar perdas frequentes por ficar preso. -

Risco de falha dos níveis de suporte/resistência

O suporte/resistência generalizado não é absolutamente confiável; existe probabilidade de falha no teste de reversão. -

Risco de posição direcional única

A estratégia é puramente reversora, sem considerar o acompanhamento de tendência, podendo perder grandes oportunidades direcionais. -

Gestão de risco

- Pode-se relaxar as condições do fator para operações de reversão, não sendo necessário reverter a cada rompimento.

- Pode-se combinar outros indicadores para filtragem, como divergência de preço-volume.

- Pode-se otimizar a estratégia de stop loss para reduzir a probabilidade de ficar preso.

Direções de Otimização

-

Otimizar parâmetros de escala

Otimizar os parâmetros do suporte/resistência generalizado para identificar fatores mais confiáveis. -

Otimizar estratégia de lucro

Pode-se adicionar mais níveis de alvos de lucro ou adotar alvos de lucro não fixos. -

Otimizar estratégia de stop loss

Ajustar os parâmetros do ATR ou usar stop loss baseado em volatilidade para reduzir custos de negociação causados por stops excessivamente agressivos. -

Combinar tendência e outros fatores

Pode-se introduzir médias móveis ou outros indicadores de tendência para evitar forte contraposição à tendência; também é possível adicionar fatores auxiliares.

Resumo

O núcleo desta estratégia é capturar grandes flutuações de curto a médio prazo usando negociações de reversão. A ideia da estratégia é simples e direta, podendo obter bons resultados em negociação real com ajustes de parâmetros. No entanto, por ser uma estratégia de reversão agressiva, existem riscos de drawdown e de ficar preso, sendo necessário otimizar ainda mais as estratégias de stop loss e lucro, além de incorporar adequadamente a análise de tendência para reduzir perdas desnecessárias.

- 1