Estratégia de Captura de Volatilidade Dinâmica com RSI e Bandas de Bollinger

Visão Geral

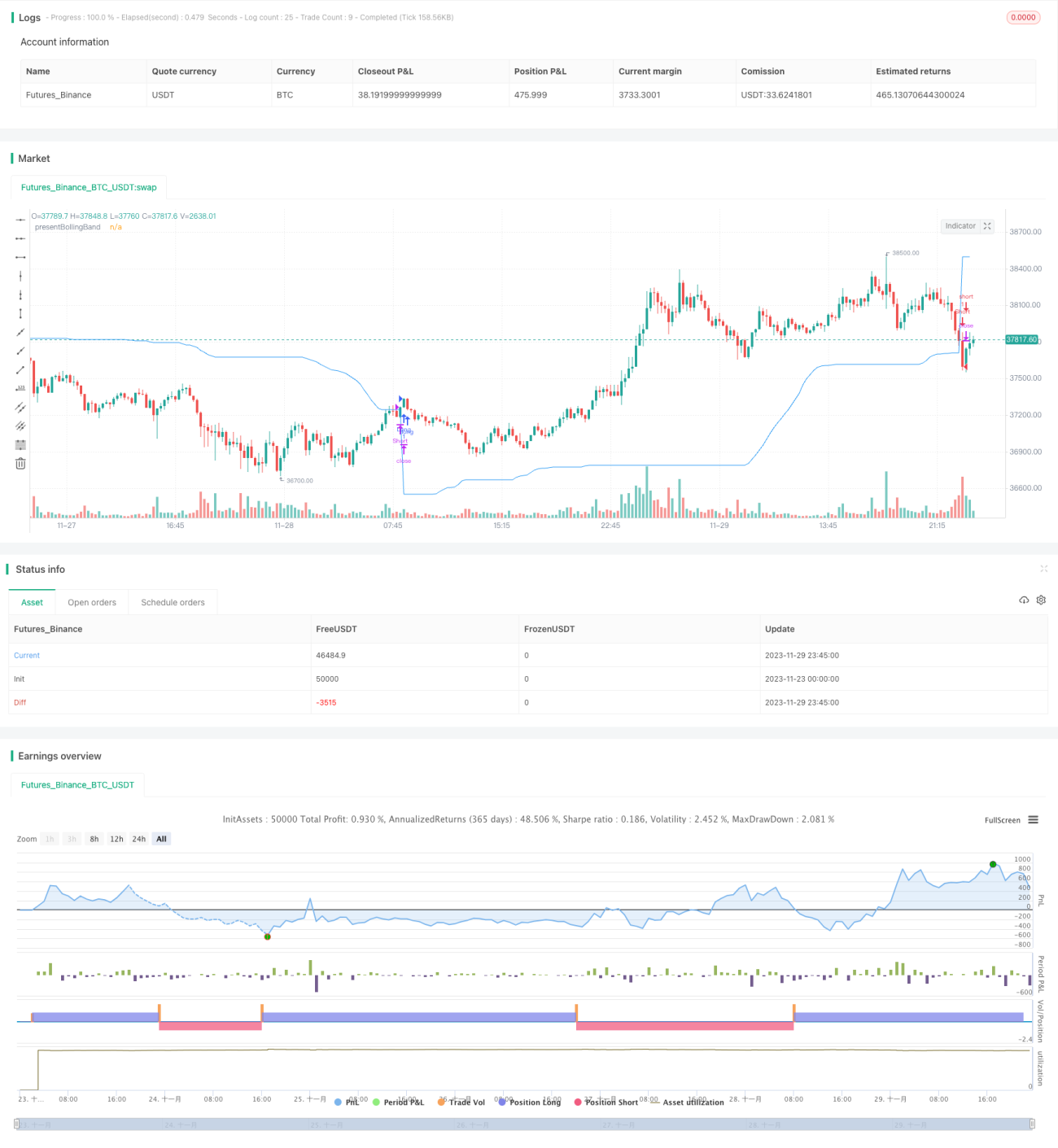

A Estratégia de Captura de Amplitude Dinâmica com RSI e Bandas de Bollinger é uma estratégia de negociação que integra os conceitos de Bandas de Bollinger (BB), Índice de Força Relativa (RSI) e Média Móvel Simples (SMA). A singularidade desta estratégia reside no fato de que ela calcula um nível dinâmico entre a banda superior e inferior com base no preço de fechamento. Essa funcionalidade exclusiva permite que a estratégia se adapte à volatilidade do mercado e às variações de preço.

Os mercados de criptomoedas e ações são altamente voláteis, tornando-os adequados para estratégias com Bandas de Bollinger. O RSI ajuda a identificar condições de sobrecompra e sobrevenda, comuns nesses mercados frequentemente especulativos.

Princípio da Estratégia

Bandas de Bollinger Dinâmicas: A estratégia primeiro calcula as bandas superior e inferior de Bollinger com base no comprimento e multiplicador definidos pelo usuário. Em seguida, combina as Bandas de Bollinger e o preço de fechamento para ajustar dinamicamente o valor de presentBollingBand. Por fim, quando o preço cruza a present BollingBand para cima, gera um sinal de compra (long); quando cruza para baixo, gera um sinal de venda (short).

RSI: Se o usuário optar por usar o RSI para gerar sinais, a estratégia também calcula o RSI e sua SMA, utilizando-os para gerar sinais adicionais de compra e venda. Os sinais baseados em RSI são usados apenas quando a opção "Usar RSI para gerar sinais" está definida como true.

Em seguida, a estratégia verifica a direção de negociação selecionada e entra em posições compradas ou vendidas de acordo. Se a direção de negociação for definida como "Ambos", a estratégia pode entrar em posições compradas e vendidas simultaneamente.

Por fim, as posições compradas são fechadas quando o preço de fechamento cruza a present BollingBand para baixo; as posições vendidas são fechadas quando o preço de fechamento cruza a present BollingBand para cima.

Análise de Vantagens

A estratégia combina as vantagens dos indicadores Bandas de Bollinger, RSI e SMA, sendo capaz de se adaptar à volatilidade do mercado, capturar amplitude dinamicamente e gerar sinais de negociação em condições de sobrecompra e sobrevenda.

O indicador RSI complementa os sinais das Bandas de Bollinger, evitando entradas equivocadas em mercados laterais. Permite escolher entre operar apenas comprado, apenas vendido ou ambos, adaptando-se a diferentes condições de mercado.

Os parâmetros são personalizáveis, permitindo ajustes conforme a tolerância ao risco individual.

Análise de Riscos

A estratégia depende de indicadores técnicos, não sendo capaz de lidar com grandes mudanças fundamentais.

Parâmetros inadequados das Bandas de Bollinger podem resultar em sinais de negociação muito frequentes ou muito raros.

O risco de negociar nos dois sentidos é maior, exigindo cautela com perdas em posições vendidas contrárias.

Recomenda-se o uso de stop loss para controlar o risco.

Direções de Otimização

-

Combinar com outros indicadores para filtrar sinais, como o MACD.

-

Adicionar estratégias de stop loss.

-

Otimizar os parâmetros das Bandas de Bollinger e do RSI.

-

Ajustar parâmetros de acordo com diferentes ativos e períodos.

-

Considerar otimização em ambiente real para ajustar parâmetros conforme as condições práticas.

Resumo

A Estratégia de Captura de Amplitude Dinâmica com RSI e Bandas de Bollinger é uma estratégia orientada por indicadores técnicos, combinando as vantagens das Bandas de Bollinger, RSI e SMA. Através do ajuste dinâmico das Bandas de Bollinger, captura a volatilidade do mercado. A estratégia oferece grande espaço para personalização e otimização, mas não consegue prever mudanças fundamentais. Recomenda-se validar os resultados em ambiente real e, se necessário, ajustar parâmetros ou adicionar outros indicadores para reduzir riscos.

- 1