Estratégia de negociação baseada na tendência de ondas

Visão Geral

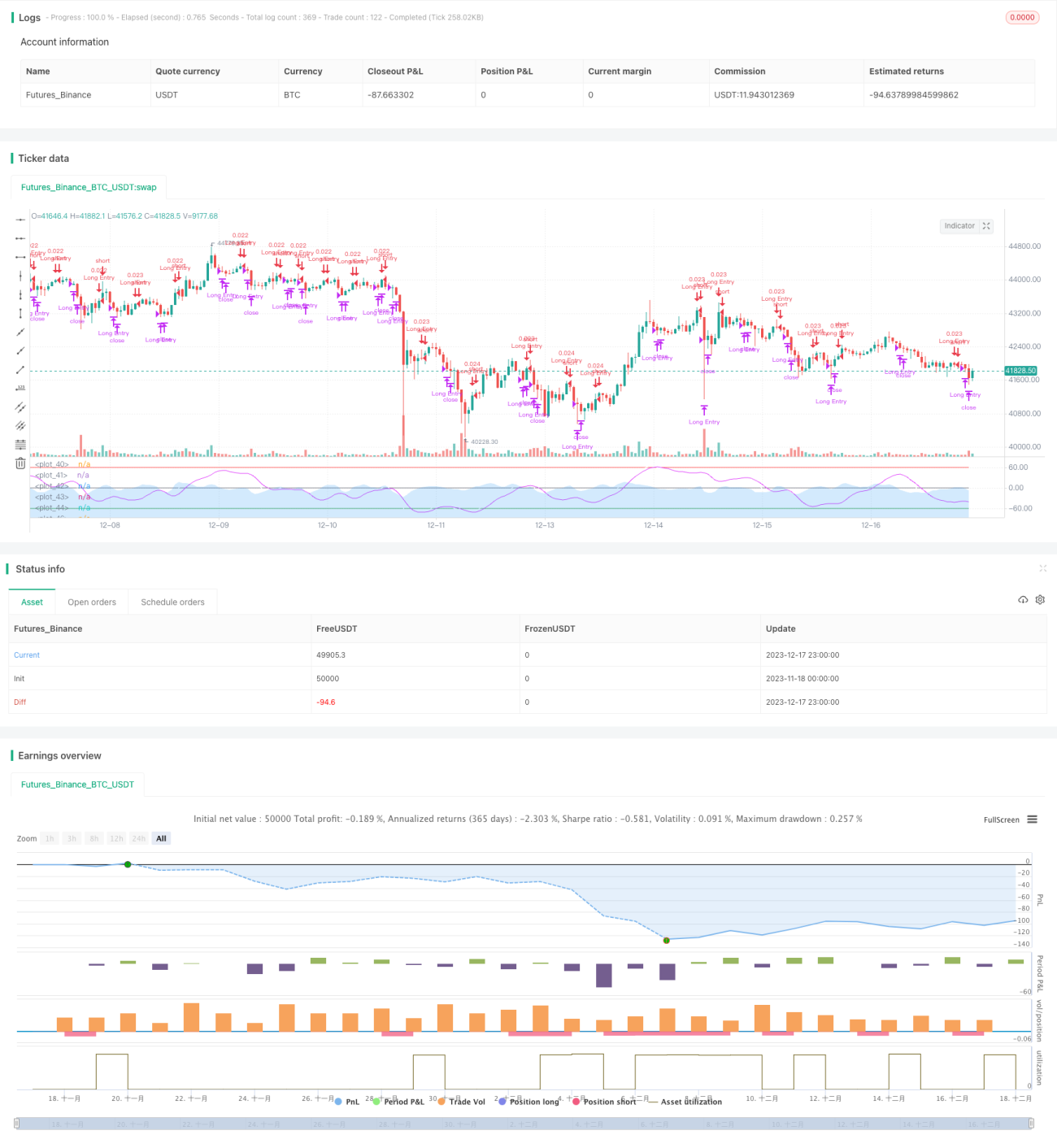

Esta é uma estratégia de negociação baseada no indicador de tendência de ondas de LazyBear. A estratégia calcula a tendência das ondas das flutuações de preço para identificar condições de sobrecompra e sobrevenda no mercado, realizando operações de compra (long) e venda (short).

Princípio da Estratégia

A estratégia baseia-se principalmente no indicador de tendência de ondas de LazyBear. Primeiro, calcula-se o preço médio (AP), em seguida, a média móvel exponencial (ESA) do AP e a média móvel exponencial da variação absoluta de preço (D). Com base nisso, calcula-se o índice de volatilidade (CI) e, em seguida, a média móvel exponencial do CI, obtendo a linha de tendência de ondas (WT). Posteriormente, a WT é suavizada por médias móveis simples, gerando WT1 e WT2. Quando WT1 cruza acima de WT2, forma-se um cruzamento dourado (golden cross), indicando compra; quando WT1 cruza abaixo de WT2, forma-se um cruzamento da morte (death cross), indicando venda.

Análise de Vantagens

Esta é uma estratégia de acompanhamento de tendência muito simples, porém extremamente prática. Suas principais vantagens são:

- Baseia-se no indicador de tendência de ondas, permitindo identificar claramente a direção do preço e o sentimento do mercado.

- Utiliza o cruzamento dourado e o cruzamento da morte da WT para determinar pontos de compra e venda, com operação simples.

- Permite personalizar os parâmetros para ajustar a sensibilidade da linha WT, adaptando-se a diferentes períodos.

- É possível adicionar condições adicionais para filtrar sinais, como limitar a janela de tempo de negociação.

Análise de Riscos

A estratégia também apresenta alguns riscos:

- Como estratégia de acompanhamento de tendência, pode gerar muitos sinais falsos em mercados laterais (consolidação).

- A linha WT possui inerentemente um atraso significativo, podendo perder pontos de reversão rápidos do preço.

- Os parâmetros padrão podem não ser adequados para todos os ativos e prazos, exigindo otimização.

- Não possui mecanismo de stop loss, podendo resultar em posições mantidas por tempo excessivo.

As principais formas de mitigação são:

- Otimizar os parâmetros para ajustar a sensibilidade da linha WT.

- Adicionar outros indicadores para confirmação, evitando sinais falsos.

- Definir stop loss e take profit.

- Limitar o número de negociações por dia ou o tamanho da posição.

Direções de Otimização

A estratégia ainda apresenta espaço para otimização adicional:

- Otimizar os parâmetros da WT para torná-la mais sensível ou mais estável.

- Utilizar diferentes combinações de parâmetros para diferentes prazos.

- Adicionar indicadores de preço e volume, indicadores de volatilidade, etc., como sinais de confirmação.

- Incorporar lógica de stop loss e take profit.

- Enriquecer as formas de posicionamento, como pirâmide, grid trading, etc.

- Combinar métodos de aprendizado de máquina para extrair melhores características e regras de negociação.

Resumo

Esta estratégia é uma estratégia de acompanhamento de tendência de ondas muito simples e prática. Ela calcula a tendência das flutuações de preço, identifica condições de sobrecompra e sobrevenda do mercado e gera sinais de negociação através dos cruzamentos dourado e da morte da linha WT. A estratégia é de fácil implementação e operação. No entanto, como estratégia de tendência, sua sensibilidade e estabilidade em relação ao preço precisam de otimização adicional, além da necessidade de combiná-la com outros indicadores e lógicas para evitar sinais falsos. No geral, é um modelo de estratégia muito prático, com grande potencial de otimização.

- 1