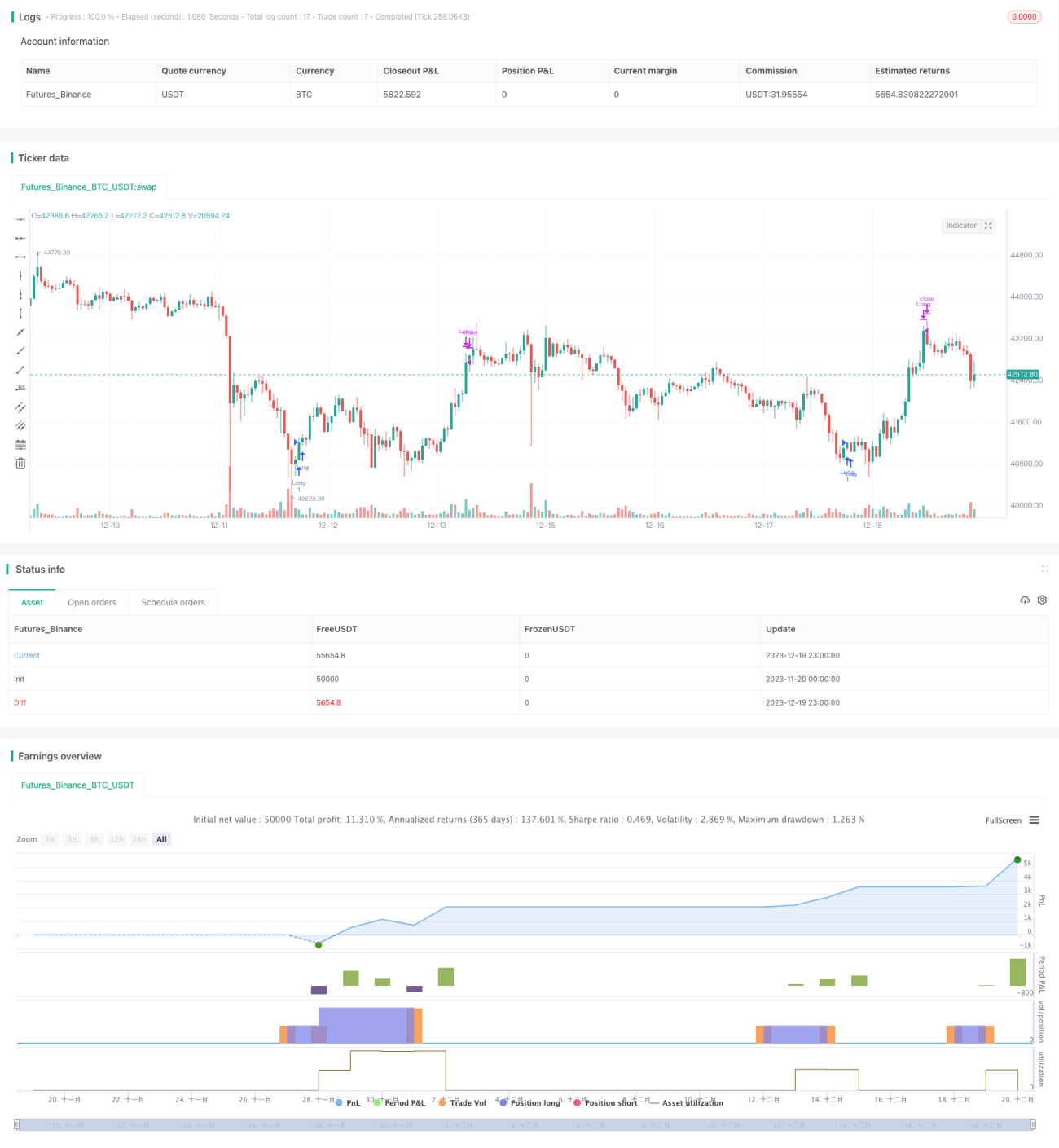

Estratégia de negociação de múltiplos períodos de tempo baseada em indicador de volatilidade e indicador estocástico

Visão Geral

Esta estratégia combina o indicador de volatilidade VIX e o indicador estocástico RSI, através da combinação de indicadores de diferentes períodos de tempo, para realizar compras de rompimento eficientes e stop-loss de sobrecompra/sobrevenda. A estratégia possui grande espaço de otimização, podendo adaptar-se a diferentes ambientes de mercado.

Princípio da Estratégia

-

Calcular o indicador de volatilidade VIX: utilizar a máxima e mínima dos últimos 20 dias para calcular a volatilidade. Quando a volatilidade está acima da banda superior, indica pânico no mercado; quando está abaixo da banda inferior, indica Complacency no mercado.

-

Calcular o indicador RSI estocástico: utilizar os ganhos/perdas dos últimos 14 dias para calcular. Quando o RSI está acima de 70, é zona de sobrecompra; quando abaixo de 30, é zona de sobrevenda.

-

Combinar os dois indicadores: quando a volatilidade estiver acima da banda superior ou no percentil máximo, comprar (long); quando o RSI estiver acima de 70, fechar a posição.

Vantagens da Estratégia

- Combina múltiplos indicadores para uma avaliação abrangente dos pontos de mercado.

- Indicadores de diferentes períodos de tempo se confirmam mutuamente, aumentando a precisão das decisões.

- Parâmetros podem ser otimizados e ajustados para se adaptar a diferentes instrumentos de negociação.

Análise de Risco

- A configuração inadequada de parâmetros pode gerar múltiplos sinais falsos.

- Um único indicador de fechamento pode facilmente perder reversões de preço.

Sugestões de Otimização

- Adicionar mais indicadores de confirmação, como médias móveis, Bandas de Bollinger, etc., para determinar o momento de entrada.

- Adicionar mais indicadores de fechamento, como padrões de candlestick de reversão, etc.

Conclusão

Esta estratégia utiliza o indicador VIX para avaliar o timing e o nível de risco do mercado, combinado com o indicador RSI para filtrar pontos de negociação desfavoráveis de sobrecompra e sobrevenda, permitindo assim comprar em momentos eficientes e fazer stop-loss de forma oportuna. A estratégia possui grande espaço de otimização, podendo adaptar-se a uma gama mais ampla de ambientes de mercado.

- 1