Estratégia de acompanhamento de tendência com cruzamento e reversão de indicador de momentum

Visão Geral

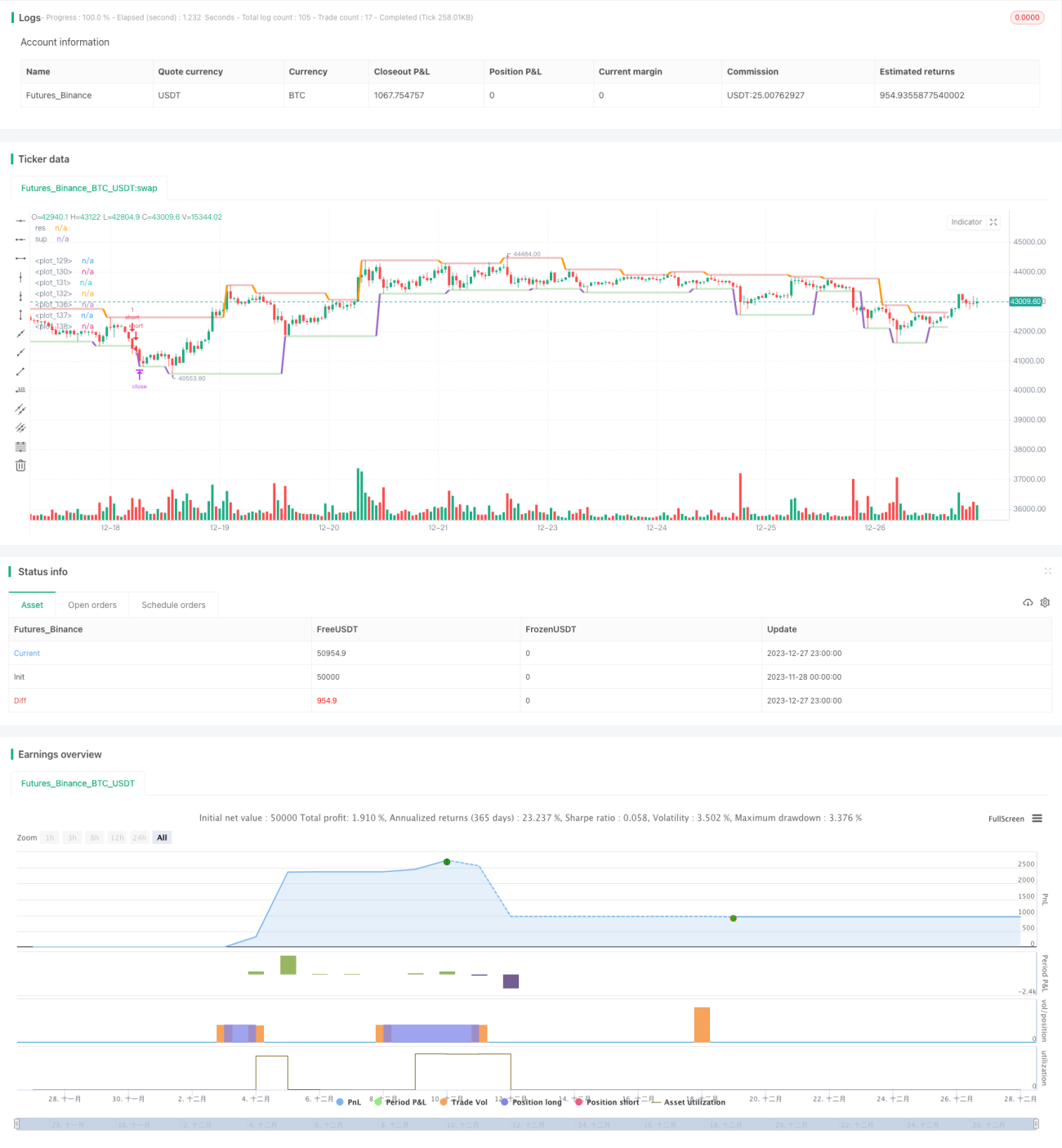

Esta estratégia combina múltiplos indicadores de momentum, como MACD, RSI e ADX, para identificar sinais de reversão de preços, adotando uma abordagem contrária, entrando na direção oposta quando a tendência forte se inverte. A estratégia também define stop loss e take profit para garantir lucros e controlar riscos.

Princípio da Estratégia

A estratégia primeiro analisa se ocorre um cruzamento de ouro ou cruzamento da morte entre as médias rápidas e lentas do indicador MACD para determinar a tendência de preço; em seguida, combina o indicador RSI para filtrar falsos rompimentos, garantindo que apenas reversões reais de preço gerem sinais; por fim, utiliza o indicador ADX para verificar novamente se o preço está em estado de tendência. Somente quando todas essas condições são atendidas simultaneamente é que um sinal de compra ou venda é gerado.

Especificamente, quando a linha rápida do MACD cruza acima da linha lenta, o RSI está acima de 50 e subindo, e o ADX está acima de 20, gera-se um sinal de compra; quando a linha rápida do MACD cruza abaixo da linha lenta, o RSI está abaixo de 50 e caindo, e o ADX está acima de 20, gera-se um sinal de venda.

Análise de Vantagens

A maior vantagem desta estratégia é o uso combinado de vários indicadores, que filtra efetivamente mercados laterais e sinais errôneos, capturando verdadeiros pontos de reversão de tendência, resultando em uma alta taxa de acerto. Além disso, a definição de stop loss e take profit para garantir lucros e controlar riscos pode mitigar efetivamente o impacto de eventos inesperados.

Análise de Riscos

O maior risco desta estratégia é o erro na identificação da reversão de tendência, como quando o preço sofre uma correção profunda, levando a um falso julgamento. Além disso, a nova tendência após a reversão pode não ter sustentação suficiente para gerar lucros adequados.

A solução é otimizar ainda mais os parâmetros, ajustar a amplitude do stop loss ou combinar mais indicadores auxiliares para filtrar os sinais.

Direções de Otimização

Esta estratégia pode ser otimizada nas seguintes áreas:

-

Otimizar a combinação de parâmetros do MACD e RSI para melhorar a precisão na identificação de reversões de preço.

-

Adicionar mais indicadores de filtro, como KD, BOLL, etc., criando um efeito de envolvimento de indicadores.

-

Ajustar dinamicamente a amplitude do stop loss conforme diferentes condições de mercado.

-

Modificar o take profit em tempo real com base no movimento real após a reversão.

Resumo

Esta estratégia combina múltiplos indicadores de momentum para identificar oportunidades potenciais de reversão de preço. Através da otimização de parâmetros, da combinação de mais indicadores auxiliares e do ajuste dinâmico das estratégias de stop loss e take profit, é possível aumentar ainda mais a estabilidade e confiabilidade da estratégia, capturando diversas oportunidades de negociação oferecidas pelo mercado.

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © AHMEDABDELAZIZZIZO

//@version=5- 1