Estratégia Avançada de SuperTrend

Visão Geral

A estratégia avançada de supertendência é uma otimização e aprimoramento do clássico indicador de supertendência. Ela combina ação de preço, volatilidade e múltiplos indicadores técnicos, visando melhorar a qualidade dos sinais, reduzir ruídos e capturar com mais precisão as mudanças nas tendências do mercado.

Princípio da Estratégia

O núcleo da estratégia avançada de supertendência é a linha de supertendência. Ela é calculada com base no Average True Range (ATR) e no momentum do preço, sendo usada para identificar possíveis tendências e pontos de reversão de preço. Quando o preço está acima da linha de supertendência, indica tendência de alta; caso contrário, indica tendência de baixa.

Diferente do indicador de supertendência tradicional, que considera apenas o preço de fechamento e o ATR, a estratégia avançada também incorpora múltiplas dimensões como volume, oscilador de momentum e dados fundamentais para verificar a confiabilidade dos sinais. Essa abordagem multivariável garante que os sinais de negociação gerados sejam mais precisos e robustos, menos suscetíveis a ruídos de mercado.

Análise de Vantagens

As principais vantagens da estratégia avançada de supertendência são:

-

Maior precisão na identificação das tendências de mercado, filtrando falsos rompimentos. Essa estratégia espera que múltiplos fatores e indicadores estejam alinhados antes de gerar um sinal, aumentando significativamente a taxa de acerto.

-

Redução da interferência de ruídos de mercado. Ao combinar filtros, é possível eliminar grande parte dos dados irrelevantes, tornando as decisões mais claras.

-

Otimização da gestão de risco. Sinais de negociação claros ajudam o trader a definir melhor stop loss e take profit, proporcionando um controle de risco superior.

-

Alta adaptabilidade. Além de identificar tendências, a estratégia pode ser combinada com outras ferramentas técnicas para construir um sistema de negociação completo e eficiente.

Análise de Riscos

A estratégia avançada de supertendência também apresenta os seguintes riscos principais:

-

Risco de configuração de parâmetros. Uma combinação inadequada de parâmetros dos indicadores pode tornar a estratégia ineficaz ou gerar muitos sinais falsos.

-

Risco de erro na identificação da tendência. Nenhuma estratégia pode evitar completamente erros; mudanças inesperadas na tendência podem resultar em perdas.

-

Risco de overfitting. Ajustar parâmetros com extrema precisão pode tornar a estratégia excessivamente dependente de dados históricos, incapaz de se adaptar a mudanças de mercado.

-

Risco de custos de negociação. Com o aumento do número de negociações, custos como comissões e slippage também aumentam significativamente.

Soluções correspondentes:

-

Otimizar a configuração dos parâmetros e realizar backtests periódicos para verificar a robustez dos mesmos.

-

Definir stop loss e take profit para controlar perdas individuais.

-

Evitar overfitting, mantendo a capacidade de generalização dos parâmetros.

-

Calcular a relação risco-retorno dos sinais para controlar os custos de negociação.

Direções de Otimização

A estratégia avançada de supertendência pode ser otimizada nos seguintes aspectos:

-

Ajustar os parâmetros de acordo com diferentes mercados para melhor se adequar às características de cada um. Por exemplo, em mercados voláteis, pode-se encurtar os períodos de cálculo.

-

Adicionar um mecanismo de filtragem adaptativa. Quando o mercado entra em um estado específico, ajustar automaticamente os parâmetros dos indicadores ou desabilitar certos filtros.

-

Explorar métodos de aprendizado de máquina, como redes neurais, para treinar modelos que otimizem dinamicamente os parâmetros.

-

Incorporar indicadores de sentimento e notícias financeiras, utilizando dados não estruturados para melhorar o desempenho.

-

Adicionar funcionalidade de dimensionamento de posição alvo. Quando a taxa de acerto é muito alta, pode-se aumentar a posição para obter maiores ganhos.

Conclusão

A estratégia avançada de supertendência, ao introduzir múltiplos filtros e indicadores de confirmação, otimiza e aprimora o clássico indicador de supertendência, permitindo identificar as tendências de mercado com mais precisão e melhorar a qualidade dos sinais. Comparada a um único indicador, essa estratégia oferece uma abordagem de negociação mais robusta, completa e eficiente. No entanto, é necessário estar atento aos riscos de parâmetros mal ajustados e erros de julgamento, adotando medidas adequadas de controle de risco. Com contínua otimização e combinação com outras ferramentas, a estratégia avançada de supertendência possui grande potencial de aplicação.

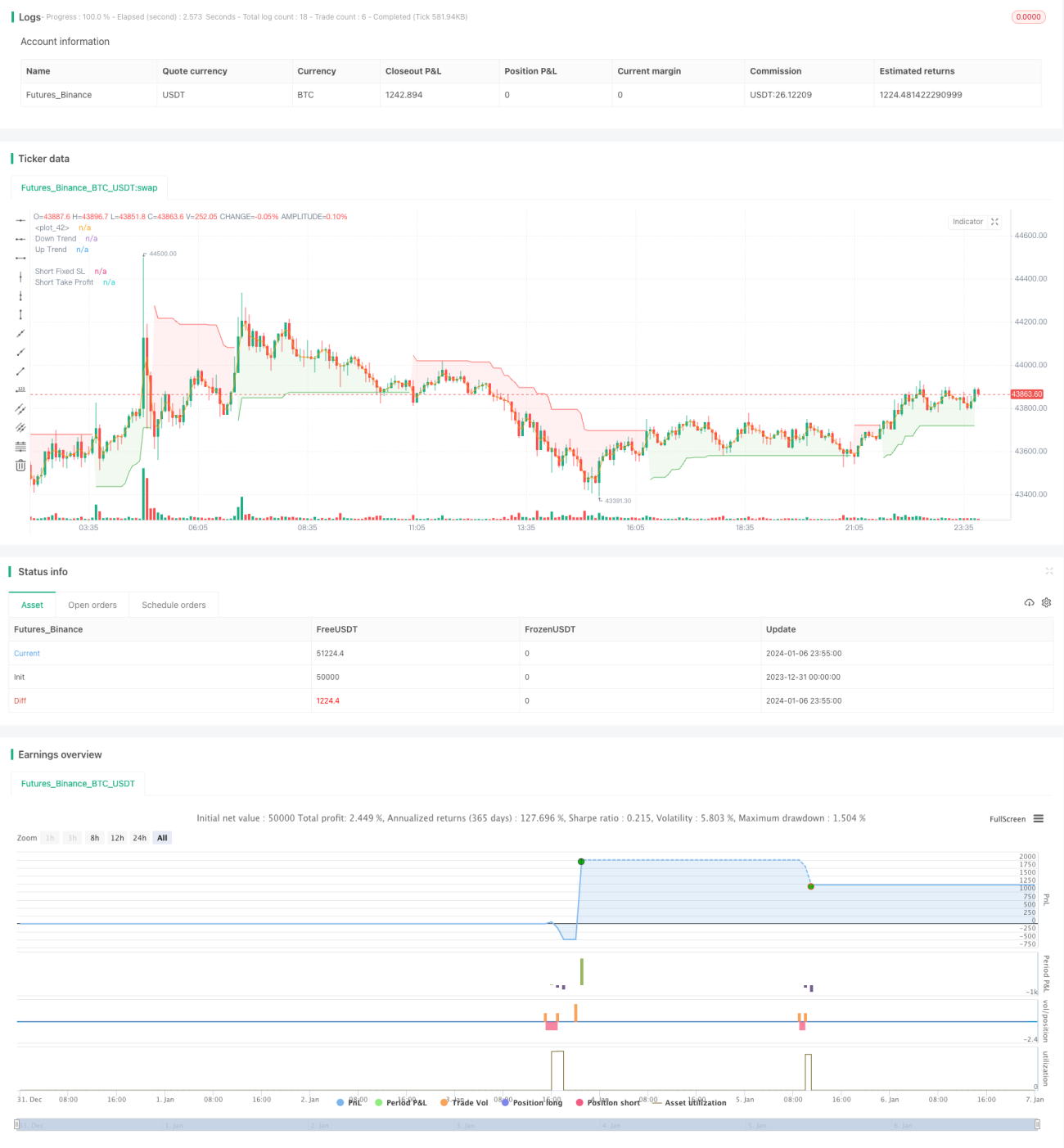

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1