Estratégia de negociação multi-timeframe baseada em RSI e média móvel

Visão Geral

Esta estratégia combina o indicador estocástico RSI, a média móvel simples (SMA) e a média móvel ponderada (WMA) para gerar sinais de compra e venda. Ela avalia a direção da tendência simultaneamente nos quadros temporais de 5 minutos e 1 hora. Em uma tendência estabilizada, quando a linha rápida do RSI cruza para cima ou para baixo a linha lenta, um sinal de negociação é gerado.

Princípio da Estratégia

A estratégia calcula primeiro a média móvel ponderada (WMA) de 144 períodos e a média móvel simples (SMA) de 5 períodos nos dois prazos (1 hora e 5 minutos). Somente quando a SMA de 5 minutos está acima da WMA, considera-se que o mercado está em alta. Em seguida, a estratégia calcula os indicadores de direção do RSI, bem como as linhas K e D correspondentes. Quando a linha K cruza abaixo da linha D vinda de uma região de sobrecompra, gera-se um sinal de venda; quando a linha K cruza acima da linha D vinda de uma região de sobrevenda, gera-se um sinal de compra.

Análise de Vantagens

Esta é uma estratégia de acompanhamento de tendência muito eficaz. Ao combinar dois prazos para julgar a tendência, reduz significativamente os sinais falsos. Além disso, ela utiliza múltiplos indicadores para filtragem, incluindo RSI, SMA e WMA, tornando os sinais mais confiáveis. Ao impulsionar o KDJ pelo RSI, ela também modifica o problema de sinais falsos comuns na estratégia KDJ convencional. Além disso, a estratégia possui configurações de stop loss e take profit para bloquear lucros, controlando efetivamente o risco.

Análise de Riscos

O maior risco desta estratégia reside no erro de julgamento de tendência. Em pontos de reversão do mercado, as médias de curto e longo prazo podem se cruzar simultaneamente para cima ou para baixo, gerando sinais falsos. Além disso, em mercados laterais, o RSI pode produzir vários sinais de negociação confusos. No entanto, esses riscos podem ser mitigados ajustando adequadamente os períodos da SMA, WMA e os parâmetros do RSI.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

- Testar diferentes comprimentos de SMA, WMA e RSI para encontrar a melhor combinação de parâmetros.

- Adicionar outros indicadores, como MACD, Bandas de Bollinger, etc., para verificar a confiabilidade dos sinais.

- Otimizar as estratégias de stop loss e take profit, testando stop loss percentual fixo, stop loss por deslizamento de saldo, stop loss móvel, entre outros.

- Incorporar um módulo de gerenciamento de capital para controlar o tamanho de cada operação e a exposição total ao risco.

- Adicionar algoritmos de aprendizado de máquina para encontrar parâmetros com melhor desempenho por meio de backtesting extenso.

Resumo

Esta estratégia aproveita plenamente as vantagens das médias móveis e do indicador estocástico, estabelecendo um sistema de acompanhamento de tendência relativamente confiável. Através da verificação em múltiplos prazos e indicadores, ela consegue capturar com sucesso a direção das tendências de médio e longo prazo. Simultaneamente, as configurações de stop loss e take profit permitem que ela suporte certo grau de oscilação do mercado. No entanto, ainda há espaço para melhorias, como testar a combinação com mais indicadores e introduzir métodos de aprendizado de máquina para encontrar parâmetros ótimos. No geral, é uma estratégia de negociação muito promissora.

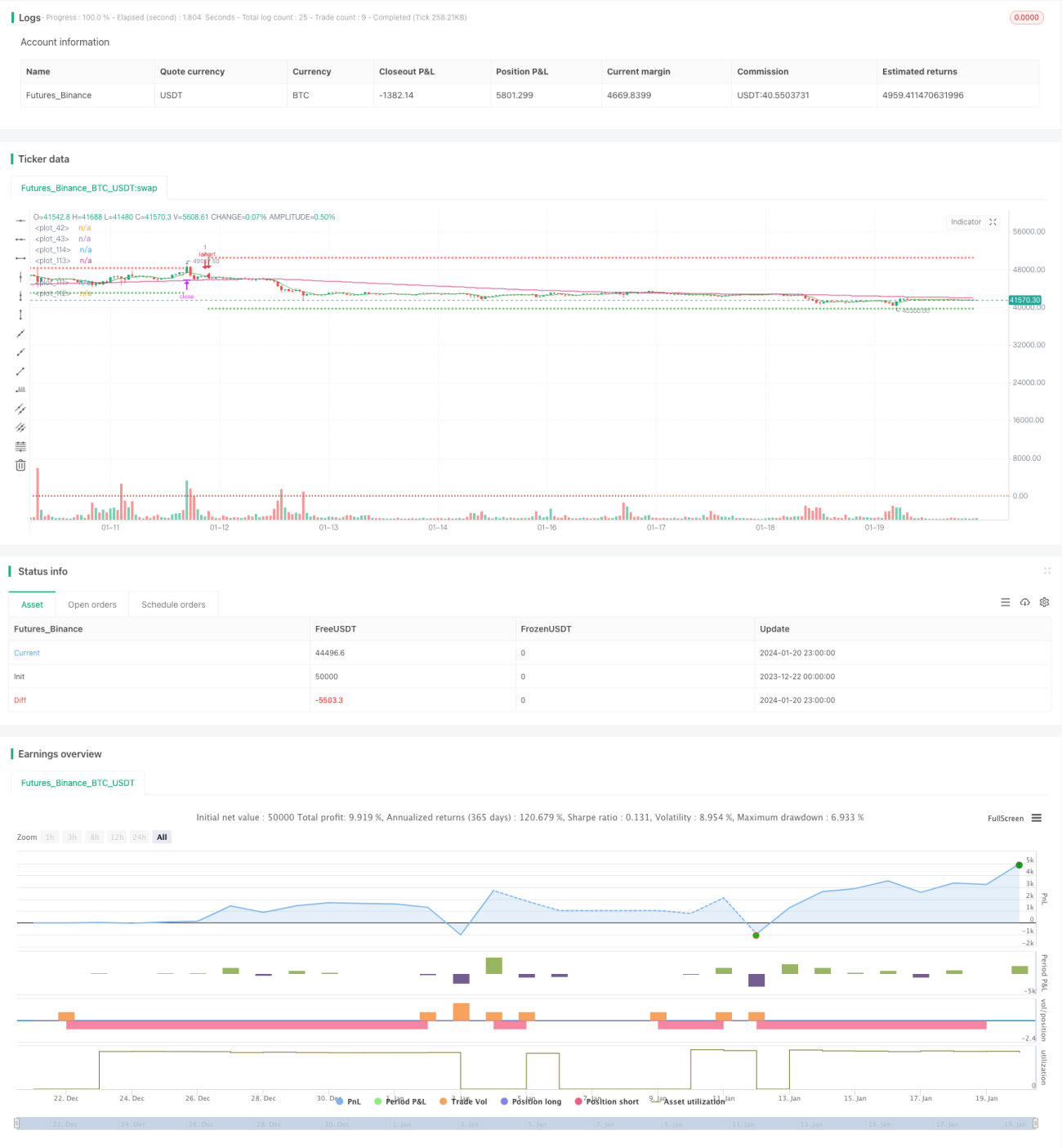

/*backtest

start: 2023-12-22 00:00:00

end: 2024-01-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © bufirolas

// Works well with a wide stop with 20 bars lookback- 1