Estratégia de Formador de Mercado com Limites nas Bandas de Bollinger

Visão Geral

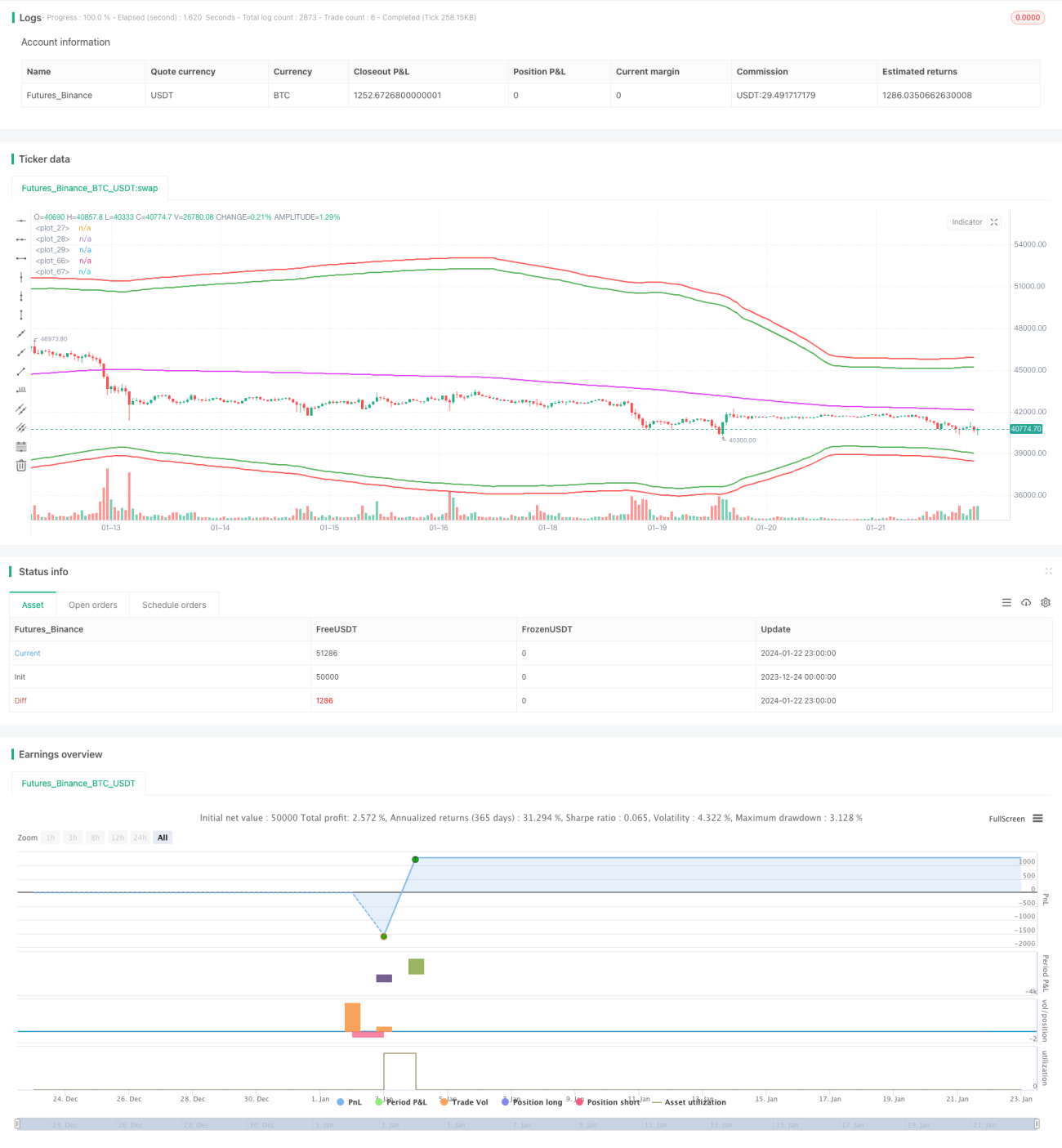

Esta estratégia é uma estratégia de market maker que utiliza Bandas de Bollinger para entradas, uma média móvel para fechamento e um percentual simples de stop loss. Ela obteve lucros extremamente elevados no contrato XTBTUSD em junho de 2022.

Princípio da Estratégia

A estratégia utiliza as bandas superior e inferior de Bollinger como zonas de oportunidade para abertura de posições. Especificamente, quando o preço está abaixo da banda inferior, abre-se uma posição comprada; quando o preço está acima da banda superior, abre-se uma posição vendida.

Além disso, a estratégia também utiliza uma média móvel como referência para o fechamento das posições. Quando se está em uma posição comprada, se o preço estiver acima da média móvel, opta-se por fechar a posição; da mesma forma, quando se está em uma posição vendida, se o preço estiver abaixo da média móvel, também se fecha a posição.

Para o stop loss, a estratégia utiliza um método de stop loss contínuo simples, baseado no preço de entrada multiplicado por um percentual fixo. Isso pode efetivamente evitar perdas enormes em movimentos unidirecionais do mercado.

Análise de Vantagens

As principais vantagens desta estratégia são as seguintes:

- O uso das Bandas de Bollinger pode capturar efetivamente a volatilidade dos preços, obtendo mais oportunidades de negociação quando a volatilidade aumenta.

- A estratégia de market maker pode obter receitas de taxas de ambos os lados (compra e venda) por meio de negociações bidirecionais.

- O stop loss percentual permite controlar o risco ativamente, evitando perdas excessivas em movimentos unidirecionais.

Análise de Riscos

Esta estratégia também apresenta alguns riscos:

- As Bandas de Bollinger nem sempre são um indicador confiável de entrada, podendo gerar sinais falsos.

- A estratégia de market maker pode facilmente ficar presa em mercados laterais (sem tendência definida).

- O stop loss percentual pode ser muito arbitrário, não conseguindo se adaptar a movimentos complexos do mercado.

Para mitigar esses riscos, podemos considerar combinar outros indicadores para filtrar sinais, otimizar a configuração do stop loss ou limitar adequadamente o tamanho das posições.

Direções de Otimização

A estratégia ainda possui espaço para otimização adicional:

- Testar diferentes combinações de parâmetros para encontrar os parâmetros ideais.

- Adicionar mais indicadores de filtro para validação multifatorial.

- Utilizar métodos de aprendizado de máquina para otimizar automaticamente os parâmetros.

- Considerar o uso de métodos de stop loss mais refinados, como o stop loss parabólico.

Resumo

No geral, esta estratégia é uma estratégia de market maker de alta frequência altamente lucrativa. Ela utiliza as Bandas de Bollinger para gerar oportunidades de negociação, ao mesmo tempo que controla o risco. No entanto, também precisamos estar cientes de seus problemas e limitações, e validá-la com cautela em negociações reais. Com otimizações adicionais, a estratégia tem potencial para gerar retornos extraordinários ainda mais estáveis.

- 1