Estratégia de Rastreamento de Momentum com Filtro de Faixa Adaptativa Bidirecional

1

Follow

1802

Followers

Visão Geral

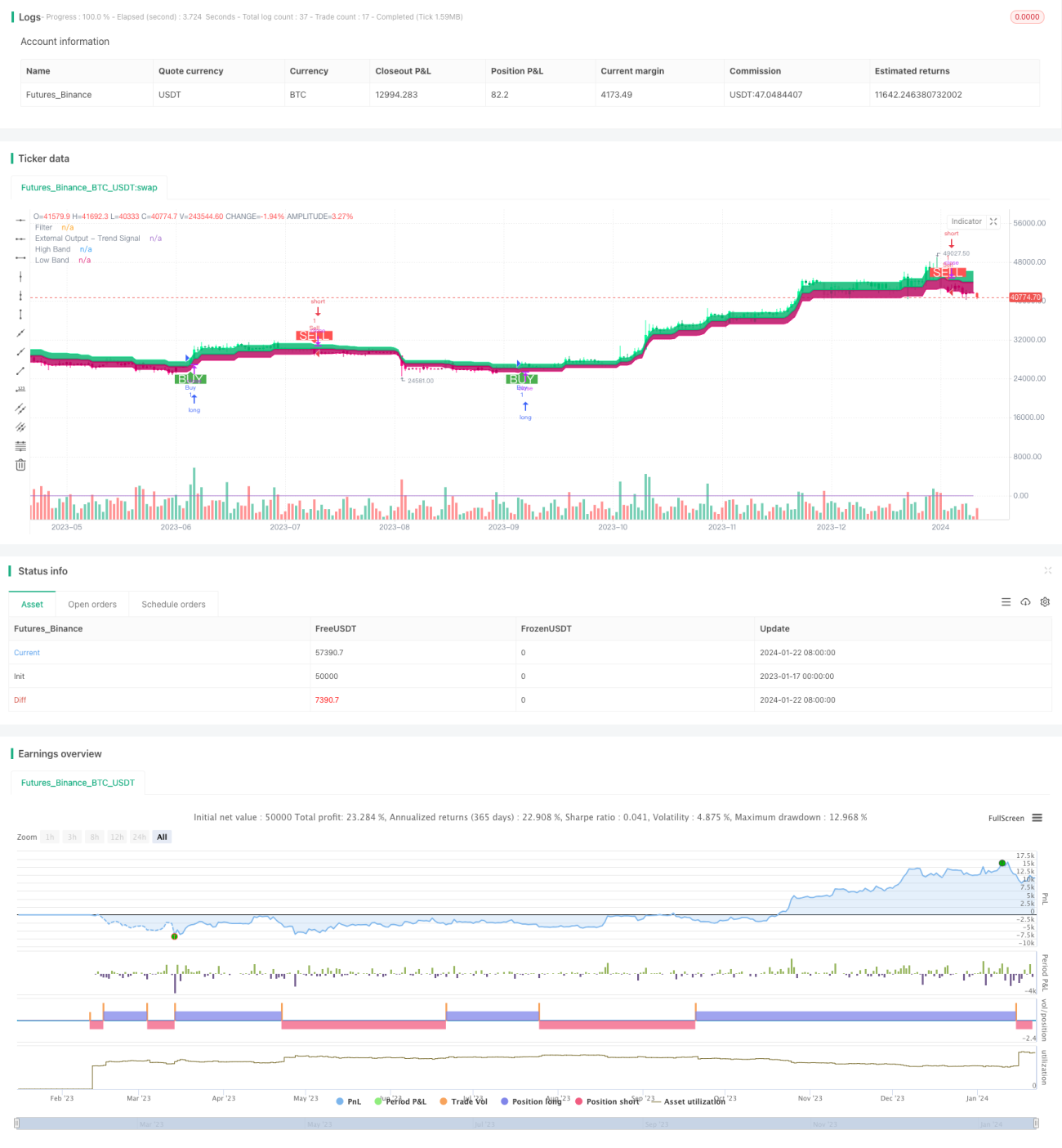

Esta estratégia é uma estratégia de rastreamento de momentum com filtro de alcance adaptativo bidirecional. Ela utiliza um filtro de alcance adaptativo para rastrear as flutuações de preço e, combinada com indicadores de volume, determina a direção de valor, realizando compras em baixa e vendas em alta.

Princípio da Estratégia

- Utiliza um filtro de alcance adaptativo para rastrear as flutuações de preço. O tamanho do filtro é ajustado adaptativamente com base no período, quantidade e escala definidos pelo usuário.

- O filtro é dividido em dois tipos: Tipo 1 e Tipo 2. O Tipo 1 é o padrão de rastreamento de alcance, enquanto o Tipo 2 é do tipo de arredondamento escalonado.

- A direção da flutuação de preço é determinada pela relação entre o filtro e o preço de fechamento. Preço acima da banda superior indica alta, e abaixo da banda inferior indica baixa.

- Combinando a variação do preço de fechamento em relação ao dia anterior, determina-se a direção de valor. Valor em alta indica posição comprada, e valor em baixa indica posição vendida.

- Quando o preço rompe a banda superior e o valor está em alta, é gerado um sinal de compra; quando o preço rompe a banda inferior e o valor está em baixa, é gerado um sinal de venda.

Análise de Vantagens

- O filtro de alcance adaptativo pode capturar com precisão as flutuações do mercado.

- Os dois tipos de filtro atendem diferentes preferências de negociação.

- Combinado com indicadores de volume, pode identificar efetivamente a direção de valor.

- A estratégia é flexível, permitindo ajustar parâmetros conforme o mercado.

- É possível customizar e selecionar a lógica de condições de negociação adequada.

Análise de Riscos

- Configurações inadequadas de parâmetros podem levar a excesso de negociações ou ordens perdidas.

- Os sinais de rompimento apresentam certo atraso.

- Os indicadores de volume podem ter certo risco de travamento.

- O rompimento de alcance pode facilmente levar a armadilhas.

Prevenção de riscos:

- Selecionar combinações adequadas de parâmetros e ajustá-las oportunamente.

- Combinar com outros indicadores para identificar tendências.

- Negociar com cautela próximo a níveis chave e em reversões de tendência.

Direções de Otimização

- Testar diferentes combinações de tamanho de alcance e período de suavização para encontrar a melhor combinação.

- Experimentar diferentes tipos de filtro e escolher o de preferência pessoal.

- Testar outros indicadores de volume ou indicadores técnicos auxiliares.

- Otimizar e ajustar a lógica das condições de negociação para reduzir negociações irracionais.

- Combinar com a teoria de fractal de mercado para definir proporções de rebalanceamento adaptativas.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1