Estratégia de reversão de tendência com três candles

Visão Geral

A Estratégia de Reversão de Tendência com Três Velas (Three Candle Reversal Trend Strategy) é uma estratégia de negociação de curto prazo que identifica três velas consecutivas de alta ou de baixa, seguidas por uma vela engulfing, para determinar a reversão da tendência de curto prazo. Ela combina diversos indicadores técnicos para filtrar os pontos de entrada. A estratégia utiliza uma relação risco-retorno de 1:3, favorecendo a obtenção de retornos excessivos.

Princípio da Estratégia

A lógica central da estratégia é identificar um padrão de três velas consecutivas de alta ou de baixa, que geralmente sinaliza uma reversão da tendência de curto prazo. Quando três velas de baixa são detectadas, aguarda-se a próxima vela de alta engulfing para entrar comprado; inversamente, quando três velas de alta são detectadas, aguarda-se a próxima vela de baixa engulfing para entrar vendido. Isso permite capturar oportunidades de reversão de tendência de curto prazo.

Além disso, a estratégia incorpora diversos indicadores técnicos para filtrar as entradas. Utiliza duas médias móveis SMA com parâmetros diferentes, considerando a entrada apenas quando a média rápida cruza acima da média lenta. Também usa um indicador de regressão linear para avaliar se o mercado está em tendência ou lateralizado; as negociações são realizadas apenas em condições de tendência. A estratégia oferece ainda um interruptor para optar por combinar o padrão de velas com um cruzamento de ouro das médias móveis para entrar. Com essa filtragem combinada, a maior parte do ruído é eliminada, aumentando a precisão das entradas.

Na definição de stop loss e take profit, a estratégia exige uma relação risco-retorno mínima de 1:3. O ATR das últimas N velas é calculado e, combinado com uma porcentagem da amplitude, ajusta-se o nível de stop loss, permitindo então definir o nível de take profit. Isso possibilita obter retornos excessivos adequados assumindo um risco controlado.

Vantagens da Estratégia

A Estratégia de Reversão de Tendência com Três Velas apresenta as seguintes vantagens:

- Identifica pontos de reversão de tendência de curto prazo, capturando oportunidades oportunamente.

- Múltiplos indicadores filtram as entradas, aumentando a precisão.

- Mecanismo de stop loss e take profit é razoável, com relação risco-retorno equilibrada.

- Parâmetros simples, fáceis de entender e operar.

Riscos da Estratégia

A estratégia também apresenta alguns riscos que devem ser observados:

- Reversões de curto prazo nem sempre representam reversões de longo prazo; é necessário considerar tendências de timeframes maiores. Pode-se adicionar médias móveis de período mais longo como filtro.

- Sinais baseados apenas no padrão de velas podem ser falsos; pode-se incluir outros sinais auxiliares.

- A definição do stop loss pode ser otimista demais; é possível ajustá-lo para um intervalo mais estreito.

- Dados insuficientes de backtest; o desempenho em tempo real apresenta certa incerteza.

Direções de Otimização

A estratégia pode ser otimizada nas seguintes direções:

- Ajustar os parâmetros das médias móveis e da regressão linear para melhorar a identificação da tendência.

- Adicionar outros indicadores auxiliares, como o Stochastics, para melhorar a precisão dos sinais.

- Otimizar os parâmetros do ATR e a amplitude do stop loss para equilibrar risco e retorno.

- Implementar um mecanismo de trailing stop para aumentar o potencial de lucro.

- Desenvolver uma gestão de capital mais rigorosa para controlar o risco de negociação.

Resumo

Em resumo, a Estratégia de Reversão de Tendência com Três Velas é uma estratégia de negociação de curto prazo que combina padrões de preços simples com múltiplos indicadores auxiliares, construída sobre um equilíbrio adequado entre risco e retorno. Com baixa complexidade, ela oferece um bom desempenho, merecendo atenção e testes por parte dos investidores. Há também espaço para melhorias. Através da otimização de parâmetros e do acréscimo de regras, ela pode evoluir para uma estratégia de negociação quantitativa estável e eficiente.

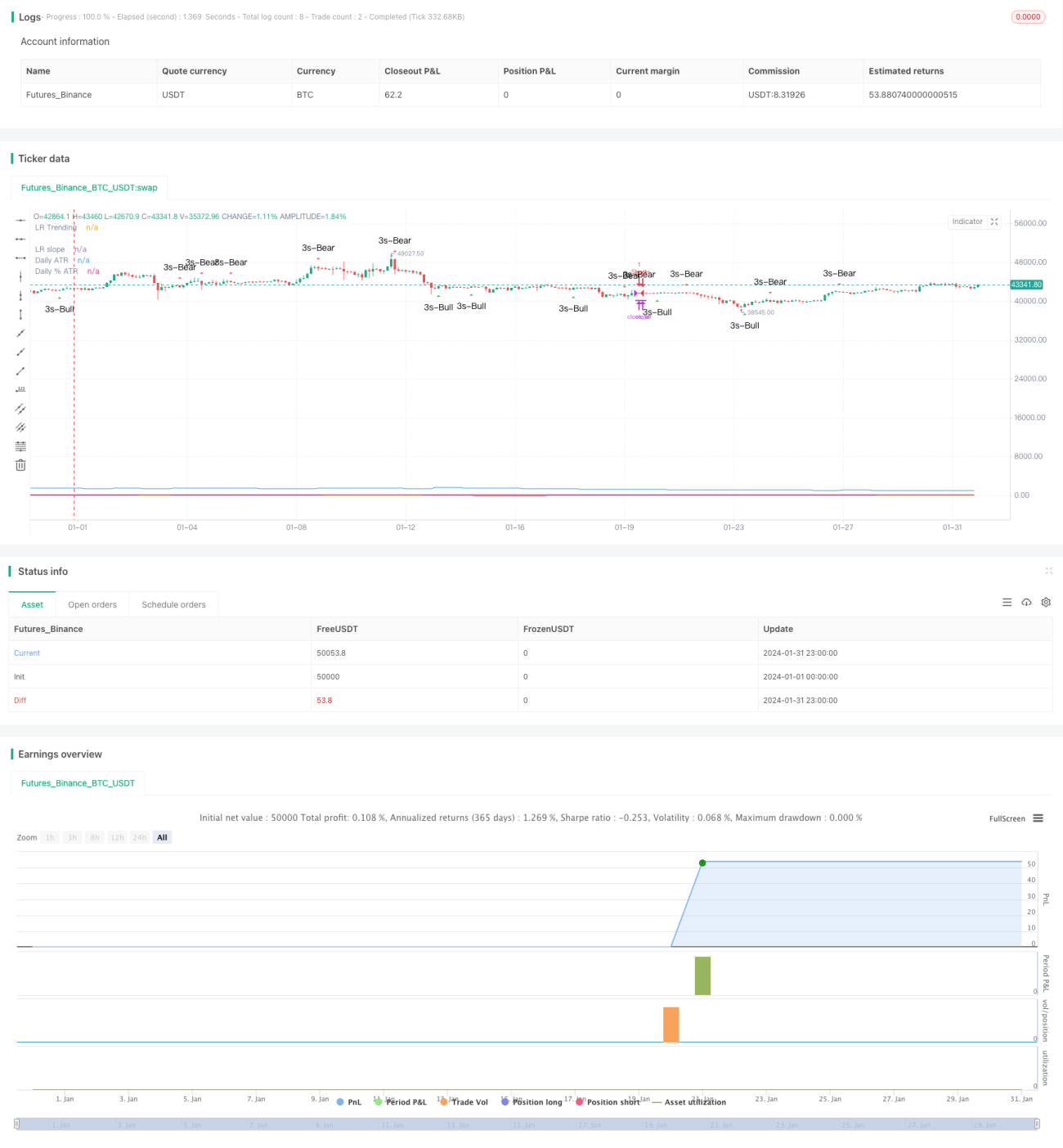

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © platsn

//

// Mainly developed for SPY trading on 1 min chart. But feel free to try on other tickers.- 1