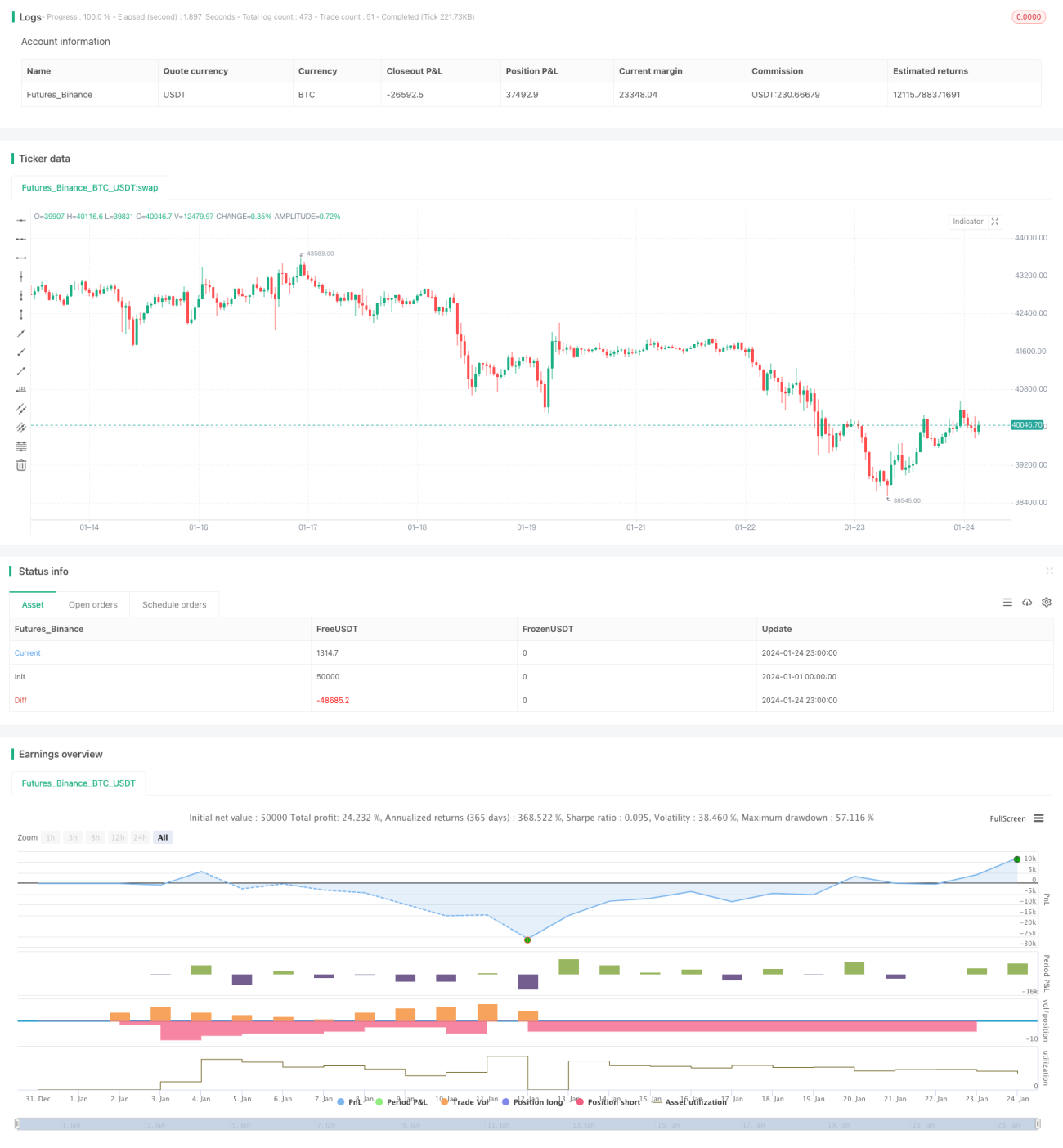

Estratégia de Grid Trading Adaptativa baseada em Plataforma de Negociação Quantitativa

Visão Geral

Esta estratégia é uma estratégia de trading em grade adaptativa baseada em uma plataforma de trading quantitativo. A estratégia define intervalos de grade automáticos ou manuais, colocando ordens de compra e venda em intervalos iguais dentro do intervalo, realizando trading em grade. Quando o preço ultrapassa os limites superior e inferior da grade, a estratégia ajusta automaticamente o intervalo da grade.

Princípio da Estratégia

-

Definir os preços limite superior e inferior da grade. É possível calcular automaticamente os preços mais altos e mais baixos do histórico de preços dentro de um determinado período como limites, ou definir manualmente preços fixos.

-

Calcular o espaçamento de preços de cada grade com base nos preços limite e no número de grades.

-

Entre os preços limite superior e inferior, dispor vários pontos de compra e venda em intervalos iguais como grade.

-

Quando o preço de mercado ultrapassa o limite inferior da grade, colocar uma ordem de compra na próxima grade após a grade da ordem aberta mais recente; quando o preço ultrapassa o limite superior, colocar uma ordem de venda na grade anterior à grade da ordem aberta mais recente.

-

Dessa forma, operações de compra e venda são realizadas continuamente entre os limites superior e inferior da grade. Quando a tendência de preços se inverte, as ordens anteriores são gradativamente encerradas com lucro ou prejuízo.

Vantagens da Estratégia

-

O trading em grade pode lucrar em mercados laterais e de oscilação.

-

O ajuste adaptativo do intervalo da grade pode ser feito automaticamente conforme a volatilidade do mercado, sem intervenção manual.

-

É possível pré-definir o montante de capital investido, alocando proporcionalmente em cada grade para controlar o risco de cada ordem.

-

Lógica simples, fácil de entender, com parâmetros flexíveis para ajuste.

Riscos e Contramedidas

-

Perdas causadas pela quebra dos limites superior e inferior

- Solução: definir posições de stop loss razoáveis.

-

Perdas repetidas em mercados de tendência

- Solução: identificar tendências e pausar o trading oportunamente.

-

Definição inadequada de parâmetros

- Solução: ajustar o número de grades e o espaçamento de preços.

Direções de Otimização

-

Utilizar aprendizado de máquina para prever a faixa de volatilidade e tendência dos preços, ajustando dinamicamente os parâmetros da grade.

-

Em mercados de tendência, mudar para trading de tendência para evitar perdas no trading em grade.

-

Combinar indicadores como taxa de utilização de capital e taxa de retorno para controle de risco.

-

Expandir para múltiplos ativos, ampliando a aplicação de capital.

Resumo

Esta estratégia é uma estratégia de grade adaptativa com parâmetros ajustáveis automaticamente, adequada para ações, criptomoedas e moedas estrangeiras em mercados laterais e de oscilação. Com o ajuste dos parâmetros, pode se adaptar a diferentes condições de mercado, possuindo certo valor prático.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-24 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//hk4jerry

strategy("Grid Bot Backtesting", overlay=false, pyramiding=3000, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.025)- 1