Стратегия разворотной торговли на основе обобщенной поддержки/сопротивления

Обзор

Данная стратегия основана на контртрендовой торговле с использованием фактора длинных/коротких позиций и установкой целевых точек получения прибыли. Основой фактора лонг/шорт является расширенная форма поддержки/сопротивления, основанная на объеме торгов, что подходит для инструментов с высоким объемом и волатильностью. Преимущество стратегии заключается в возможности улавливать значительные среднесрочные и краткосрочные развороты тренда и быстро получать прибыль, однако существует риск попадания в ловушку.

Принцип стратегии

-

Идентификация фактора лонг/шорт на основе «обобщенной поддержки/сопротивления» по объему

- Использование свечных паттернов для выявления классических уровней поддержки/сопротивления, фильтрация ложных пробоев по большому объему.

- Обобщенная поддержка/сопротивление обладает лучшей охватывающей способностью по сравнению с классическими паттернами.

- Пробой обобщенной поддержки — сигнал бычьего фактора, пробой обобщенного сопротивления — сигнал медвежьего фактора.

-

Контртрендовая торговля

- После появления сигнала фактора выполняется операция в противоположном направлении.

- При наличии открытой позиции производится частичное закрытие или открытие позиции в противоположную сторону.

-

Установка целей прибыли

- Стоп-лосс на основе ATR.

- Установка нескольких целевых уровней прибыли: 1R/2R/3R и т.д.

- Частичное закрытие позиций при достижении разных целей.

Анализ преимуществ

-

Возможность улавливать значительные среднесрочные и краткосрочные развороты.

Пробой уровней поддержки/сопротивления является достаточно надежным сигналом сильного разворота тренда, позволяя фиксировать значительные по величине развороты на средних и кратких интервалах. -

Быстрая фиксация прибыли и малая просадка.

Благодаря стоп-лоссу и многоуровневым целям прибыли можно быстро получить прибыль и ограничить просадку по отдельным активам. -

Подходит для инструментов с большим объемом институциональных средств и высокой волатильностью.

Стратегия опирается на объемные показатели, требует достаточного притока институциональных средств для поддержки тренда, а также определенного пространства для колебаний цены для реализации прибыли.

Анализ рисков

-

Риск попадания в ловушку при боковом движении.

При флэте операции по выходу по стопу и входу в обратную сторону могут привести к частым попаданиям в ловушку. -

Риск неэффективности поддержки/сопротивления.

Обобщенные уровни поддержки/сопротивления не являются абсолютно надежными, существует вероятность неудачного тестирования и разворота. -

Риск однонаправленной позиции.

Стратегия является чисто контртрендовой и не учитывает трендовое следование, что может привести к упущению крупных направленных движений. -

Управление рисками:

- Возможно ослабить условия для контртрендовых сделок, не обязательно разворачиваться при каждом пробое.

- Можно комбинировать с другими индикаторами для фильтрации, например, с дивергенцией цены и объема.

- Оптимизировать стратегию стоп-лосса, чтобы снизить вероятность попадания в ловушку.

Направления оптимизации

-

Оптимизация параметров периода.

Оптимизировать параметры обобщенной поддержки/сопротивления для выявления более надежных факторов. -

Оптимизация стратегии взятия прибыли.

Можно добавить больше уровней целей или использовать нефиксированные цели. -

Оптимизация стратегии стоп-лосса.

Изменить параметры ATR или использовать интеллектуальный стоп-лосс, чтобы уменьшить излишние торговые издержки от резких стопов. -

Комбинирование с трендом и другими факторами.

Ввести скользящие средние для оценки тренда, чтобы избегать сильного противоборства с трендом, или добавить другие вспомогательные факторы.

Заключение

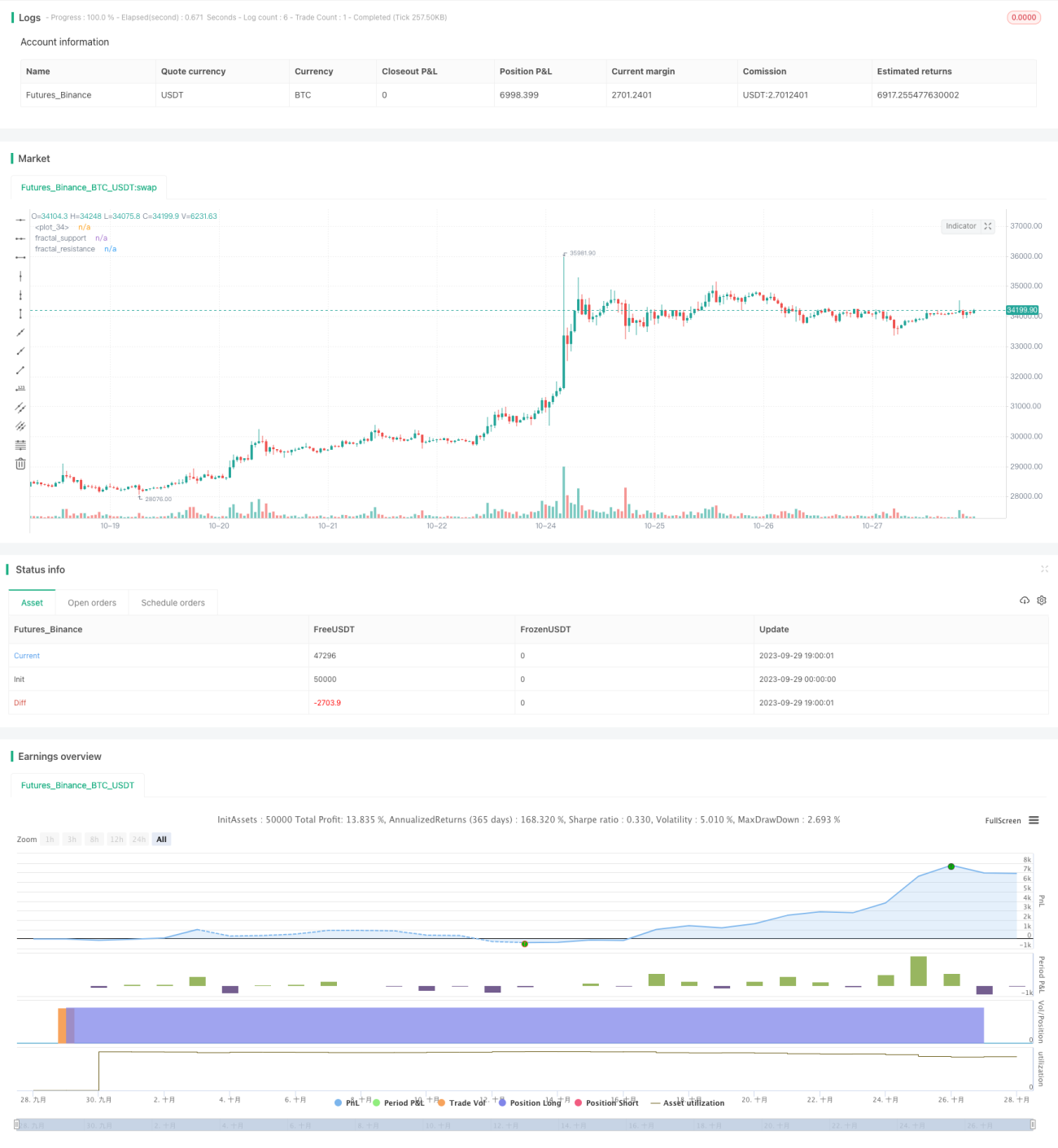

Основная идея стратегии заключается в использовании контртрендовой торговли для улавливания значительных колебаний среднесрочного и краткосрочного характера. Стратегия проста и прямолинейна, настройка параметров позволяет добиться неплохих результатов на реальном рынке. Однако контртрендовый подход довольно агрессивен, сопряжен с определенной просадкой и риском попадания в ловушку, поэтому требуется дальнейшая оптимизация стоп-лосса и стратегии получения прибыли, а также разумное сочетание с определением тренда для снижения ненужных потерь.

- 1