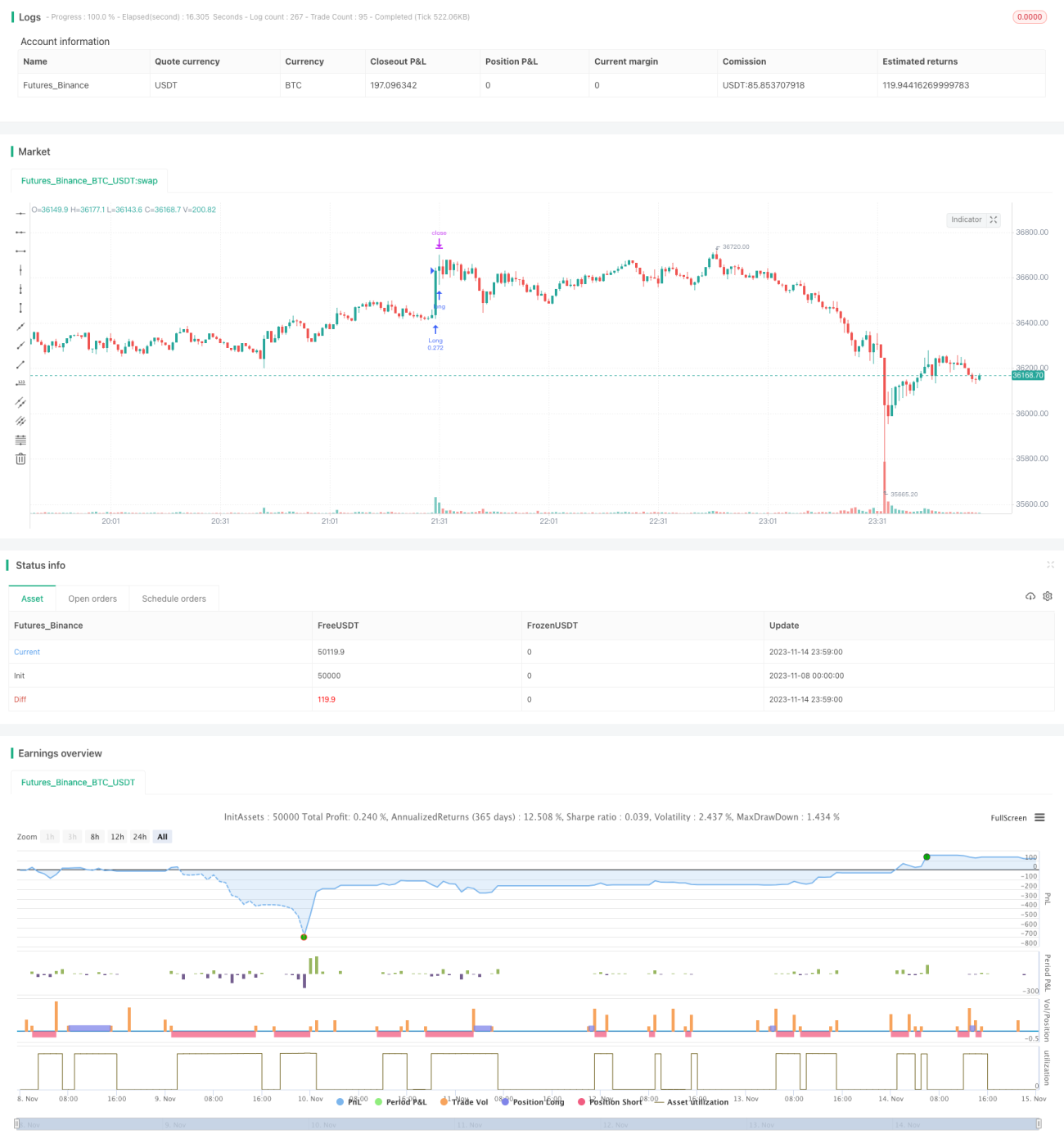

Мультитрендовая стратегия

Обзор

Данная стратегия комплексно использует несколько индикаторов для определения направления тренда, применяя метод следования за трендом для捕捉 среднесрочных и краткосрочных трендовых возможностей. Стратегия специально разработана для следования за трендом, чтобы увеличить процент успешных сделок и снизить просадки.

Принцип стратегии

- Используется индикатор WVAP для оценки ценового соотношения;

- Индикатор RSI определяет импульс быков и медведей;

- Индикатор QQE выявляет ценовые прорывы;

- Индикатор ADX оценивает силу тренда;

- Coral Trend Indicator определяет фундаментальный тренд;

- Индикатор LSMA вспомогательно определяет тренд;

- Комбинация сигналов нескольких индикаторов формирует торговые сигналы.

Стратегия в основном полагается на такие индикаторы, как RSI, QQE, ADX, для определения направления и силы тренда, а кривая Coral Trend Indicator используется как критерий фундаментального тренда. Когда такие индикаторы, как RSI, подают сигнал на покупку, и Coral Trend Indicator также показывает восходящую кривую, это с высокой вероятностью соответствует восходящему тренду, и стратегия выбирает покупку. Индикаторы, такие как WVAP, в основном используются для оценки разумности цены, чтобы избежать покупки на вершине.

Преимущества стратегии

- Комбинация нескольких индикаторов повышает точность判断;

- Акцент на следование за трендом увеличивает вероятность прибыли;

- Использование подхода прорывов, отсеивание рынков с торговым диапазоном;

- Включение фундаментальных индикаторов позволяет избежать торговли против тренда;

- Разумные настройки времени торговли и размера позиции снижают риски;

- Чёткая логика стратегии, легко понять и оптимизировать.

Главное преимущество стратегии — комбинация нескольких индикаторов, что в определённой степени снижает вероятность ошибок одного индикатора и повышает точность判断. Одновременно акцент на следование за трендом и подход прорывов помогает отбирать надёжные среднесрочные и краткосрочные возможности. Кроме того, включение фундаментальных индикаторов позволяет избежать операций против тренда. Все эти конструктивные особенности повышают стабильность стратегии и вероятность получения прибыли.

Риски стратегии

- Запаздывание в определении направления тренда может привести к пропуску оптимального момента входа;

- Контроль просадок несовершенен, существует риск значительных просадок;

- При развороте фундаментальных факторов стратегия может пропустить сигналы;

- Не учитываются торговые издержки, на практике доходность может снизиться.

Наибольший риск стратегии заключается в возможном запаздывании комбинации нескольких индикаторов, что приводит к пропуску наилучшего момента входа и снижает потенциал прибыли. Кроме того, контроль просадок неидеален, есть риск больших просадок. Когда фундаментальные условия рынка меняются, а индикаторы ещё не отразили это, легко возникают убытки. На практике торговые издержки также окажут определённое влияние на доходность.

Направления оптимизации стратегии

- Добавление стратегии стоп-лосса для оптимизации контроля просадок;

- Оптимизация настроек параметров для сокращения задержек индикаторов;

- Увеличение применения фундаментальных индикаторов для повышения точности;

- Интеграция алгоритмов машинного обучения для динамической оптимизации параметров.

Основной фокус оптимизации стратегии должен быть направлен на контроль просадок: можно добавить скользящий стоп-лосс для фиксации прибыли и снижения просадок. Также можно оптимизировать настройки параметров, сократить задержки индикаторов и повысить чувствительность стратегии к изменениям рынка. Кроме того, можно добавить дополнительные фундаментальные индикаторы для повышения точности. Если удастся применить методы машинного обучения для динамической оптимизации параметров, это также значительно повысит стабильность стратегии.

Заключение

Данная стратегия комплексно использует несколько индикаторов для определения направления тренда, разработана на основе подхода следования за трендом, направлена на повышение точности判断 и увеличение вероятности прибыли. Стратегия имеет преимущества в виде комбинации индикаторов, акцента на следование за трендом и включения фундаментальных факторов, но также существуют проблемы, такие как запаздывание ошибок и недостаточный контроль просадок. В будущем её можно улучшить путём оптимизации настроек параметров, совершенствования стратегии стоп-лосса, добавления фундаментальных индикаторов и другими способами, чтобы добиться лучших результатов при практическом применении.

- 1