Стратегия захвата динамической амплитуды на основе RSI и полос Боллинджера

Обзор

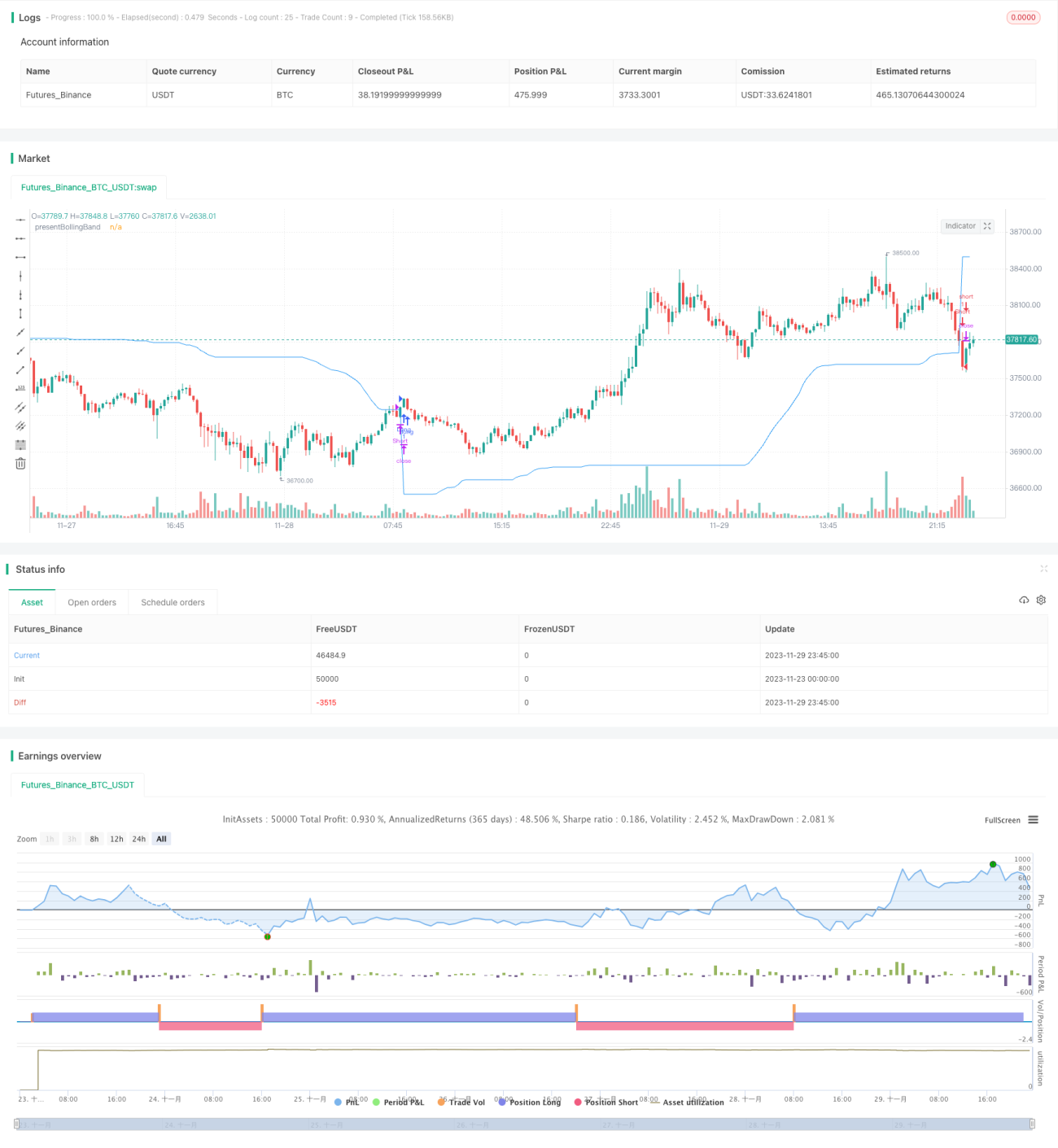

Стратегия захвата динамической волатильности с RSI и полосами Боллинджера — это торговая стратегия, объединяющая концепции полос Боллинджера (BB), индекса относительной силы (RSI) и простой скользящей средней (SMA). Уникальность стратегии в том, что она рассчитывает динамический уровень на основе цены закрытия между верхней и нижней полосами. Эта особенность позволяет стратегии адаптироваться к рыночной волатильности и движению цен.

Рынки криптовалют и акций крайне волатильны, поэтому они идеально подходят для стратегий с полосами Боллинджера. RSI помогает выявить состояния перекупленности и перепроданности на этом часто спекулятивном рынке.

Принцип стратегии

Динамические полосы Боллинджера: Стратегия сначала рассчитывает верхнюю и нижнюю полосы Боллинджера на основе заданной длины и множителя. Затем объединяет полосы и цену закрытия для динамической корректировки значения presentBollingBand. Наконец, когда цена пересекает present BollingBand, генерируется сигнал на покупку, а когда цена пересекает present BollingBand — сигнал на продажу.

RSI: Если пользователь выбирает использование RSI для генерации сигналов, стратегия также рассчитывает RSI и его SMA и использует их для создания дополнительных сигналов на покупку и продажу. Сигналы на основе RSI используются только в том случае, если опция «Использовать RSI для генерации сигналов» установлена в true.

Затем стратегия проверяет выбранное направление торговли и соответствующим образом открывает длинную или короткую позицию. Если направление торговли установлено как «В обе стороны», стратегия может открывать как длинные, так и короткие позиции одновременно.

Наконец, когда цена закрытия пересекает present BollingBand, длинная позиция закрывается; когда цена закрытия пересекает present BollingBand, короткая позиция закрывается.

Анализ преимуществ

Стратегия сочетает в себе преимущества полос Боллинджера, RSI и SMA, что позволяет ей адаптироваться к рыночной волатильности, динамически улавливать колебания и генерировать торговые сигналы в условиях перекупленности/перепроданности.

Индикатор RSI дополняет сигналы полос Боллинджера, помогая избежать ложных входов на колеблющемся рынке. Стратегия позволяет выбирать только длинные, только короткие или двусторонние сделки, адаптируясь к различным рыночным условиям.

Параметры настраиваются, что позволяет адаптировать стратегию под индивидуальную толерантность к риску.

Анализ рисков

Стратегия опирается на технические индикаторы и не может справиться с фундаментальными разворотами.

Неправильная настройка параметров полос Боллинджера может приводить к слишком частым или слишком редким торговым сигналам.

Двусторонняя торговля увеличивает риск, необходимо остерегаться убытков при коротких позициях на встречном движении.

Рекомендуется использовать стоп-лосс для контроля риска.

Направления оптимизации

- Комбинировать с другими индикаторами для фильтрации сигналов, например MACD.

- Добавить стратегию стоп-лосса.

- Оптимизировать параметры полос Боллинджера и RSI.

- Настраивать параметры под разные торговые инструменты и таймфреймы.

- Рассмотреть оптимизацию на реальных данных, корректируя параметры под реальные условия.

Заключение

Стратегия захвата динамической волатильности с RSI и полосами Боллинджера — это стратегия на основе технических индикаторов, объединяющая преимущества полос Боллинджера, RSI и SMA. Она динамически корректирует полосы Боллинджера для улавливания рыночной волатильности. Стратегия имеет широкие возможности настройки и оптимизации, но не может предсказать фундаментальные изменения. Рекомендуется протестировать на реальном счете, при необходимости скорректировать параметры или добавить другие индикаторы для снижения риска.

- 1