Продвинутая стратегия SuperTrend

Обзор

Стратегия Advanced SuperTrend представляет собой оптимизированную и улучшенную версию классического индикатора SuperTrend. Она объединяет ценовое действие, волатильность и ряд технических индикаторов, чтобы повысить качество сигналов, уменьшить шум и более точно улавливать изменения рыночных трендов.

Принцип стратегии

Основой стратегии Advanced SuperTrend является линия SuperTrend. Она рассчитывается на основе истинного диапазона (ATR) и ценового импульса и используется для определения потенциальных ценовых трендов и точек разворота. Когда цена находится выше линии SuperTrend, это указывает на восходящий тренд; в противном случае — на нисходящий.

В отличие от традиционного индикатора SuperTrend, который учитывает только цену закрытия и истинный диапазон, расширенная стратегия также включает несколько измерений, таких как объем, осциллятор импульса и фундаментальные данные, для проверки надежности сигналов. Такой многомерный подход позволяет генерировать более точные и надежные торговые сигналы, менее подверженные рыночному шуму.

Анализ преимуществ

Основные преимущества стратегии Advanced SuperTrend:

-

Более точное определение рыночного направления и фильтрация ложных пробоев. Стратегия дожидается согласованности нескольких факторов и индикаторов, прежде чем сгенерировать торговый сигнал, что значительно повышает процент успешных сделок.

-

Снижение влияния рыночного шума. Комбинированное использование фильтров позволяет отсечь множество несущественных рыночных данных, делая анализ более четким.

-

Оптимизация управления рисками. Четкие торговые сигналы помогают трейдерам лучше определять уровни стоп-лосса и тейк-профита, обеспечивая более эффективный контроль рисков.

-

Высокая адаптивность. Помимо определения трендов, стратегию можно комбинировать с другими техническими инструментами для создания комплексной и эффективной торговой системы.

Анализ рисков

Стратегия Advanced SuperTrend также имеет следующие основные риски:

-

Риск настройки параметров. Неправильное сочетание параметров индикаторов может привести к неработоспособности стратегии или генерации избыточных ложных сигналов.

-

Риск ошибочного определения тренда. Ни одна стратегия не может полностью избежать ошибок в определении тренда; неожиданные изменения тренда могут привести к убыткам.

-

Риск переоптимизации. Чрезмерная подгонка параметров под исторические данные делает стратегию слишком зависимой от прошлого и неспособной адаптироваться к изменениям рынка.

-

Риск торговых издержек. При увеличении количества сделок заметно возрастают торговые издержки, такие как комиссии и проскальзывание.

Соответствующие методы решения:

-

Оптимизация настройки параметров, регулярное бэктестирование для проверки их устойчивости.

-

Установка стоп-лосса и тейк-профита для контроля убытков по каждой сделке.

-

Избегать переоптимизации, сохранять обобщающую способность параметров.

-

Рассчитывать соотношение риска и доходности сигналов, контролировать торговые издержки.

Направления оптимизации

Стратегию Advanced SuperTrend можно оптимизировать по следующим направлениям:

-

Настройка параметров в соответствии с различными рынками, чтобы они лучше соответствовали их характеристикам. Например, на волатильных рынках можно сократить период расчета.

-

Добавление механизма адаптивной фильтрации. При входе рынка в определенное состояние автоматически корректировать параметры индикаторов или отключать некоторые фильтры.

-

Исследование методов машинного обучения, например, использование нейронных сетей для динамической оптимизации параметров.

-

Интеграция индикаторов настроения и новостных данных, использование неструктурированной информации для повышения эффективности.

-

Добавление функции масштабирования позиции. При высокой вероятности успеха можно увеличивать объем позиции для получения более высокой прибыли.

Заключение

Стратегия Advanced SuperTrend за счет внедрения множества фильтров и подтверждающих индикаторов оптимизирует и улучшает классический индикатор SuperTrend, что позволяет более точно определять рыночное направление и повышать качество сигналов. По сравнению с одиночным индикатором, данная стратегия предлагает более устойчивое, комплексное и эффективное торговое решение. Однако необходимо учитывать риски неправильной настройки параметров и ошибочного определения тренда, принимая соответствующие меры контроля. При дальнейшей оптимизации и использовании в сочетании с другими инструментами стратегия Advanced SuperTrend обладает большим потенциалом применения.

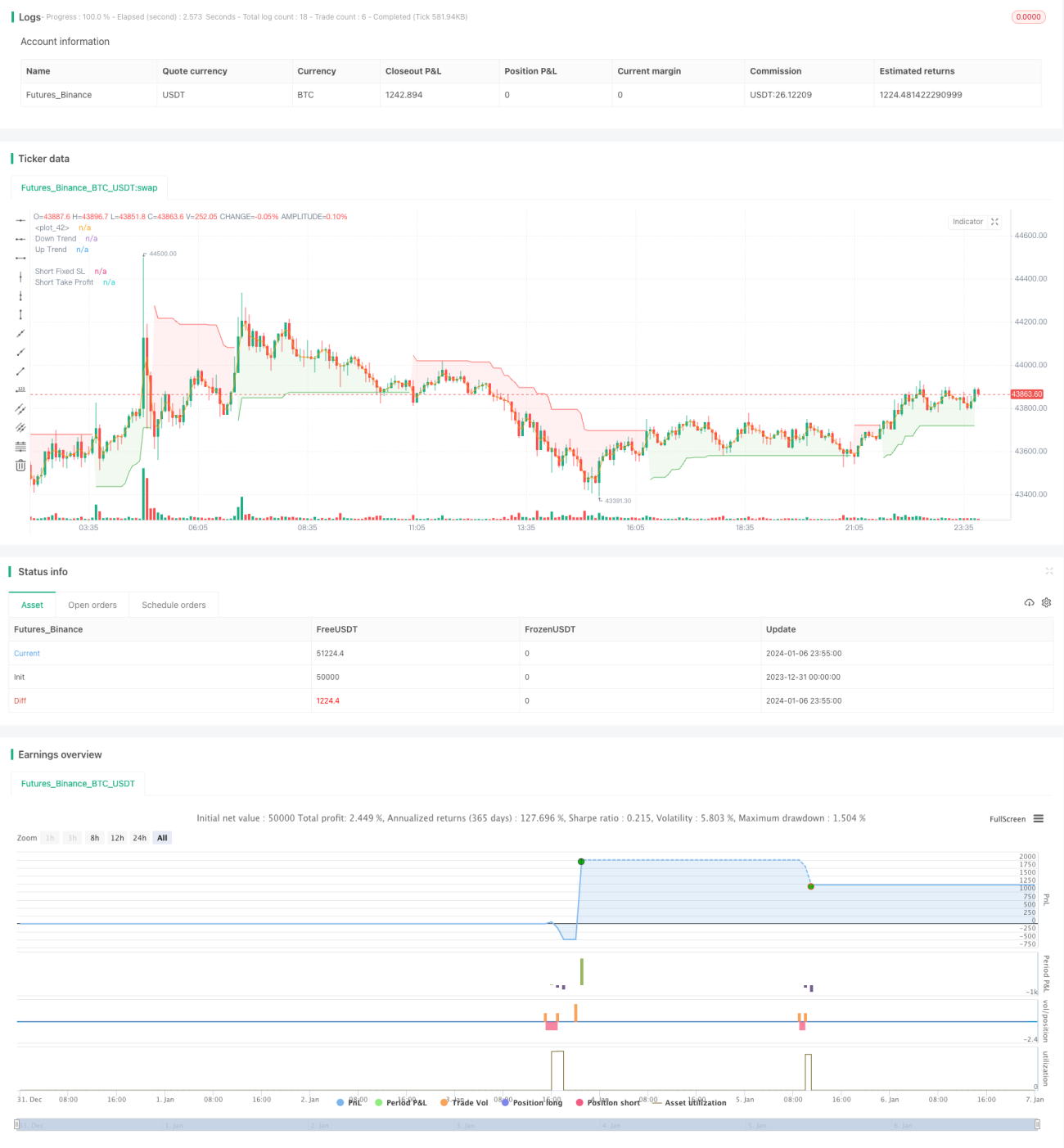

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1