Стратегия разворота тренда по трем свечам

Обзор

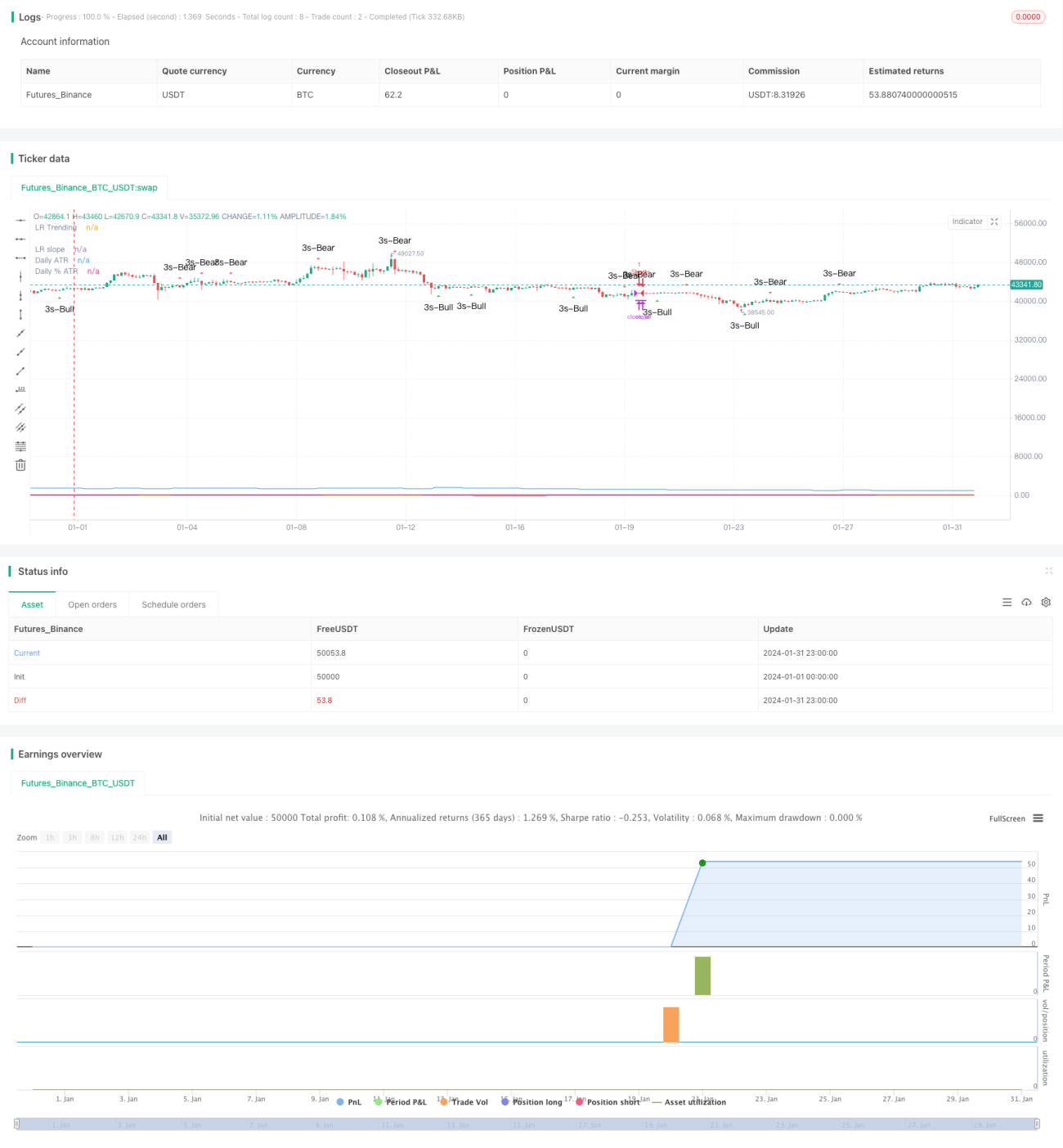

Стратегия разворота тренда на основе трёх свечей (Three Candle Reversal Trend Strategy) представляет собой краткосрочную торговую стратегию. Она идентифицирует три последовательные бычьи или медвежьи свечи, после которых следует поглощающая свеча, чтобы определить разворот краткосрочного тренда, и использует комбинацию нескольких технических индикаторов для фильтрации моментов входа. Стратегия использует соотношение стоп-лосса и тейк-профита 1:3, что способствует получению избыточной доходности.

Принцип стратегии

Основная логика стратегии заключается в распознавании паттерна из трёх последовательных бычьих или медвежьих свечей, который обычно предвещает разворот краткосрочного тренда. При обнаружении трёх медвежьих свечей, когда появляется следующая поглощающая бычья свеча, открывается длинная позиция; и наоборот, при обнаружении трёх бычьих свечей, когда появляется следующая поглощающая медвежья свеча, открывается короткая позиция. Это позволяет своевременно ловить развороты краткосрочного тренда.

Кроме того, стратегия использует несколько технических индикаторов для фильтрации моментов входа. Применяются две скользящие средние (SMA) с разными параметрами, и вход рассматривается только когда быстрая линия пересекает медленную снизу вверх. Также с помощью индикатора линейной регрессии определяется, находится ли рынок в трендовом или боковом состоянии; торговля ведётся только при трендовом состоянии. Стратегия также предоставляет переключатель, позволяющий при необходимости комбинировать «золотое пересечение» скользящих средних с паттерном свечей для входа. Благодаря комплексной оценке этих индикаторов удаётся отсеять большую часть шума и повысить точность входа.

В плане стоп-лосса и тейк-профита стратегия требует, чтобы соотношение риска к прибыли было не менее 1:3. Уровень стоп-лосса устанавливается на основе ATR за последние N свечей в сочетании с процентом волатильности, и затем рассчитывается уровень тейк-профита. Это позволяет получить разумную избыточную доходность при принятии определённого риска.

Преимущества стратегии

Стратегия разворота тренда на основе трёх свечей имеет следующие преимущества:

- Определение точек разворота краткосрочного тренда, своевременное использование возможностей.

- Фильтрация с помощью нескольких индикаторов, повышение точности входа.

- Разумный механизм стоп-лосса и тейк-профита, сбалансированное соотношение риска и доходности.

- Простые настройки параметров, легко понять и применять.

Риски стратегии

Стратегия также несёт некоторые риски, на которые следует обратить внимание:

- Краткосрочный разворот не обязательно означает долгосрочный разворот тренда, необходимо учитывать тренд на более высоком таймфрейме. Можно добавить скользящую среднюю с более длинным периодом в качестве фильтра.

- Сигналы от одного свечного паттерна могут быть ложными, можно рассмотреть добавление других вспомогательных сигналов.

- Установка стоп-лосса может быть слишком оптимистичной, можно немного сузить диапазон стоп-лосса.

- Недостаточность данных бэктестинга, на реальном рынке присутствует определённая неопределённость.

Направления оптимизации стратегии

Стратегию можно оптимизировать по следующим направлениям:

- Настройка параметров скользящих средних и линейной регрессии для улучшения оценки трендового состояния.

- Добавление других вспомогательных индикаторов, таких как стохастик (Stoch), для повышения точности сигналов.

- Оптимизация параметров ATR и процента стоп-лосса для баланса риска и доходности.

- Добавление механизма трейлинга точек пробоя тренда для повышения прибыльности.

- Построение более строгой системы управления капиталом для контроля торговых рисков.

Заключение

В целом, стратегия разворота тренда на основе трёх свечей использует простые ценовые паттерны в сочетании с несколькими вспомогательными индикаторами и строится на основе сбалансированного соотношения риска и доходности. Она является краткосрочной торговой стратегией. При относительно низкой сложности она демонстрирует неплохие результаты, заслуживает внимания и тестирования инвесторами, а также имеет множество возможностей для улучшения. Путём оптимизации параметров и дополнения правил она может превратиться в стабильную и эффективную стратегию количественной торговли.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © platsn

//

// Mainly developed for SPY trading on 1 min chart. But feel free to try on other tickers.- 1