Новая количественная торговая стратегия на основе паттерна ABCD с трейлинг-стоп-лоссом и трейлинг-тейк-профитом

1. Обзор стратегии

Название стратегии — «Лучшая стратегия торговли по паттерну ABCD (с трейлинг-стопом и трейлинг-тейк-профитом)». Это количественная стратегия, основанная на четкой модели ценового паттерна ABCD для совершения торговых операций. Основная идея заключается в идентификации полного паттерна ABCD, после чего открывается длинная или короткая позиция в зависимости от направления паттерна, а для управления позицией устанавливаются стоп-лосс и тейк-профит с трейлингом.

2. Принцип работы стратегии

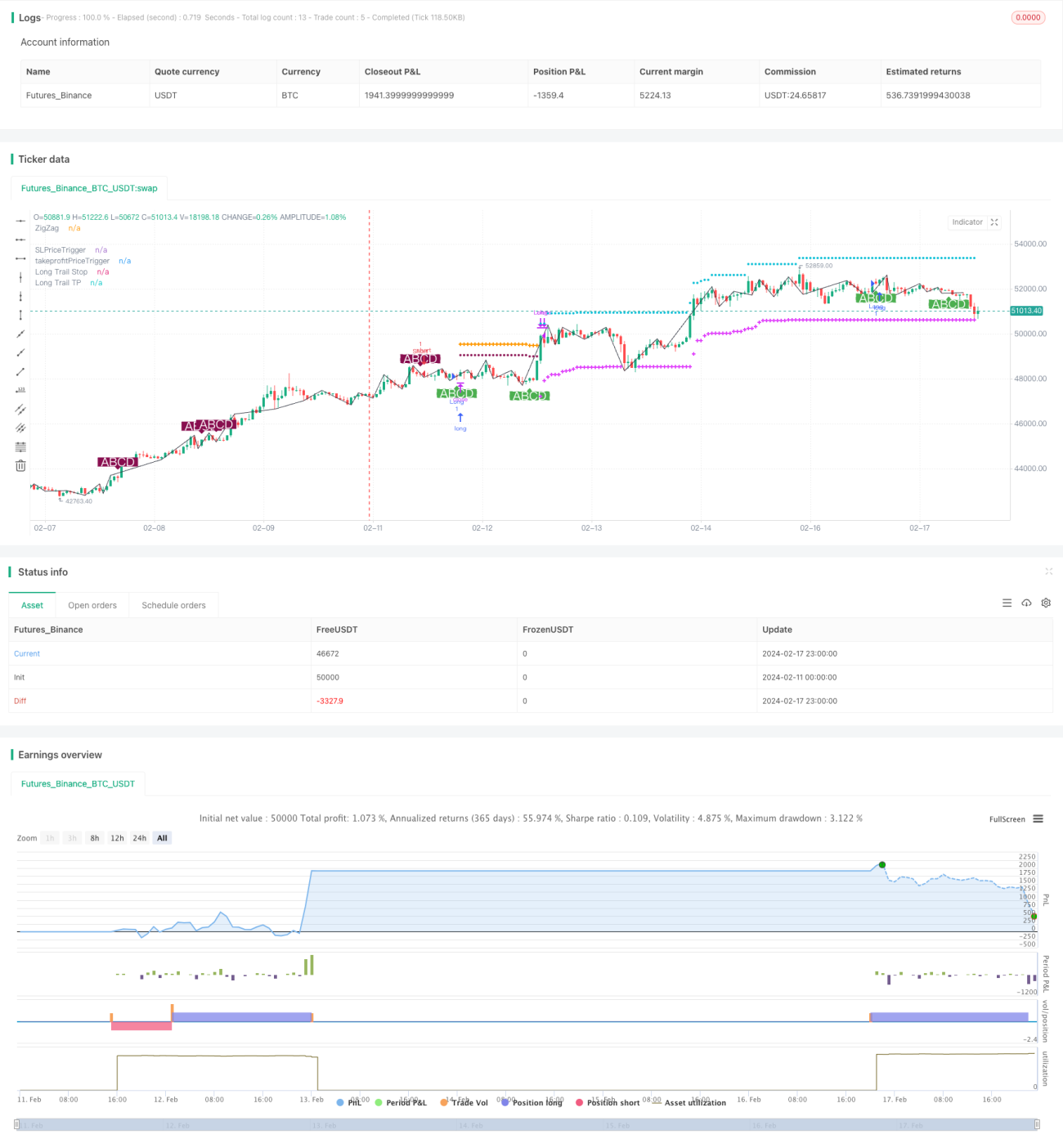

- Для определения точек вершин и впадин цены используется метод вспомогательного определения с помощью полос Боллинджера, в результате чего получается кривая ZigZag.

- На кривой ZigZag идентифицируется полный паттерн ABCD, причем точки A, B, C, D должны удовлетворять определенным пропорциональным соотношениям. После обнаружения соответствующего паттерна ABCD открывается длинная или короткая позиция.

- После открытия позиции устанавливается трейлинг-стоп для контроля риска. Первоначально используется фиксированный стоп-лосс, а после достижения определенного процента прибыли он переключается на скользящий стоп для фиксации части прибыли.

- Аналогично настраивается трейлинг-тейк-профит для своевременного закрытия позиции после получения достаточной прибыли и предотвращения ее потери. Трейлинг-тейк-профит также состоит из двух этапов: сначала используется фиксированный тейк-профит для фиксации части прибыли, затем он переключается на скользящий тейк-профит для продолжения отслеживания цены.

- Когда цена достигает скользящего стопа или тейк-профита, позиция закрывается, завершая один торговый цикл.

3. Анализ преимуществ стратегии

- Использование метода вспомогательного определения с помощью полос Боллинджера для идентификации кривой ZigZag позволяет избежать проблемы перерисовки, характерной для традиционных кривых ZigZag, делая торговые сигналы более надежными.

- Торговая модель ABCD является зрелой и стабильной, торговые возможности достаточно обильны. Кроме того, направление паттерна ABCD четко определено, что облегчает определение направления входа в рынок.

- Установка двухэтапного трейлинг-стопа и тейк-профита позволяет лучше контролировать риски и получать прибыль. Скользящие стоп и тейк-профит делают стратегию более гибкой.

- Параметры стратегии разумно спроектированы: проценты стоп-лосса и тейк-профита, а также процент активации трейлинга могут быть настроены индивидуально, что обеспечивает гибкость использования.

- Стратегия может применяться к любым инструментам, включая форекс, криптовалюты и фондовые индексы.

4. Анализ рисков стратегии

- Хотя паттерн ABCD достаточно четкий, торговые возможности относительно ограничены, и не гарантируется достаточная частота сделок.

- В условиях бокового рынка может наблюдаться частое срабатывание стоп-лоссов и тейк-профитов. В этом случае необходимо скорректировать параметры, расширив диапазон стоп-лосса и тейк-профита.

- Необходимо учитывать ликвидность торгуемого инструмента. Для инструментов с низкой ликвидностью точное исполнение стоп-лоссов и тейк-профитов затруднено.

- Стратегия чувствительна к торговым издержкам, поэтому необходимо выбирать брокеров и счета с низкими комиссиями.

- Некоторые параметры могут быть дополнительно оптимизированы, например, можно протестировать различные значения условий активации скользящего стопа и тейк-профита, чтобы найти оптимальные точки.

5. Направления оптимизации стратегии

- Можно комбинировать с другими индикаторами и добавить больше фильтров, чтобы избежать некоторых ложных паттернов. Это позволит сократить количество неэффективных сделок.

- Добавить анализ трехфазной структуры рынка и искать торговые возможности только в третьей фазе. Это может повысить процент выигрышных сделок.

- Протестировать и оптимизировать начальный размер капитала, чтобы найти оптимальный уровень. Слишком большой или слишком маленький капитал не способствует получению наилучшей доходности.

- Можно протестировать на данных вне выборки, чтобы проверить робастность параметров. Это необходимо для понимания долгосрочной стабильности стратегии.

- Продолжить оптимизацию условий активации скользящего стопа/тейк-профита и величины проскальзывания, чтобы повысить эффективность исполнения стратегии. Оптимизация настроек бесконечна.

6. Заключение

Данная стратегия в основном полагается на ценовой паттерн ABCD для принятия решений и входа в рынок. Для управления рисками и прибылью устанавливается двухэтапный трейлинг-стоп и тейк-профит. Стратегия достаточно зрелая и стабильная, однако частота сделок может быть низкой. Мы можем получить более эффективные торговые возможности, добавив фильтры. Кроме того, дальнейшая оптимизация параметров и размера капитала также может повысить стабильную прибыльность стратегии. В целом, стратегия имеет четкую логику, проста для понимания и реализации, и представляет собой количественную торговую стратегию, заслуживающую углубленного изучения и применения.

- 1