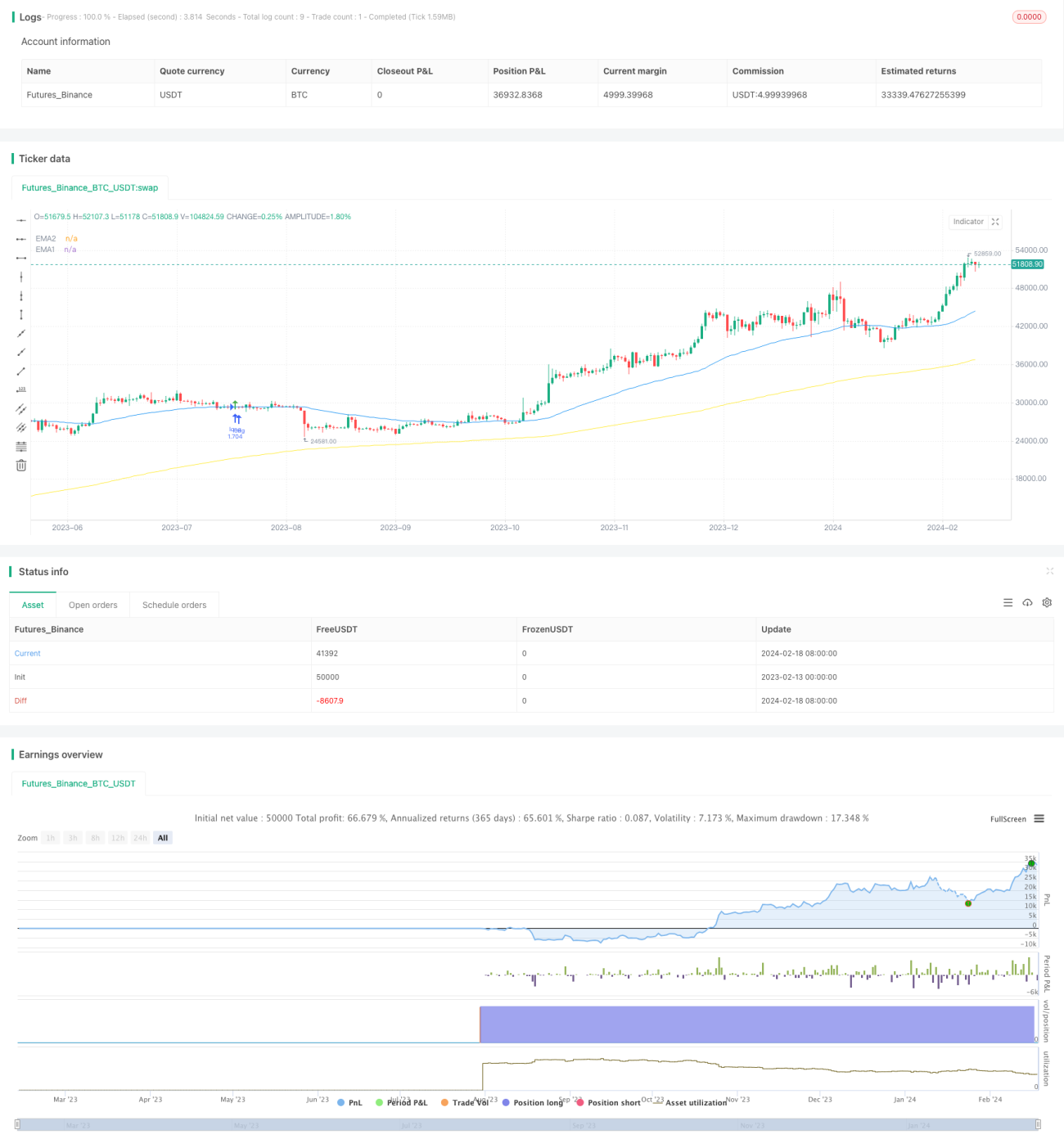

Стратегия следования за трендом на основе пробоя комбинации индикаторов

Обзор

Данная стратегия называется «Стратегия следования за трендом на основе комбинации индикаторов». Она комплексно использует несколько индикаторов для определения направления рыночного тренда и выполняет операции следования за трендом. Включает следующие основные части:

- Использование волнового трендового индикатора для определения основного тренда рынка.

- Комбинация индикатора RSI и индикатора денежного потока для фильтрации ложных сигналов.

- Использование индикатора EMA для определения конкретного направления действий.

- Вход в позицию по методу пробоя с последующим движением, чтобы следовать за трендом.

Принцип стратегии

Стратегия в основном определяет направление и силу крупного тренда, а также устанавливает двусторонние сделки (лонг и шорт). Конкретный принцип работы следующий:

Сигнал на вход в лонг:

- Цена выше 200-дневной EMA, что указывает на бычий рынок.

- Цена откатывается к 50-дневной EMA, образуя поддержку.

- Волновой индикатор разворачивается в восходящий тренд и подает сигнал на покупку.

- RSI и MFI показывают перекупленность.

- Последовательное пробитие 50-дневной EMA тремя свечами подряд, что указывает на прорыв вверх.

Сигнал на вход в шорт:

Противоположен сигналу на вход в лонг.

Способы стоп-лосса и тейк-профита:

Предусмотрены два варианта: стоп-лосс по минимуму/максимуму цены и стоп-лосс по ATR.

Анализ преимуществ стратегии

Данная стратегия обладает следующими преимуществами:

- Комплексная оценка крупного тренда с помощью нескольких индикаторов позволяет избежать ложных пробоев.

- Использование EMA для определения направления действий облегчает следование за трендом.

- Метод скользящего стоп-лосса позволяет получать постоянную прибыль.

- Возможность одновременно открывать как длинные, так и короткие позиции, следуя за движением рынка в любом направлении.

Анализ рисков стратегии

Стратегия также имеет некоторые риски:

- Вероятность ложных сигналов от индикаторов.

- Слишком узкий стоп-лосс увеличивает риск его срабатывания.

- Большое количество сделок приводит к скрытым потерям в виде комиссий.

Для снижения указанных рисков можно провести оптимизацию по следующим направлениям:

- Настройка параметров индикаторов для фильтрации ложных сигналов.

- Соответствующее расширение стоп-лосса.

- Оптимизация параметров индикаторов для уменьшения количества сделок.

Направления оптимизации стратегии

С точки зрения кода, основными направлениями оптимизации стратегии являются:

- Настройка параметров волнового индикатора, RSI и MFI для поиска наилучшего сочетания.

- Тестирование эффективности различных периодов EMA.

- Настройка коэффициента соотношения риска и доходности тейк-профита и стоп-лосса для получения оптимальной конфигурации.

Путем настройки и тестирования параметров можно добиться максимальной доходности при снижении просадок и рисков.

Заключение

Данная стратегия комплексно использует несколько индикаторов для определения направления крупного тренда, применяет EMA в качестве сигнала для конкретных операций и использует метод скользящего стоп-лосса для фиксации прибыли. Благодаря оптимизации параметров можно получить стабильную доходность. Однако следует также учитывать определенные системные риски и постоянно отслеживать эффективность индикаторов и изменения рыночной среды.

- 1