Стратегия торговли золотом на основе моментума и стандартного отклонения

Обзор

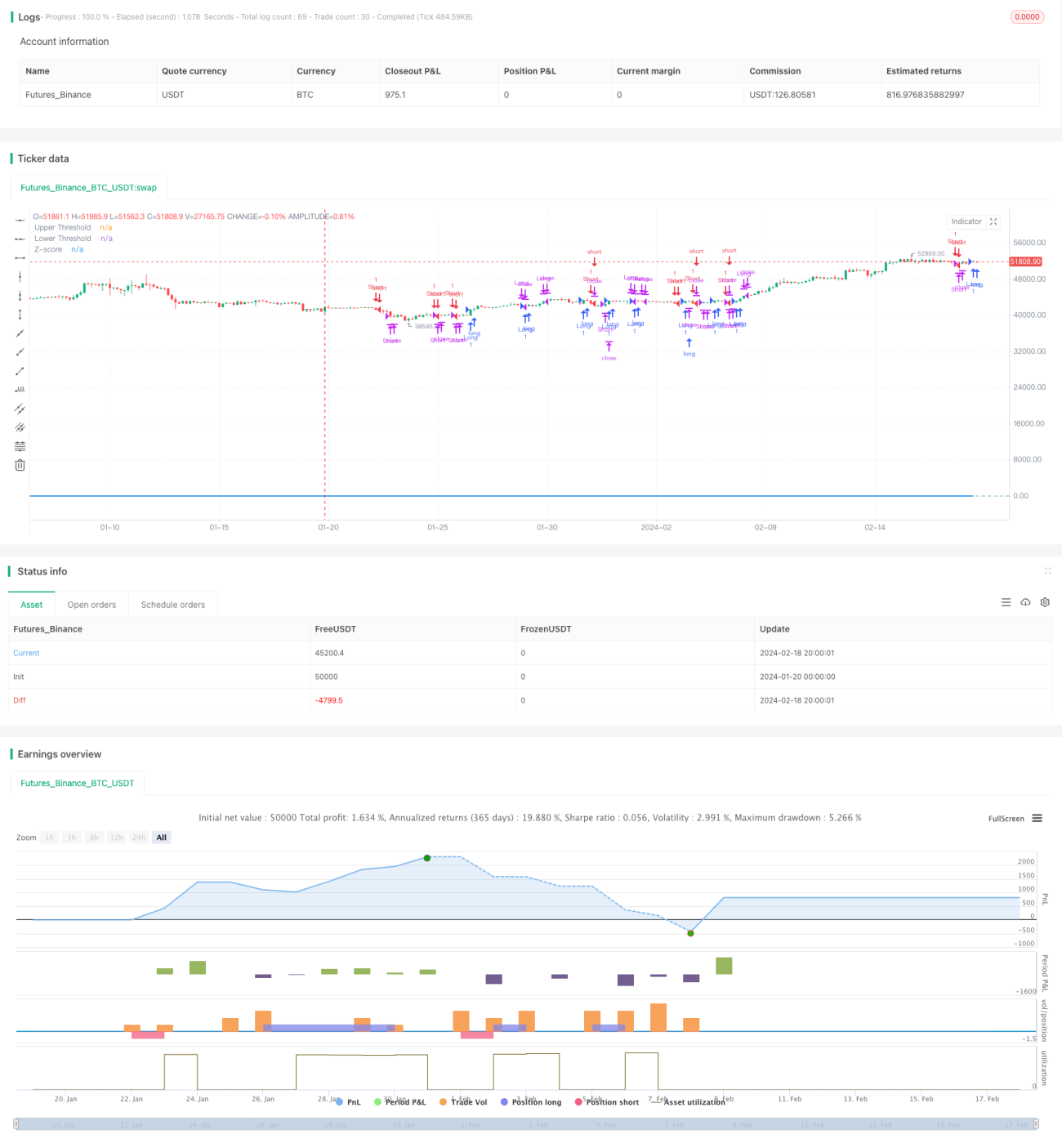

Данная стратегия основана на расчете отклонения цены золота от 21-дневной экспоненциальной скользящей средней (EMA) в сочетании со стандартным отклонением для определения состояний перекупленности и перепроданности рынка. При достижении определенного стандартного отклонения применяется стратегия следования за трендом с механизмом стоп-лосса для контроля рисков.

Принцип стратегии

- Рассчитывается 21-дневная EMA в качестве центральной оси.

- Вычисляется отклонение цены золота от скользящей средней.

- Отклонение стандартизируется и преобразуется в Z-оценку.

- Когда Z-оценка пересекает уровень 0,5 вверх – открывается длинная позиция; при пересечении вниз уровня -0,5 – открывается короткая позиция.

- При возврате Z-оценки к порогу 0,5/-0,5 позиция закрывается.

- При выходе Z-оценки за пределы 3/-3 – срабатывает стоп-лосс.

Анализ преимуществ

Это трендовая стратегия, основанная на ценовом моментуме и стандартном отклонении для определения перекупленности/перепроданности, обладающая следующими преимуществами:

- Использование скользящей средней в качестве динамической поддержки/сопротивления позволяет улавливать тренды.

- Стандартное отклонение и Z-оценка хорошо определяют состояния перекупленности/перепроданности, снижая количество ложных сигналов.

- Применение экспоненциальной скользящей средней придает больший вес последним ценам, что делает стратегию более чувствительной.

- Стандартизация отклонения цены с помощью Z-оценки делает правила оценки более единообразными и системными.

- Наличие механизма стоп-лосса позволяет своевременно ограничивать убытки и контролировать риски.

Анализ рисков

У данной стратегии также есть некоторые риски:

- Использование скользящей средней в качестве основы для оценки может приводить к ложным сигналам при значительных гэпах или пробоях цены.

- Пороги стандартного отклонения и Z-оценки требуют корректной настройки: слишком большие или слишком маленькие значения ухудшат эффективность стратегии.

- Неправильная настройка стоп-лосса может быть слишком агрессивной и приводить к ненужным убыткам.

- Резкие колебания цены из-за непредвиденных событий могут активировать стоп-лосс и привести к упущению тренда.

Способы решения:

- Разумно настроить параметры скользящей средней для выявления основного тренда.

- Оптимизировать параметры стандартного отклонения с помощью бэктестинга для поиска наилучших порогов.

- Использовать trailing stop для проверки обоснованности стоп-лосса стратегии.

- После наступления события своевременно переоценивать рыночную ситуацию и корректировать параметры стратегии.

Направления оптимизации

Стратегию можно улучшить по следующим направлениям:

- Использовать индикатор волатильности, например ATR, вместо простого стандартного отклонения для лучшей оценки склонности к риску.

- Протестировать различные типы скользящих средних для поиска более подходящего центрального индикатора.

- Оптимизировать параметры скользящей средней для определения оптимального периода.

- Оптимизировать пороги Z-оценки для поиска точки с наилучшей производительностью стратегии.

- Добавить метод стоп-лосса, основанный на волатильности, чтобы сделать его более интеллектуальным и обоснованным.

Заключение

В целом данная стратегия представляет собой обоснованную трендовую стратегию. Она использует скользящую среднюю для определения основного направления тренда, а стандартизация отклонения цены позволяет четко выявлять состояния перекупленности/перепроданности рынка, генерируя таким образом торговые сигналы. Разумный стоп-лосс также позволяет стратегии контролировать риски, сохраняя прибыльность. Дальнейшая оптимизация параметров и добавление дополнительных условий могут сделать стратегию более стабильной и надежной, обладающей высокой практической ценностью.

- 1