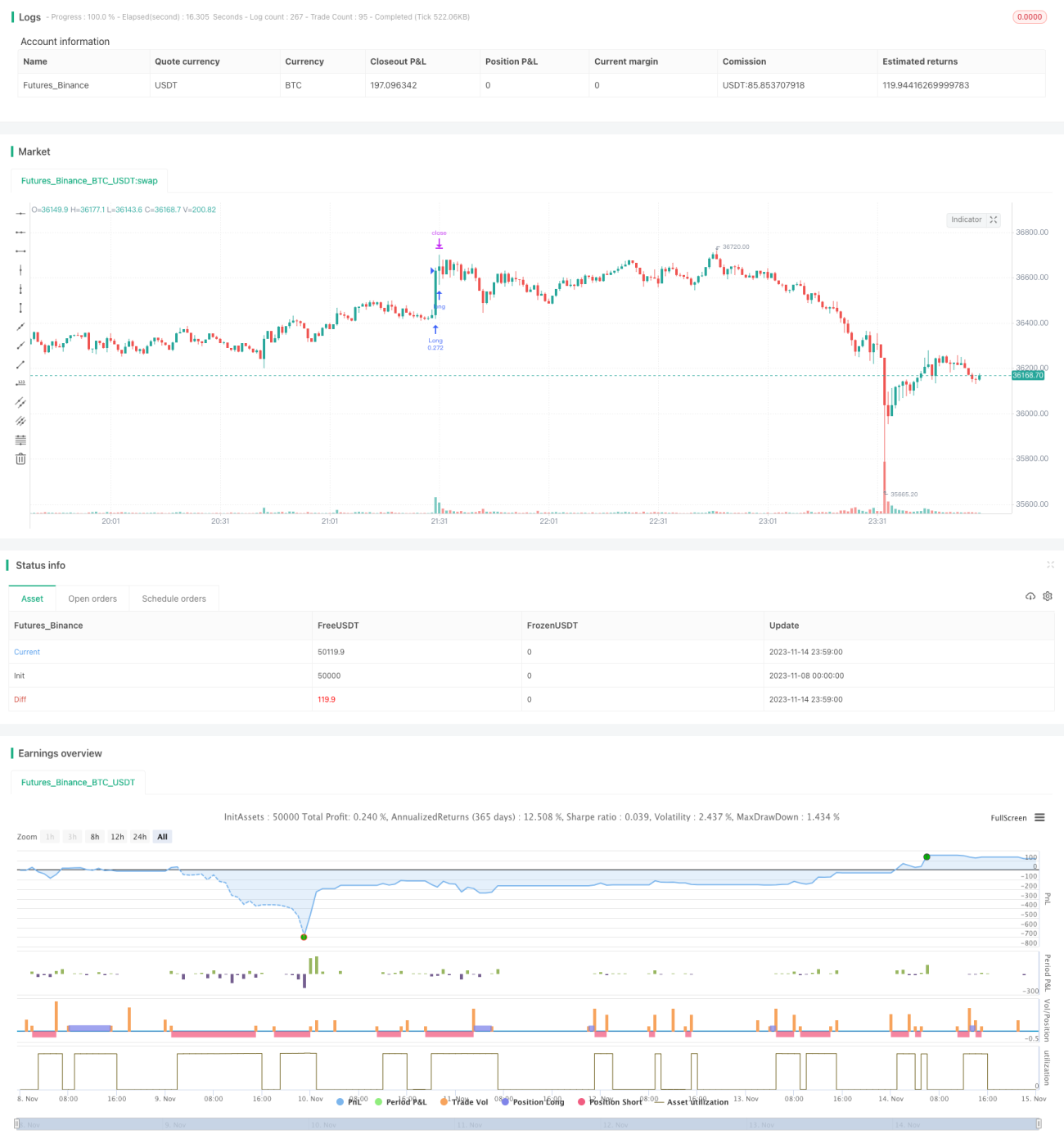

کثیر رجحانی حکمت عملی

خلاصہ

یہ حکمت عملی مختلف اشاریوں کو ملا کر رجحان کی سمت کی نشاندہی کرتی ہے اور رجحان کی پیروی کے طریقے سے درمیانی اور مختصر مدت میں مواقع حاصل کرتی ہے۔ یہ حکمت عملی خاص طور پر رجحان کی پیروی کے لیے تیار کی گئی ہے تاکہ کامیابی کی شرح بڑھے اور نقصانات کم ہوں۔

حکمت عملی کا اصول

- WVAP اشارے کا استعمال کرتے ہوئے قیمت کے تناسب کا تعین کریں؛

- RSI اشارے سے تیزی اور مندی کی رفتار کا اندازہ لگائیں؛

- QQE اشارے سے قیمت کی بریک آؤٹ کی نشاندہی کریں؛

- ADX اشارے سے رجحان کی طاقت کا تعین کریں؛

- Coral Trend Indicator سے بنیادی رجحان کا تعین کریں؛

- LSMA اشارے سے رجحان کی معاونت کریں؛

- مختلف اشاریوں کے سگنلز کو ملا کر تجارتی سگنل جاری کریں۔

یہ حکمت عملی بنیادی طور پر RSI, QQE, ADX جیسے متعدد اشاریوں پر انحصار کرتی ہے تاکہ رجحان کی سمت اور طاقت کا تعین کیا جا سکے، اور Coral Trend Indicator کے منحنی خط کو بنیادی رجحان کے معیار کے طور پر استعمال کرتی ہے۔ جب RSI جیسے اشارے خریداری کا سگنل دیتے ہیں اور Coral Trend Indicator بھی اوپر کی طرف رجحان دکھاتا ہے، تو اس کا امکان زیادہ ہوتا ہے کہ رجحان اوپر کی طرف ہے، اس صورت میں حکمت عملی خریداری کا انتخاب کرے گی۔ WVAP جیسے اشاریے بنیادی طور پر قیمت کی مناسبیت کا تعین کرنے اور اونچی قیمتوں پر خریداری سے بچنے کے لیے استعمال ہوتے ہیں۔

حکمت عملی کے فوائد

- متعدد اشاریوں کا امتزاج، فیصلہ سازی کی درستگی میں اضافہ؛

- رجحان کی پیروی پر زور، منافع کے امکانات میں اضافہ؛

- بریک آؤٹ کے نقطہ نظر کا استعمال، ٹریڈنگ رینج مارکیٹوں کی چھانٹی؛

- بنیادی اشاریوں کا استعمال، مخالف رجحان کی تجارت سے بچنا؛

- تجارتی وقت اور لاٹ سائز کی مناسب ترتیب، خطرے میں کمی؛

- حکمت عملی کا واضح تصور، سمجھنے اور بہتر بنانے میں آسانی۔

اس حکمت عملی کا سب سے بڑا فائدہ متعدد اشاریوں کا مشترکہ فیصلہ ہے جو ایک اشارے کی غلط تشخیص کے امکان کو کسی حد تک کم کر سکتا ہے اور فیصلہ سازی کی درستگی کو بڑھا سکتا ہے۔ اس کے ساتھ ساتھ رجحان کی پیروی اور بریک آؤٹ کے نقطہ نظر پر زور دینے سے قابل اعتماد درمیانی اور مختصر مدتی مواقع کی نشاندہی میں مدد ملتی ہے۔ مزید برآں، حکمت عملی میں بنیادی اشاریوں کو شامل کرنے سے مخالف رجحان کے کاموں سے بچا جا سکتا ہے۔ یہ تمام ڈیزائن حکمت عملی کے استحکام اور منافع کے امکانات کو بڑھاتے ہیں۔

حکمت عملی کے خطرات

- تیزی اور مندی کے فیصلوں میں تاخیر ہو سکتی ہے، جس کی وجہ سے داخلے کا بہترین موقع ضائع ہو سکتا ہے؛

- نقصانات پر قابو پانا مکمل نہیں ہے، بڑے نقصانات کا خطرہ موجود ہے؛

- جب بنیادی رجحان میں تبدیلی آتی ہے تو حکمت عملی سگنل سے محروم ہو سکتی ہے؛

- تجارتی اخراجات پر غور نہیں کیا گیا، عملی استعمال میں منافع میں کمی کا خطرہ ہے۔

اس حکمت عملی کا سب سے بڑا خطرہ متعدد اشاریوں کے مشترکہ فیصلے میں تاخیر کا امکان ہے، جس کی وجہ سے داخلے کا بہترین موقع ضائع ہو سکتا ہے اور منافع کے دائرے پر اثر پڑ سکتا ہے۔ اس کے علاوہ، حکمت عملی میں نقصانات پر قابو پانا اطمینان بخش نہیں ہے اور بڑے نقصانات کا خطرہ موجود ہے۔ جب مارکیٹ کا بنیادی رجحان تبدیل ہوتا ہے اور اشاریے اس کی عکاسی نہیں کرتے تو نقصان کا سامنا کرنا پڑ سکتا ہے۔ عملی استعمال میں تجارتی اخراجات بھی منافع پر کچھ اثر ڈال سکتے ہیں۔

حکمت عملی کی بہتری کے رخ

- اسٹاپ لاس کی حکمت عملی شامل کرنا، نقصانات پر قابو پانے میں بہتری؛

- پیرامیٹرز کی ترتیب کو بہتر بنانا، اشاریوں کی تاخیر کو کم کرنا؛

- بنیادی اشاریوں کے استعمال میں اضافہ، درستگی میں بہتری؛

- مشین لرننگ الگورتھم کا استعمال کرتے ہوئے متحرک پیرامیٹر بہتری۔

اس حکمت عملی کی بہتری کا مرکز نقصانات پر قابو پانے پر ہونا چاہیے۔ منافع کو محفوظ رکھنے اور نقصانات کو کم کرنے کے لیے متحرک اسٹاپ لاس کی حکمت عملی شامل کی جا سکتی ہے۔ اس کے ساتھ ساتھ پیرامیٹرز کی ترتیب کو بہتر بنا کر اشاریوں کی تاخیر کو کم کیا جا سکتا ہے اور مارکیٹ کی تبدیلیوں کے لیے حکمت عملی کی حساسیت بڑھائی جا سکتی ہے۔ مزید برآں، بنیادی فیصلہ کرنے والے مزید اشاریے شامل کیے جا سکتے ہیں تاکہ درستگی بڑھے۔ اگر مشین لرننگ کے طریقوں سے پیرامیٹرز کی متحرک بہتری ممکن ہو تو اس سے حکمت عملی کے استحکام میں نمایاں بہتری آئے گی۔

خلاصہ

یہ حکمت عملی متعدد اشاریوں کو ملا کر رجحان کی سمت کا تعین کرتی ہے اور رجحان کی پیروی کے تصور پر مبنی ہے تاکہ فیصلہ سازی کی درستگی میں اضافہ اور منافع کے امکانات بڑھائے جا سکیں۔ حکمت عملی میں اشاریوں کے امتزاج، رجحان کی پیروی پر زور، اور بنیادی اشاریوں کے استعمال جیسے فوائد ہیں، لیکن اس میں غلط تشخیص، تاخیر، اور نقصانات پر قابو پانے کی کمی جیسے مسائل بھی ہیں۔ مستقبل میں پیرامیٹرز کی ترتیب کو بہتر بنا کر، اسٹاپ لاس کی حکمت عملی کو مکمل کر کے، اور بنیادی اشاریوں میں اضافہ کر کے اسے بہتر بنایا جا سکتا ہے تاکہ عملی استعمال میں بہتر نتائج حاصل ہوں۔

- 1