Chiến lược giao dịch đảo chiều dựa trên hỗ trợ/kháng cự tổng quát

Tổng quan

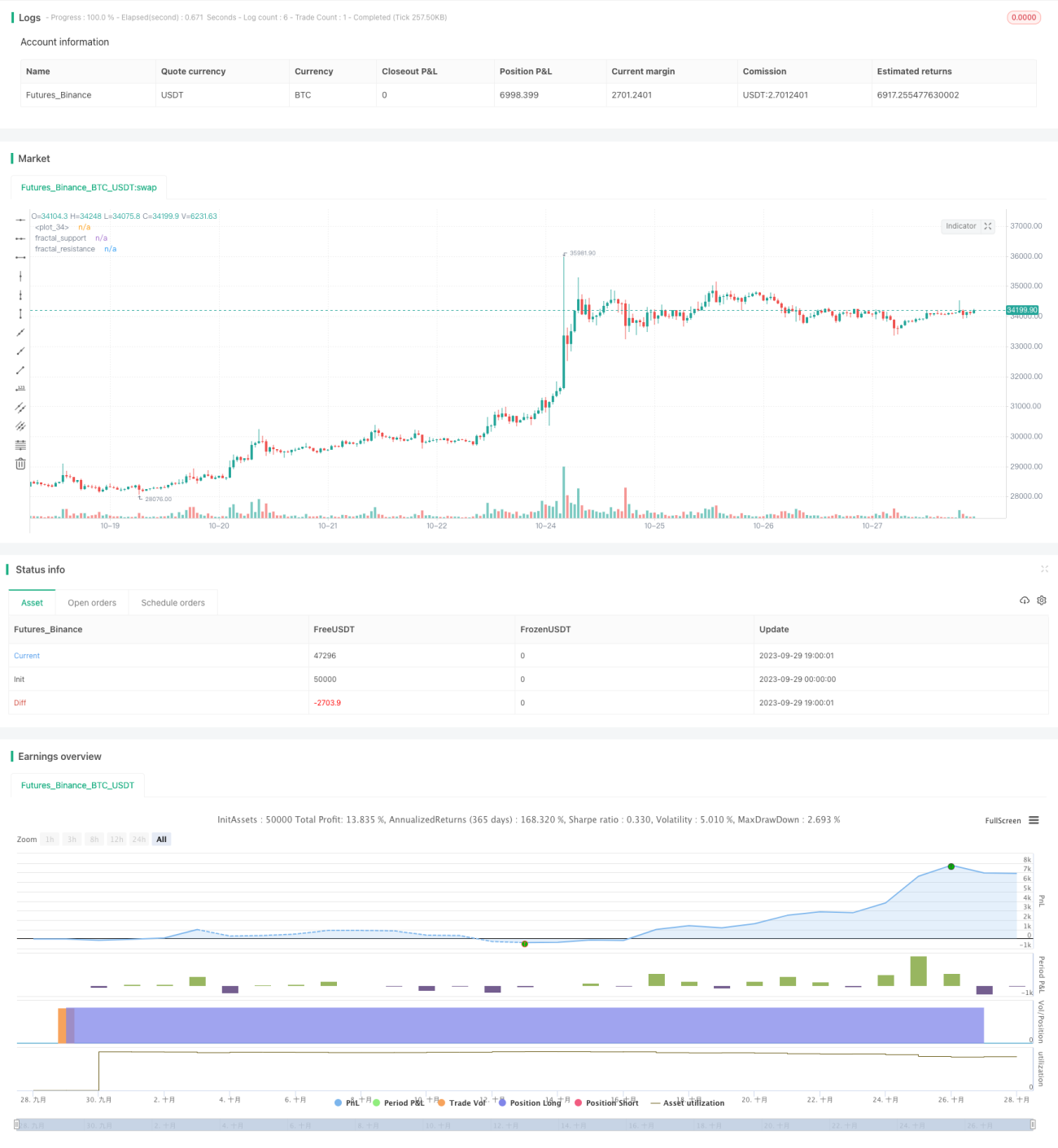

Chiến lược này dựa trên chỉ báo đa yếu tố dài/ngắn để thực hiện giao dịch đảo chiều, đồng thời thiết lập các điểm chốt lời mục tiêu. Cốt lõi của yếu tố dài/ngắn là "hỗ trợ/kháng cự mở rộng" dựa trên khối lượng giao dịch, phù hợp với các tài sản có khối lượng giao dịch và biến động cao. Ưu điểm của chiến lược là có thể nắm bắt các cơ hội đảo chiều xu hướng trung và ngắn hạn lớn, giúp thu lợi nhanh; nhưng cũng tồn tại rủi ro bị kẹt lệnh.

Nguyên lý chiến lược

-

Xác định yếu tố dài/ngắn dựa trên "hỗ trợ/kháng cự mở rộng" theo khối lượng

- Sử dụng mô hình nến để nhận diện hỗ trợ/kháng cự cổ điển, lọc các phá vỡ giả bằng khối lượng giao dịch lớn

- Hỗ trợ/kháng cự mở rộng có tính bao phủ tốt hơn so với mô hình cổ điển

- Phá vỡ hỗ trợ mở rộng là tín hiệu yếu tố dài (long), phá vỡ kháng cự mở rộng là tín hiệu yếu tố ngắn (short)

-

Giao dịch đảo chiều

- Sau khi tín hiệu yếu tố được phát ra, thực hiện hành động ngược lại

- Nếu đã có vị thế, thực hiện giảm vị thế ngược chiều hoặc mở vị thế ngược lại

-

Thiết lập mục tiêu lợi nhuận

- Đặt stop loss dựa trên ATR

- Thiết lập nhiều điểm chốt lời mục tiêu như 1R/2R/3R

- Khi đạt các mức lợi nhuận khác nhau, giảm vị thế dần

Phân tích ưu điểm

-

Có thể nắm bắt đảo chiều trung và ngắn hạn với biên độ lớn

Việc phá vỡ hỗ trợ/kháng cự đại diện cho tín hiệu đảo chiều xu hướng mạnh, có độ tin cậy nhất định, có thể nắm bắt đảo chiều lớn trong trung và ngắn hạn.

-

Thu lợi nhanh, drawdown nhỏ

Thông qua việc thiết lập stop loss và nhiều mức chốt lời, có thể đạt lợi nhuận nhanh và hạn chế drawdown của từng cổ phiếu.

-

Phù hợp với các tài sản có dòng vốn tổ chức lớn và biến động cao

Chiến lược này phụ thuộc vào chỉ báo khối lượng giao dịch, cần có đủ dòng vốn tổ chức đổ vào để hỗ trợ xu hướng; đồng thời cần một không gian biến động nhất định để đạt lợi nhuận.

Phân tích rủi ro

-

Rủi ro bị kẹt lệnh trong thị trường đi ngang

Khi thị trường dao động, việc thoát lệnh stop loss rồi vào lại ngược chiều có thể dẫn đến bị kẹt thường xuyên.

-

Rủi ro hỗ trợ/kháng cự mất hiệu lực

Hỗ trợ/kháng cự mở rộng không hoàn toàn đáng tin cậy, có xác suất thất bại trong các pha kiểm tra đảo chiều.

-

Rủi ro vị thế một chiều

Chiến lược thuần đảo chiều, không xem xét theo xu hướng, có thể bỏ lỡ các cơ hội xu hướng lớn.

-

Về mặt quản lý rủi ro

- Có thể nới lỏng điều kiện yếu tố cho giao dịch đảo chiều, không nhất thiết phải đảo chiều mỗi lần phá vỡ

- Có thể kết hợp các chỉ báo khác để lọc, như phân kỳ khối lượng-giá

- Có thể tối ưu hóa chiến lược stop loss để giảm xác suất bị kẹt

Hướng tối ưu

-

Tối ưu tham số khẩu độ (khoảng cách)

Tối ưu tham số của hỗ trợ/kháng cự mở rộng để nhận diện các yếu tố đáng tin cậy hơn

-

Tối ưu chiến lược chốt lời

Có thể thêm nhiều mức chốt lời hơn, hoặc sử dụng chốt lời không cố định

-

Tối ưu chiến lược stop loss

Điều chỉnh tham số ATR hoặc sử dụng stop loss thống kê (istics) để giảm chi phí giao dịch do stop loss không cần thiết

-

Kết hợp xu hướng và các yếu tố khác

Có thể đưa vào đường trung bình động và các chỉ báo xu hướng khác để tránh chống lại xu hướng mạnh; cũng có thể đưa vào các yếu tố phụ trợ khác

Tổng kết

Cốt lõi của chiến lược này là sử dụng giao dịch đảo chiều để nắm bắt các biến động lớn trong trung và ngắn hạn. Ý tưởng chiến lược đơn giản và trực tiếp, thông qua điều chỉnh tham số có thể đạt được hiệu quả thực tế tốt. Tuy nhiên, chiến lược đảo chiều khá mạnh mẽ, tồn tại rủi ro drawdown và bị kẹt nhất định, cần tối ưu hóa thêm chiến lược stop loss và chốt lời, đồng thời kết hợp hợp lý với nhận định xu hướng để giảm thiểu tổn thất không cần thiết.

- 1