Chiến lược đa xu hướng

Tổng quan

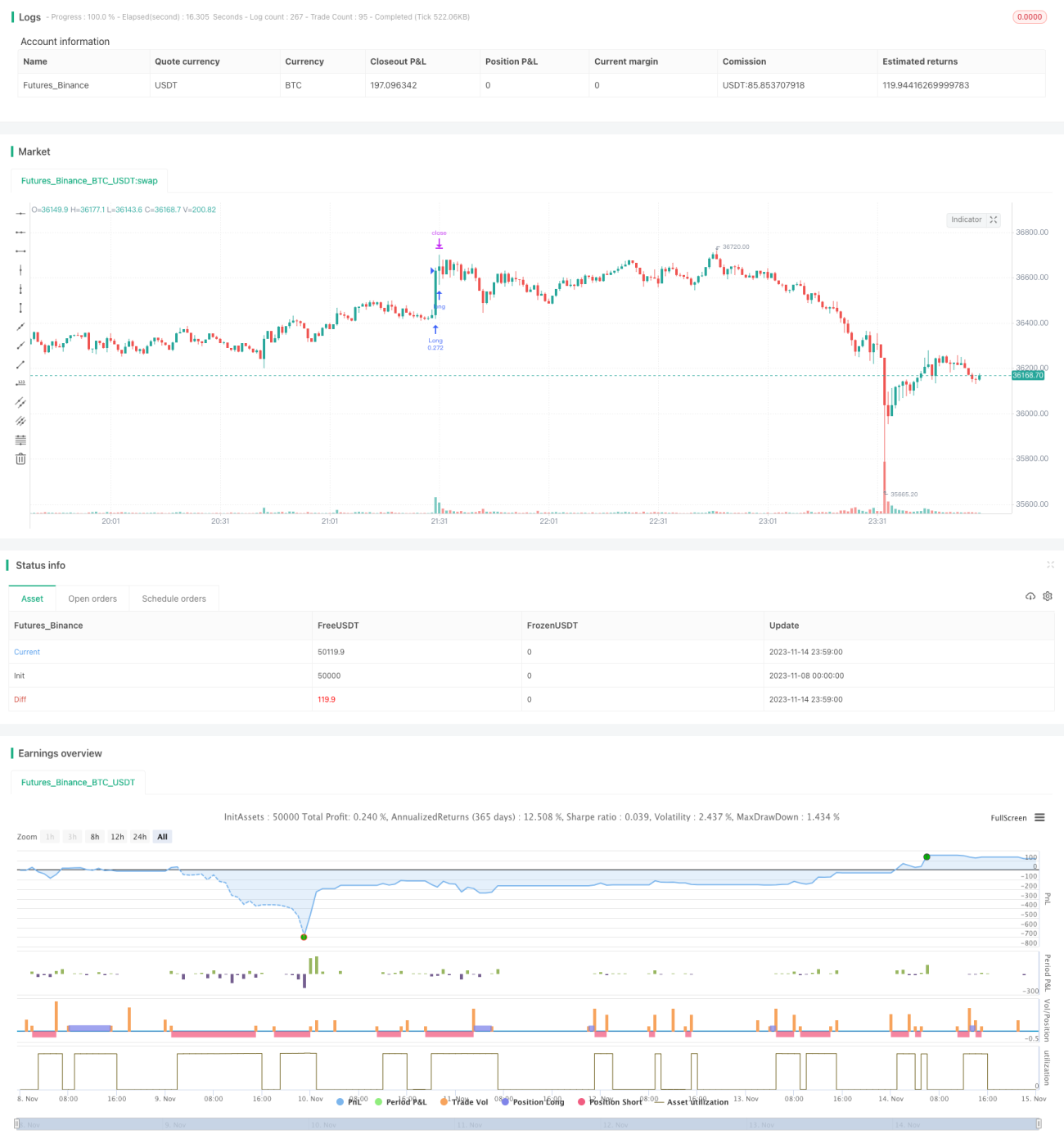

Chiến lược này kết hợp nhiều chỉ báo để xác định xu hướng, sử dụng phương pháp theo dõi xu hướng, nhằm nắm bắt cơ hội xu hướng trong trung và ngắn hạn. Chiến lược được thiết kế chuyên biệt để theo dõi xu hướng, nhằm tăng tỷ lệ thắng và giảm drawdown.

Nguyên lý chiến lược

-

Sử dụng chỉ báo WVAP để đánh giá tỷ lệ giá;

-

Chỉ báo RSI để đánh giá động lượng đa/không;

-

Chỉ báo QQE để xác định sự phá vỡ giá;

-

Chỉ báo ADX để đánh giá sức mạnh xu hướng;

-

Chỉ báo Coral Trend Indicator để đánh giá xu hướng cơ bản;

-

Chỉ báo LSMA hỗ trợ đánh giá xu hướng;

-

Kết hợp tín hiệu từ nhiều chỉ báo để đưa ra tín hiệu giao dịch.

Chiến lược này chủ yếu dựa vào nhiều chỉ báo như RSI, QQE, ADX để xác định hướng và sức mạnh xu hướng, đồng thời sử dụng đường của Coral Trend Indicator làm tiêu chuẩn đánh giá xu hướng cơ bản. Khi các chỉ báo như RSI phát ra tín hiệu mua, nếu Coral Trend Indicator cũng hiển thị đường tăng, thì khả năng cao xu hướng đang hướng lên, và chiến lược sẽ chọn mua. Các chỉ báo như WVAP chủ yếu được sử dụng để đánh giá mức giá hợp lý, tránh mua ở đỉnh.

Ưu điểm của chiến lược

-

Kết hợp nhiều chỉ báo, tăng độ chính xác trong đánh giá;

-

Nhấn mạnh theo dõi xu hướng, tăng xác suất sinh lời;

-

Áp dụng tư duy phá vỡ, lọc các thị trường Trading Range;

-

Kết hợp chỉ báo cơ bản, tránh giao dịch ngược xu hướng;

-

Cài đặt thời gian và khối lượng giao dịch hợp lý, giảm rủi ro;

-

Tư duy chiến lược rõ ràng, dễ hiểu và tối ưu.

Ưu điểm lớn nhất của chiến lược này là sự kết hợp nhiều chỉ báo, giúp giảm một phần xác suất đánh giá sai của từng chỉ báo đơn lẻ, tăng độ chính xác. Đồng thời nhấn mạnh theo dõi xu hướng và tư duy phá vỡ, hỗ trợ lọc ra các cơ hội trung ngắn hạn đáng tin cậy. Ngoài ra, chiến lược bổ sung chỉ báo cơ bản, có thể tránh giao dịch ngược xu hướng. Những thiết kế này đều nâng cao độ ổn định và xác suất sinh lời của chiến lược.

Rủi ro của chiến lược

-

Xác định đa/không có độ trễ, có thể bỏ lỡ thời điểm vào lệnh tốt nhất;

-

Kiểm soát drawdown chưa hoàn thiện, có rủi ro drawdown lớn;

-

Khi xu hướng cơ bản chuyển hướng, chiến lược có thể bỏ lỡ tín hiệu;

-

Chưa xem xét chi phí giao dịch, khi áp dụng thực tế lợi nhuận có thể giảm.

Rủi ro lớn nhất của chiến lược này là việc kết hợp nhiều chỉ báo có thể gây ra độ trễ đánh giá, dẫn đến bỏ lỡ thời điểm vào lệnh tốt nhất, ảnh hưởng đến không gian lợi nhuận. Ngoài ra, kiểm soát drawdown của chiến lược chưa lý tưởng, có rủi ro drawdown lớn. Khi xu hướng cơ bản của thị trường thay đổi mà các chỉ báo chưa phản ánh kịp, cũng dễ hình thành thua lỗ. Khi áp dụng thực tế, chi phí giao dịch cũng ảnh hưởng nhất định đến lợi nhuận.

Hướng tối ưu hóa chiến lược

-

Thêm chiến lược stop loss, tối ưu kiểm soát drawdown;

-

Tối ưu cài đặt tham số, rút ngắn độ trễ chỉ báo;

-

Tăng cường ứng dụng chỉ báo cơ bản, nâng cao độ chính xác;

-

Kết hợp thuật toán học máy, thực hiện tối ưu tham số động.

Trọng tâm tối ưu hóa của chiến lược này nên xem xét đến kiểm soát drawdown, có thể thêm chiến lược trailing stop loss để khóa lợi nhuận, giảm drawdown. Đồng thời có thể tối ưu cài đặt tham số, rút ngắn độ trễ chỉ báo, tăng độ nhạy của chiến lược đối với biến động thị trường. Ngoài ra, có thể bổ sung thêm chỉ báo đánh giá cơ bản, nâng cao độ chính xác. Nếu có thể sử dụng phương pháp học máy để thực hiện tối ưu tham số động, cũng sẽ cải thiện đáng kể độ ổn định của chiến lược.

Tổng kết

Chiến lược này kết hợp nhiều chỉ báo để xác định hướng xu hướng, được thiết kế theo tư duy theo dõi xu hướng, nhằm nâng cao độ chính xác trong đánh giá và tăng xác suất sinh lời. Chiến lược có ưu điểm như kết hợp chỉ báo, nhấn mạnh theo dõi xu hướng, kết hợp yếu tố cơ bản, nhưng cũng tồn tại các vấn đề như độ trễ đánh giá, kiểm soát drawdown chưa đầy đủ. Trong tương lai có thể cải thiện thông qua tối ưu cài đặt tham số, hoàn thiện chiến lược stop loss, tăng cường chỉ báo cơ bản, v.v., để chiến lược đạt hiệu quả tốt hơn khi ứng dụng thực tế.

- 1