Chiến lược chỉ báo kỹ thuật Bollinger Bands dựa trên phân rã chuỗi thời gian và trọng số khối lượng

Tổng quan

Chiến lược này kết hợp bốn chỉ báo kỹ thuật: Phân rã chuỗi thời gian, Giá trung bình theo khối lượng giao dịch, Dải Bollinger và Delta (OBV-PVT) nhằm đánh giá đa chiều về xu hướng giá, tình trạng quá mua/quá bán.

Nguyên lý chiến lược

- Sử dụng phân rã chuỗi thời gian để loại bỏ nhiễu và tính chu kỳ trong giá, từ đó có được nhận định xu hướng chính xác hơn;

- Dựa trên đường xu hướng đó, tính toán mức giá mới theo khối lượng giao dịch;

- Tính chỉ báo %B của Dải Bollinger dựa trên giá đóng cửa để xác định quá mua/quá bán;

- Tính %B của Dải Bollinger đối với biến động Delta(OBV-PVT), làm tiêu chí đánh giá phân kỳ khối lượng-giá;

- Sinh tín hiệu giao dịch dựa trên giao nhau tăng/giảm của các chỉ báo khối lượng-giá và hiện tượng vượt quá/rút lui của chỉ báo Dải Bollinger.

Phân tích ưu điểm

- Kết hợp nhiều phán đoán về giá, khối lượng và đặc tính thống kê, chiến lược có độ ổn định cao;

- Kết hợp %B và Delta(OBV-PVT) giúp nhận diện tốt hơn các hiện tượng quá mua/quá bán ngắn hạn;

- Tín hiệu giao nhau khối lượng-giá loại bỏ được một số điểm giao dịch nhiễu.

Phân tích rủi ro

- Cài đặt tham số quá phức tạp, khó điều chỉnh;

- Dao động ngắn hạn trong vùng sideway có thể làm tăng thua lỗ;

- Sự phân kỳ khối lượng-giá không thể hoàn toàn lọc bỏ tín hiệu sai lệch.

Có thể tối ưu hóa chiến lược bằng cách điều chỉnh chu kỳ đường trung bình, độ rộng Dải Bollinger và tỷ lệ rủi ro lợi nhuận, từ đó giảm tần suất giao dịch đồng thời nâng cao tỷ lệ lời/lỗ trên mỗi giao dịch.

Tổng kết

Chiến lược này tích hợp nhiều công cụ phân tích như phân rã chuỗi thời gian, Dải Bollinger, chỉ báo OBV,… thông qua sự kết hợp hữu cơ giữa quan hệ khối lượng-giá, đặc tính thống kê và nhận định xu hướng, giúp nhận diện các dao động ngắn hạn và nắm bắt hiệu quả xu hướng chính của thị trường. Tuy nhiên, vẫn tồn tại rủi ro nhất định và cần điều chỉnh tham số để đạt trạng thái tối ưu.

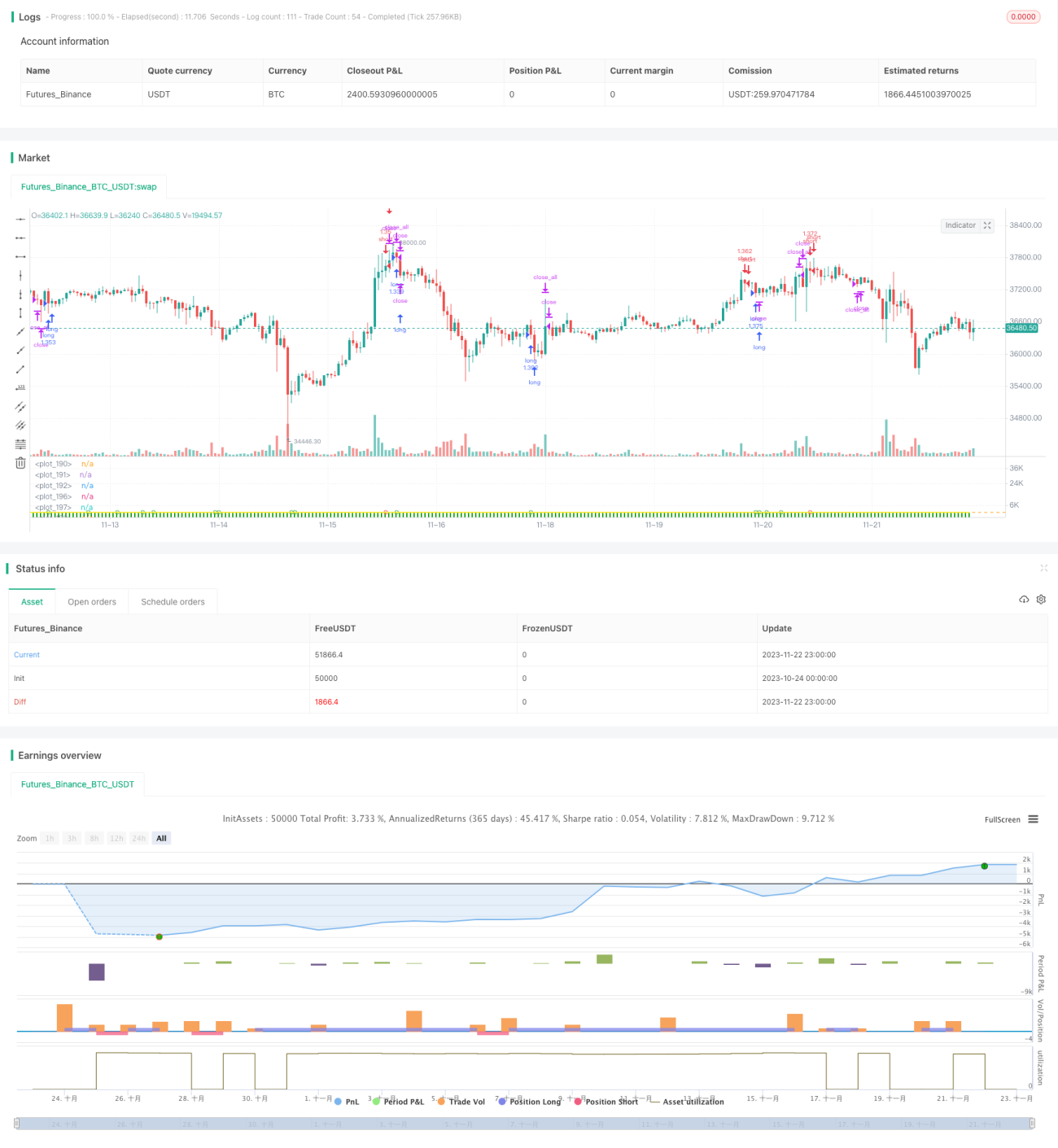

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © oakwhiz and tathal

- 1