Chiến lược giao dịch dựa trên đường EMA

Tổng quan

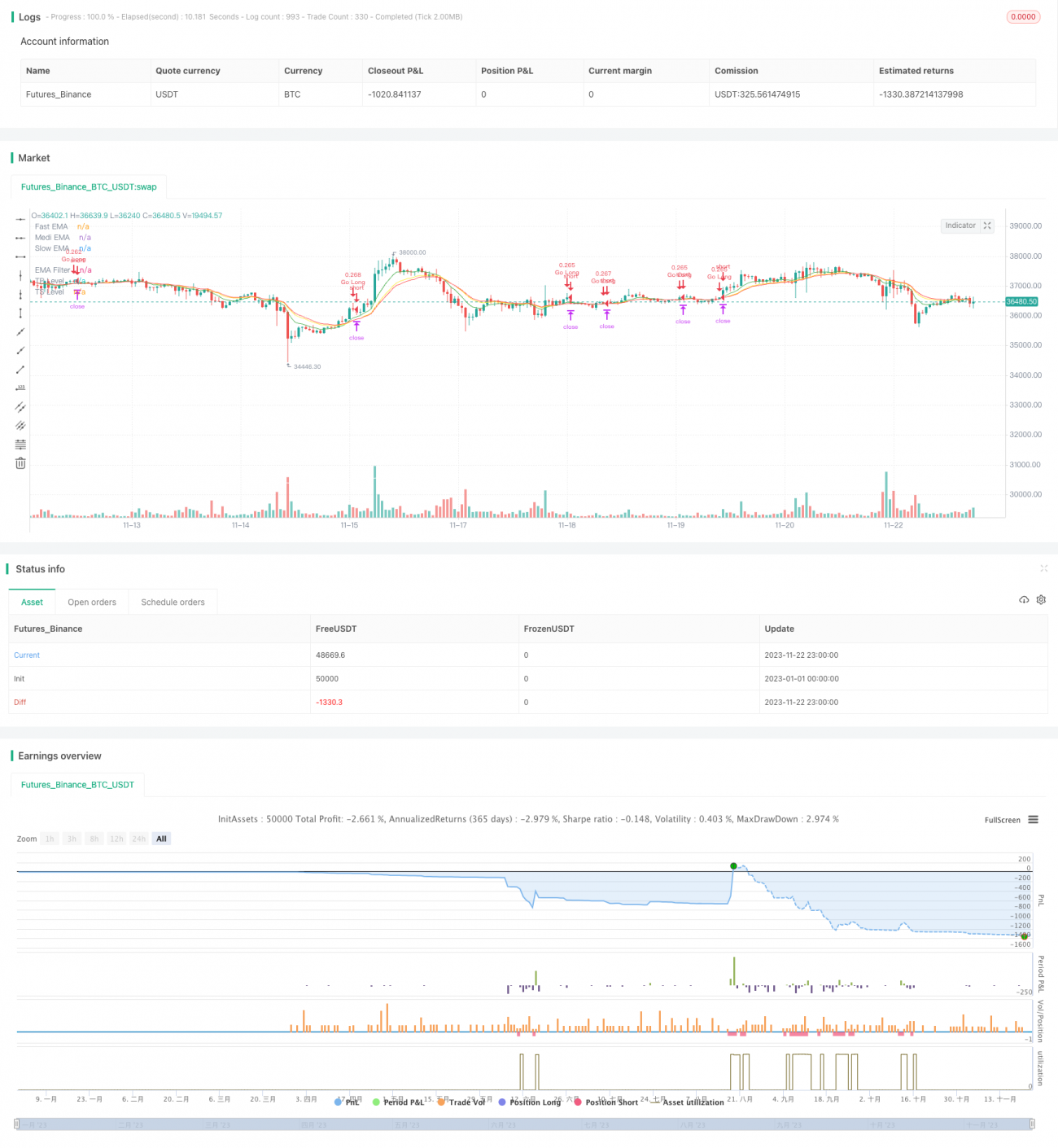

Chiến lược này sử dụng 4 đường EMA với các chu kỳ khác nhau, dựa trên thứ tự sắp xếp của chúng để hình thành tín hiệu giao dịch, tương tự như đèn giao thông với ba màu đỏ, vàng, xanh, do đó được đặt tên là "Chiến lược giao dịch đèn giao thông". Nó đánh giá thị trường từ cả hai góc độ xu hướng và đảo chiều, nhằm nâng cao độ chính xác của quyết định giao dịch.

Nguyên lý chiến lược

-

Thiết lập 3 đường EMA: đường nhanh (chu kỳ 8), đường trung bình (chu kỳ 14), đường chậm (chu kỳ 16), và thêm một đường EMA chu kỳ dài (100 chu kỳ) làm bộ lọc.

-

Xác định thứ tự sắp xếp của 3 đường EMA nhanh, trung bình, chậm và sự giao nhau với bộ lọc để xác định thời điểm mua và bán:

-

Khi đường nhanh cắt lên trên đường trung bình hoặc đường trung bình cắt lên trên đường chậm, đó là tín hiệu mua.

-

Khi đường trung bình cắt xuống dưới đường nhanh, đó là tín hiệu đóng vị thế mua.

-

Khi đường nhanh cắt xuống dưới đường trung bình hoặc đường trung bình cắt xuống dưới đường chậm, đó là tín hiệu bán.

-

Khi đường trung bình cắt lên trên đường nhanh, đó là tín hiệu đóng vị thế bán.

-

-

Thông qua thứ tự của 3 đường EMA nhanh, trung bình, chậm để xác định hướng và sức mạnh của xu hướng, kết hợp với sự giao nhau giữa các đường EMA và bộ lọc để xác định điểm đảo chiều, nhằm kết hợp hữu cơ giữa theo dõi xu hướng và bắt đáy.

Phân tích ưu điểm

Chiến lược này tích hợp ưu điểm của cả theo dõi xu hướng và giao dịch đảo chiều, có thể nắm bắt tốt cơ hội thị trường. Các ưu điểm chính bao gồm:

- Sử dụng nhiều đường EMA, khả năng đánh giá mạnh hơn, giảm tín hiệu nhiễu.

- Linh hoạt thiết lập điều kiện mua/bán, tránh bỏ lỡ cơ hội giao dịch.

- Sử dụng kết hợp các đường EMA chu kỳ ngắn và dài, đánh giá toàn diện.

- Có thể tùy chỉnh điều kiện chốt lời/cắt lỗ, kiểm soát rủi ro tốt.

Thông qua tối ưu hóa tham số, chiến lược này có thể thích ứng với nhiều loại tài sản hơn, thể hiện khả năng sinh lời và độ ổn định mạnh mẽ trong backtest.

Phân tích rủi ro

Các rủi ro chính của chiến lược này bao gồm:

- Khi thứ tự sắp xếp của nhiều đường EMA bị xáo trộn, sẽ làm tăng độ khó trong đánh giá, dẫn đến do dự giao dịch.

- Không thể lọc hiệu quả các tín hiệu nhiễu từ biến động bất thường của thị trường, ví dụ như gây thua lỗ trong các dao động lớn.

- Khi tham số cài đặt không phù hợp, điều kiện chốt lời/cắt lỗ có thể quá rộng hoặc quá chặt, dẫn đến mất lợi nhuận hoặc thua lỗ quá mức.

Khuyến nghị tiếp tục nâng cao độ ổn định của chiến lược và kiểm soát rủi ro thông qua tối ưu hóa tham số, thiết lập mức cắt lỗ, giao dịch thận trọng, v.v.

Hướng tối ưu hóa

Các hướng tối ưu hóa chính của chiến lược:

- Điều chỉnh tham số chu kỳ của các đường EMA để phù hợp với nhiều loại tài sản hơn.

- Thêm các chỉ báo lọc khác như MACD, Bollinger Bands, v.v., để nâng cao độ chính xác đánh giá.

- Tối ưu hóa tỷ lệ chốt lời/cắt lỗ, đạt được sự cân bằng tốt nhất giữa rủi ro và lợi nhuận.

- Thêm cơ chế cắt lỗ thích ứng như cắt lỗ theo ATR để kiểm soát rủi ro giảm giá tốt hơn.

Thông qua việc điều chỉnh tham số đa chiều và đưa vào các biện pháp kiểm soát rủi ro, có thể liên tục nâng cao độ ổn định và khả năng sinh lời của chiến lược.

Tổng kết

Chiến lược giao dịch đèn giao thông này tích hợp theo dõi xu hướng và đánh giá đảo chiều, sử dụng 4 đường EMA để hình thành tín hiệu giao dịch, thông qua tối ưu hóa tham số để thích ứng với nhiều loại tài sản hơn, thể hiện khả năng sinh lời mạnh mẽ trong backtest. Trong tương lai, thông qua kiểm soát rủi ro và đưa thêm các chỉ báo đa dạng, nó có tiềm năng trở thành một chiến lược giao dịch định lượng ổn định và hiệu quả.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © maxits

// 4HS Crypto Market Strategy- 1